This Audit Lessons sets out six lessons aimed at improving management of corporate credit cards, based on four ANAO 2023–24 performance audits on compliance with corporate credit card requirements and other relevant audits over the past five years.

1. Compliance with credit card requirements by senior executives sets the tone for the entity

2. Controls to prevent and detect credit card non-compliance are needed to address risks

3. Policies and procedures should be fit for purpose and make it straightforward for staff to do the right thing

4. Credit card training can improve levels of compliance

5. Transaction approvers should be in a position to exercise independent judgement

6. Internal audits and reporting on credit card compliance can assist with ongoing assurance and improvement

Lesson 1: Compliance with credit card requirements by senior executives sets the tone for the entity

Senior Executive Service (SES) officers set the tone for the entity. SES officers need to set a positive example for staff by demonstrating compliance with both the letter and the spirit of an entity’s integrity framework, which includes corporate credit card requirements.

The Australian Public Service Commission (APSC) states that the APS must maintain and foster a pro-integrity culture at the institutional level that values, acknowledges and champions doing the right thing.

The APSC states that SES officers ‘set the tone for workplace culture and expectations’, they ‘are viewed as role models of integrity and professionalism’ and ‘are expected to foster a culture that makes it safe and straightforward for employees to do the right thing’. SES officers can model integrity by:

- understanding and fulfilling their obligations for credit card use;

- complying with the letter and the spirit of credit card requirements;

- highlighting to staff that integrity should be central to every decision, including those related to the use of credit cards;

- making it safe for staff to raise concerns, admit mistakes and learn from them; and

- addressing suspected misuse of credit cards in a fair, timely and effective way.

Lesson 2: Controls to prevent and detect credit card non-compliance are needed to address risks

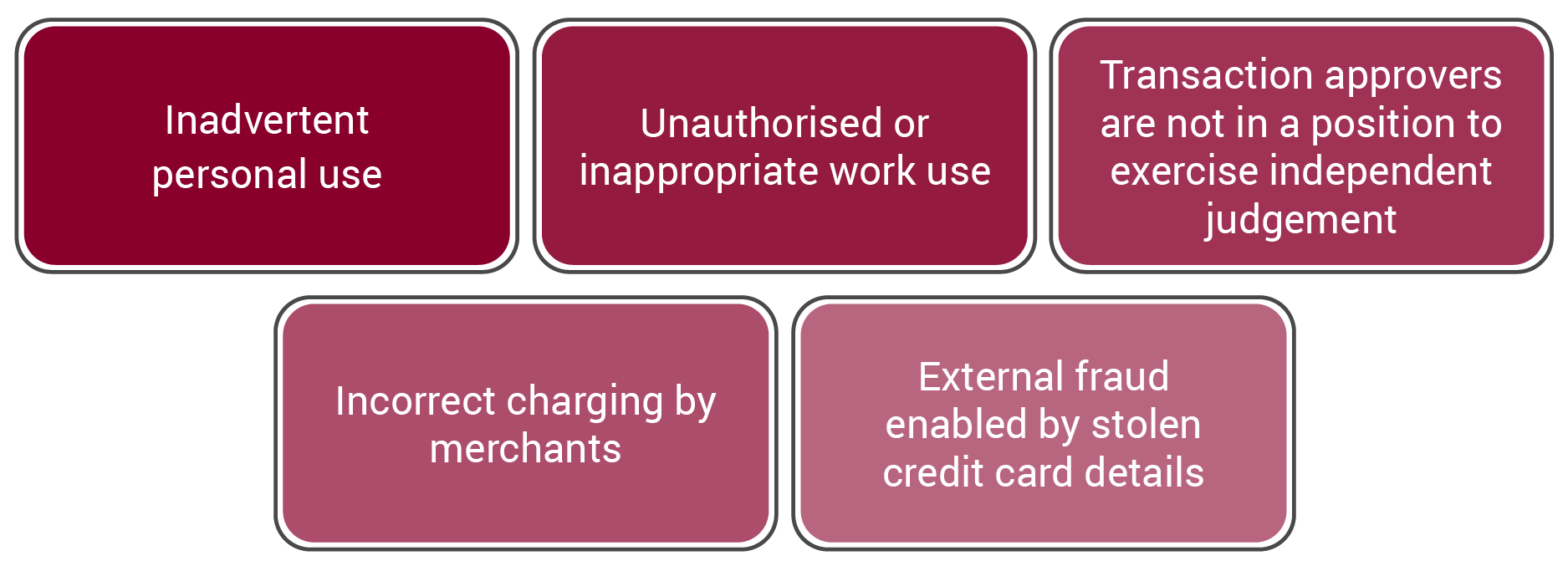

Corporate credit cards are a source of fraud and corruption risk, as well as other financial risks. Accountable authorities must establish and maintain an appropriate system of internal control for the entity, including measures to ensure officials comply with the finance law. The Commonwealth Risk Management Policy supports this PGPA Act requirement.

The Fraud and Corruption Rule requires accountable authorities to take all reasonable measures to prevent, detect and deal with fraud relating to their entities. The Commonwealth Fraud and Corruption Policy and Finance guidance support these requirements.

Entities need to assess risks associated with corporate credit cards and put mitigating controls in place to prevent and detect non-compliance.

When developing controls for credit card management, an entity should consider risks in its operating environment.

Examples of corporate credit card risks

Preventive controls work by reducing the likelihood of inappropriate credit card use before it occurs. Preventive controls for credit cards could include:

- policies and procedures;

- education and training;

- deterrence messaging;

- declarations and acknowledgements to communicate and confirm that a person understands their obligations and the consequences for non-compliance;

- blocking certain categories of merchants;

- issuing cards only to those with an established business need;

- cancelling or suspending cards when staff resign or are on long-term leave;

- placing limits on available credit; and

- limiting the availability of cash advances.

Detective controls work after a credit card transaction has occurred by identifying if there is a risk that it may have been inappropriate. Detective controls for credit cards can include:

- regular acquittal and reconciliation processes (with segregation of duties between cardholder and approver);

- fraud detection software;

- detection of outlier transactions and exception reporting;

- tip-offs and public interest disclosures;

- monitoring and reporting incidents to management; and

- audits and reviews.

When detective controls identify instances of fraud or non-compliance, entities should have effective processes in place for managing investigations and follow-up actions (such as further training, sanctions, or referral to law enforcement agencies).

The Fraud and Corruption Rule requires relevant Australian Government entities to conduct periodic reviews of the effectiveness of the entity’s fraud and corruption controls. Fraud and corruption control testing can involve desktop reviews, system or process walkthroughs, data analysis, sample testing and pressure testing. Entities can strengthen their fraud and corruption control frameworks by employing different testing methods and better documenting testing outcomes.

Robust testing of controls can help identify deficiencies and potential improvements to the existing controls to ensure they are achieving their intended purpose in preventing and detecting fraud or misuse. Recently observed examples of control deficiencies include the following.

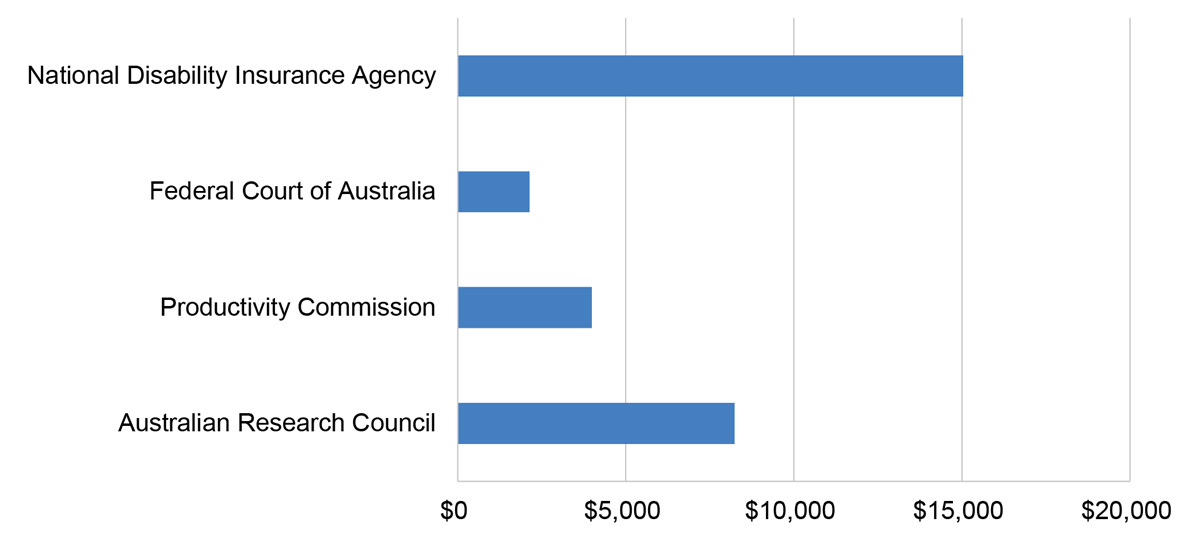

Australian Research Council

The ARC has training and education arrangements for cardholders and supervisors and requires all cardholders to sign a cardholder agreement form acknowledging the consequences for credit card misuse.

The ARC controls register stated that the credit card provider would block same value transactions from the same merchant where these occurred over a ‘short time frame’ to reduce the risk of duplicate transactions. This risk control had not been tested. The ANAO found an example of the credit card provider not blocking two identical value transactions that occurred within four minutes of each other.

Federal Court of Australia

The Federal Court of Australia’s (FCA) Commonwealth Credit Card Policy requires departing staff to immediately notify the finance team to cancel their credit card.

The FCA did not require post-travel provision of CabCharge receipts to support expense approval. Additionally, there was no requirement for managers to approve CabCharge transactions post-travel.

National Disability Insurance Agency

NDIA Finance Policies include several requirements for credit card cancellation or suspension, including that credit cards be suspended when staff go on leave for greater than six weeks, and credit cards be cancelled when staff leave the NDIA.

From the examined sample of 117 credit card transactions, the ANAO identified 11 transactions that occurred during a period when the credit card should have been suspended, and one which occurred after the credit card should have been cancelled. These transactions had not been identified by the NDIA as non-compliant.

Productivity Commission

The PC’s Corporate Credit Cards Policy and Procedure requires that a taxi card be used for only official domestic taxi travel and taxi alternatives.

Control over taxi card compliance relied on staff adhering to its taxi card policy requirements and the finance team manually checking for non-compliant transactions each month. There were no processes in place to block or restrict certain merchant categories on taxi cards.

To read more, see paragraph 2.15 of Compliance with Corporate Credit Card Requirements in the Australian Research Council; paragraph 3.41 of Compliance with Corporate Credit Card Requirements in the Federal Court of Australia; paragraphs 17, 2.50 and 3.23 of Compliance with Corporate Credit Card Requirements in the National Disability Insurance Agency; and paragraphs 3.21 to 3.24 of Compliance with Corporate Credit Card Requirements in the Productivity Commission.

Lesson 3: Policies and procedures should be fit for purpose and make it straightforward for staff to do the right thing

Entities can help public servants comply with credit card requirements by ensuring credit card policies and procedures are straightforward and fit for purpose for the entity’s risks and operating environment.

Entities should ensure their policies and procedures clearly outline how credit cards are to be issued, used and returned; and what officials’ responsibilities are under the finance law. The Department of Finance has published model accountable authority instructions, which include instructions for managing corporate credit cards. These model instructions assist entities with establishing clear policies and procedures that are tailored to an entity’s operating environment and risks.

In 2024, the ANAO examined whether four entities had developed fit-for-purpose policies and procedures for the issue, use and return of corporate credit cards.

All four entities’ accountable authority instructions and other policies included requirements for the issue, use and return of credit cards.

Australian Research Council

Policies and procedures were not reviewed and updated in line with the ARC’s timeframes.

Certain language in the ARC’s credit card policy was not clear. For example, the use of ‘may’ in policies, such as the credit card ‘may’ be cancelled by the ARC’s finance team when a credit cardholder ceases employment with the ARC.

Federal Court of Australia

Eligibility requirements for issuing credit cards could have defined business need criteria for card issuance. More guidance could have been provided on using and acquitting CabCharge cards.

National Disability Insurance Agency

Accountable authority instructions and the NDIA’s finance policies were reviewed annually and were largely consistent with Australian Government guidance on managing credit cards.

Productivity Commission

Eligibility criteria for issuing credit cards and information on the need for supporting documentation for transactions under the PC’s required limit could be improved.

To read more, see paragraphs 2.25 to 2.43 of Compliance with Corporate Credit Card Requirements in the Australian Research Council; paragraphs 2.22 to 2.44 of Compliance with Corporate Credit Card Requirements in the Federal Court of Australia; paragraphs 2.42 to 2.57 of Compliance with Corporate Credit Card Requirements in the National Disability Insurance Agency; and paragraphs 2.12 to 2.30 of Compliance with Corporate Credit Card Requirements in the Productivity Commission.

Lesson 4: Credit card training can improve levels of compliance

Delivering tailored training to credit cardholders and their supervisors on corporate credit card requirements is an effective preventive control that supports compliance. This should include periodic messaging that outlines good practices and raises awareness of fraud and non-compliance risks.

Training in the proper use of credit cards should be a prerequisite for the issuing of a credit card. All credit cardholders (including SES officers) and those with approver and reviewer responsibilities should be required to undertake induction and periodic refresher training (such as through an e-learning module). Training could outline good practice, provide clear examples of what non-compliance looks likes, and explain fraud and non-compliance risks. Monitoring training completion is important to ensure this control is operating as intended.

The ANAO examined whether the PC had developed effective training and education arrangements to promote compliance with policy and procedural requirements. The ANAO found that while the PC had published relevant policies and procedures on its intranet, it did not provide structured training and education to promote compliance with corporate credit card policy and procedural requirements.

The PC advised the ANAO in November 2023 that its policy is that all staff must complete a finance induction training session with the Finance Director, who can provide further tailored credit card training as required.

There was no evidence of finance induction training sessions occurring, other than a presentation for graduates and a reference outlining key financial resources available through the intranet. These materials did not include content related to corporate credit card policy and procedural requirements.

The ANAO’s random sample of 47 PC credit card transactions included the following examples of non-compliance: no taxi card transactions had receipts; 16 transactions were not raised in the system prior to or within 48 hours of the transaction occurring; two travel-related transactions occurred on weekends, when the approved travel dates were weekdays; and there was one instance of accidental personal misuse.

To read more, see paragraphs 2.31 to 2.33 and 3.38 of Compliance with Corporate Credit Card Requirements in the Productivity Commission.

In 2023, the ANAO examined probity management within the Australian Securities and Investments Commission (ASIC), including ASIC’s management of credit cards. The ANAO found ASIC’s probity management to be largely effective and that ASIC had implemented credit card training.

Credit card training was mandatory for staff who held a credit card.

ASIC required all credit cardholders to complete training on corporate credit card expenditure at least every 2 years.

ASIC managers had access to a dashboard showing training completion for their staff, with individual reports produced in relation to training non-compliance. Completion rates for mandatory training were reported quarterly to senior management committees.

The ANAO examined a sample of ASIC credit card transactions and found that: all receipts or other supporting documentation were provided (where applicable); 88 per cent of transactions were acquitted within required timeframes; all transactions were approved in line with requirements; and there were no observed instances of personal misuse.

To read more, see paragraphs 14, 2.114 to 2.118, and 4.41 to 4.47 in Probity Management in Financial Regulators — Australian Securities and Investments Commission.

Lesson 5: Transaction approvers should be in a position to exercise independent judgement

Under the PGPA Act, officials must exercise their powers, perform their functions and discharge their duties with care and diligence, honestly, in good faith and for a proper purpose. Officials also have a duty to not improperly use their position to gain a benefit or advantage for themselves or any other person. Transaction approvers must be able to fulfill these duties by being in a position to exercise independent judgement over the legitimacy of a credit card transaction.

A corporate credit cardholder’s expenditure is typically approved by their supervisor. An SES officer’s credit card expenditure should not be approved by an officer who is more junior to them (even if the approver is an SES officer). Having a more junior officer approve transactions introduces the risk that an officer will not perform their duties with the same level of care and diligence as they would if they were monitoring someone junior to them. This ‘positional authority’ risk should be considered when delegating authority to approve credit card transactions, including for key roles, such as accountable authorities.

If suitable, entities could also implement transparency measures, such as regularly reporting on the expenses of accountable authorities to audit committee chairs.

In 2024, the ANAO examined entities’ arrangements for transaction acquittals and how entities managed the risk of ‘positional authority’ — where the approver is not in a position to exercise independent judgement.

Australian Research Council

The risk of inappropriate positional authority between an approver and credit cardholder was not explicitly addressed in the ARC’s risk management documents.

The ARC advised the ANAO in January 2024 that a ‘one-up’ in level policy approval is in place. The ARC’s financial delegations’ policies did not outline the ‘one-up’ requirement. The policies allowed for approvers to be at the same level as the applicant, or at a lower level. ANAO analysis identified that acquittals for the CEO (a statutory appointment) were approved by either the Branch Manager Corporate Services (a lower-level SES officer) or the Chief Financial Officer (a non-SES officer). The ANAO recommended the ARC implement transparency measures, such as to regularly report on CEO expenses to the Audit Committee Chair.

National Disability Insurance Agency

The NDIA’s finance policies did not specify the process for travel pre-approval, or review of credit card and travel acquittals, for the CEO or for members of the NDIA board.

The NDIA board did not pre-approve the Chair’s or board members’ travel expenses. Instead, they were approved by NDIA staff at SES or non-SES levels. From a sample of 117 transactions, the ANAO identified 20 credit card acquittals for the CEO and other SES officers, where the approving officer was junior to the credit cardholder. The CEO and board members made 51 trips where the approving delegate was junior to the traveller. The ANAO recommended NDIA address positional authority risk by requiring that: expenditure by the NDIA Board Chair be approved by a deputy or other NDIA Board member; expenditure by NDIA Board members (other than the Chair) be approved by the NDIA Board Chair; and expenditure by the NDIA CEO be approved by the NDIA Board.

To read more, see: paragraphs 3.38 to 3.41 of Compliance with Corporate Credit Card Requirements in the Australian Research Council; and paragraphs 2.51–2.55, 3.25 and 3.30 of Compliance with Corporate Credit Card Requirements in the National Disability Insurance Agency.

Lesson 6: Internal audits and reporting on credit card compliance can assist with ongoing assurance and improvement

Regular reporting to executive management on credit card issue, use and return; non-compliance; and actions taken in response to non-compliance gives management visibility over the effectiveness of internal controls. It can also provide insights into fraud and integrity risks within the entity and help executive management to better understand and manage these risks.

Entities should include a rolling program of internal audits that examine key internal controls, including controls for corporate credit card management.

Reporting on credit card non-compliance can provide assurance to the accountable authority, the executive committee, the audit committee and other relevant governance committees. Timely and accurate internal reporting of credit card use is important to address risks and issues as they occur. Internal audits are a valuable way to identify opportunities for improvement and highlight areas of risk.

The ANAO’s review of the PC’s reporting on credit card use found the following.

The PC used monthly statements and reports from its financial management system to complete credit card acquittals.

This information was not aggregated at either a current or historical level to provide organisation-wide reporting to executive management. As a consequence, executive management lacked visibility of current and historical non-compliance rates, and the overall effectiveness of entity controls.

To read more, see paragraphs 2.38 and 2.39 of Compliance with Corporate Credit Card Requirements in the Productivity Commission.

As part of the examination of whether entities had appropriate arrangements for managing credit card risks, the ANAO examined whether credit card management had been the subject of a recent internal audit.

Australian Research Council

- An internal audit was completed in 2021–22 on reporting and monitoring of operational risks that exceed the ARC’s risk appetite. The internal audit did not directly consider credit card risk, but stated that ‘the ARC’s overall approach to undertaking the review process provides adequate assurance that it is complying with its financial management obligations under Finance Law’.

Federal Court of Australia

- Two internal audits relevant to corporate credit cards were undertaken and reported to the FCA’s audit and risk committee, one in 2017 and one in 2023.

Productivity Commission

- An internal audit on key financial controls was completed in 2022, which included a review of the PC’s use of credit cards. The internal audit identified five ‘agreed actions’ related to credit cards.

To read more, see paragraphs 2.22 to 2.24 of Compliance with Corporate Credit Card Requirements in the Australian Research Council; paragraph 2.18 of Compliance with Corporate Credit Card Requirements in the Federal Court of Australia; paragraph 2.34 of Compliance with Corporate Credit Card Requirements in the National Disability Insurance Agency; and paragraphs 2.9 to 2.11 of Compliance with Corporate Credit Card Requirements in the Productivity Commission.