Areas examined

This chapter examines whether the Australian Research Council (ARC) had effective arrangements in place to manage the issue, return and use of corporate credit cards.

Conclusion

The ARC’s arrangements for managing the issue, return and use of corporate credit cards were largely effective. Documentation of policies and procedures could be improved and the ARC has not tested all risk controls related to credit cards. The ARC did not respond to parliamentary questions on notice with accurate information on credit card use.

Areas for improvement

The ANAO identified one opportunity for improvement to ensure policies and procedures are reviewed and updated within established timeframes; and strengthening language in policies, and procedures (paragraph 2.32).

2.1 If Australian Government officials deliberately misuse corporate credit cards, they are committing fraud. Other risks of credit card use include: inadvertent personal use; unauthorised or inappropriate work use; incorrect charging by merchants; and external fraud enabled by stolen credit card details.

2.2 Under the Public Governance, Performance and Accountability Act 2013 (PGPA Act), an accountable authority of an Australian Government entity has a duty to establish and maintain appropriate systems of risk oversight and management and internal control, including measures to ensure that officials comply with the finance law.

2.3 In addition, the Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) establishes a requirement for an accountable authority of a non-corporate Commonwealth entity to take all reasonable measures to prevent, detect and deal with fraud relating to the entity. Specific requirements of the Australian Government’s Fraud Rule include:

- conducting regular fraud risk assessments and developing and implementing a fraud control plan that deals with identified risks;

- establishing appropriate preventive controls (which should include fit-for-purpose policies and procedures and effective training and education arrangements); and

- establishing appropriate monitoring and reporting arrangements.

Have appropriate arrangements been established for managing risks associated with use of corporate credit cards within the ARC?

Risks related to credit card misuse are contained in the ARC’s Fraud Control Plan. Credit card compliance is reviewed through an annual CEO compliance review and a compliance survey every four months. There are opportunities for the ARC to improve the identification and management of controls around duplicate transactions.

Enterprise risk management arrangements

2.4 The ARC has a risk framework in place which is supported by processes and documents that set out general requirements and minimum standards that need to be considered when implementing the risk framework. Documents supporting the risk framework include:

- ARC Fraud Control Plan 2020–22 and 2022–24;

- ARC Risk Management Policy (April 2021);

- ARC Risk Management Plan and Toolkit (April 2021); and

- ARC Chief Executive Instructions (September 2018 and May 2023), which adopt the Accountable Authority Instructions (AAIs).

2.5 Elements of the risk framework most relevant to credit card risk are the ARC’s risk register and the ARC Credit Card Policy; through which the ARC has explicitly considered actions to mitigate credit card risk.

Fraud control plan and fraud risk register

2.6 The ARC Fraud Control Plan’s purpose is to ‘provide policy direction, instructions and procedural guidelines for fraud control by ARC officials’ to meet the requirements of the PGPA Act.

2.7 The ARC Fraud Control Plan includes the Risk Analysis Matrix, which describes a ‘Low rating’ as meeting the ARC’s risk appetite. The ARC has ‘zero tolerance’ for fraudulent activities.

2.8 The ARC has combined its operational and fraud risks into a single risk register, which the ARC advised the ANAO in April 2024 is reviewed twice a year. The risk register has a dedicated section for credit cards that identifies:

- risk owners at a business unit as the Corporate Services Branch and at an individual-level, the Chief Financial Officer;

- risk event, causes and impacts;

- whether something is a ‘fraud risk’;

- risk levels, likelihood and consequence of occurrence;

- whether an incident had actually occurred;

- controls in place;

- shared risks; and

- residual ratings.

2.9 Table 2.1 outlines the seven credit card-related risks identified in the ARC’s risk register and the ARC’s assessment of inherent risk levels and the corresponding residual risk levels. The ARC advised the ANAO in April 2024 that it assesses the residual risk levels, twice a year, against the implemented controls and mitigations consistent with the ARC’s Fraud Control Plan.

2.10 Two inherent risks were assessed as ‘Medium’. All seven residual risk ratings were ‘Low’. The ARC evaluates residual risks based on its assessment of controls implemented to manage risks. These controls include:

- a dedicated finance team reviewing all statements and reconciliations;

- the approvals processes;

- credit card limits; and

- controls in place by the bank.

Table 2.1: Credit-card related risks and ARC-identified risk level

|

Fraudulent purchases and transactions made on a corporate credit carda

|

Medium

|

Low

|

|

Unauthorised transactions and expenditure charged to a credit cardb

|

Medium

|

Low

|

|

Finance section staff (who have access to all credit card numbers) make fraudulent purchases by phone

|

Low

|

Low

|

|

Corporate credit cardholders make cash withdrawals

|

Low

|

Low

|

|

Fraudulent purchases (domestic including Australian Government credit card and overseas purchases when cardholder is on travel allowance)

|

Low

|

Low

|

|

A stolen or lost card not reported in a timely way used to make purchases

|

Low

|

Low

|

|

Card details misused by merchants (including double billing, bogus purchases, fraudulent purchases and overcharging)

|

Low

|

Low

|

| |

|

|

Note a: The ARC Risk Register identified controls to reduce this risk from medium to low: a small number of people with access who review reconciliations; appropriate fraud awareness training and instructions signed by cardholders; approvals processes; low card limits; CFO only verifying all cards issued; banks monitoring out of the ordinary transactions and PIN authorisation required for over-the-counter transactions.

Note b: The ARC Risk Register identified controls to reduce this risk from medium to low: approvals processes, the finance section checking all reconciliations, including checking receipts; low card limits; and bank controls that block same value transactions made by the same merchant within a short time frame.

Source: ANAO analysis of the ARC risk register.

2.11 The ARC’s risk register considers credit card risks associated with travel.

- Controls to prevent fraudulent credit card travel transactions are: travel movement requisitions; and credit card reconciliations needing approval by supervisors.

- The register considers the risk of fraudulent purchases caused by staff members using the ARC credit card to purchase meals or incidentals when they have been paid travel allowance.

- The controls for fraudulent purchases caused by staff members using the credit card when they should use travel allowance are:

- credit card reconciliations are approved by the cardholder’s supervisor and reviewed by the Finance Section;

- travel requires a travel acquittal; and

- low card limits are in place.

2.12 There are examples of inconsistencies on the ARC’s risk documents for credit cards.

- In the risk register, ‘Fraudulent purchases and transactions’ was marked as ‘FALSE’ under ‘fraud risk’.

- The ARC Risk Analysis Matrix states ‘low risks…do not require further attention’, and is inconsistent with the statement ‘periodic confirmation that controls continue to be in place and are effective’.

Risk mitigation

2.13 The ARC Credit Card Policy states that staff are not to obtain cash advances. The check box on initial credit card — HSBC applications can be selected to prevent this. HSBC confirmed to the ARC in February 2024 that cash advances are blocked regardless of the check box control; and cash advances are blocked for all current cardholders.

2.14 Merchant blocking can be used to prevent the misuse of corporate credit cards and minimise fraud risks by excluding classes of transactions from high-risk vendors. The ARC does not block merchant types, and it has advised the ANAO in February 2024 that blocking specific merchants would introduce more risk as some merchant types are broader than others. The ARC considers misuse of credit card details by merchants as a risk in the risk register, however there is no documented risk assessment that takes into account the risk around blocking certain merchant types.

2.15 The ANAO identified one instance where a risk control had not been tested. A credit card risk control listed in the ARC risk register stated the credit card provider will block same value transactions made by the same merchant ‘within a short time frame’ to reduce the risk of duplicate transactions. The ANAO identified one occasion where payments from the same merchant, for the same amounts were made on the same day. Despite being valid transactions, these were not identified by the ARC or blocked by HSBC.

2.16 The ARC Credit Card Policy considers risk mitigation through five scenarios where a credit card could be cancelled:

- the cardholder ceases employment with the ARC;

- the cardholder no longer requires the card because of a change of duties or position;

- the cardholder fails to comply with any CEO Directions, ARC’s policies or procedures relating to the use of the credit card;

- requested to do so by a supervisor, director or the Chief Financial Officer (CFO) or Deputy Chief Financial Officer (DCFO); or

- the credit card has not been used for more than twelve months.

Compliance review

2.17 The ARC finance team conducts ongoing transactional checks and an annual review of credit card compliance, which is documented as part of the annual CEO compliance review.

2.18 The ARC requires its executive level and senior executive staff to complete a compliance survey every four months. The compliance survey has two questions about awareness of:

- personal purchases on their corporate credit card; or

- failure to follow the ARC Credit Card Policy and Procedures.

2.19 The ARC advised the ANAO in April 2024, responses to the survey are analysed by the finance team and CFO and reported to the ARC Audit and Risk Committee. Two instances where a corporate credit card was accidentally used for personal purchases were reported through the compliance survey and included in the annual CEO compliance review 2021–22. There were no instances reported in 2022–23.

2.20 In its annual CEO compliance review, the ARC stated that preventive and detective controls are in place and:

ongoing testing [and] checking is conducted on compliance with financial delegations, and compliance with the delegation to sign contracts, upon transaction entry to the contracts register and upon processing claims for payment. Any issues identified are recorded in the Financial Non-Compliance Register or Late Payment of Invoices Register.

2.21 Incidents of non-compliance identified by the ARC have been included in the risk register.

Audit Committee and Management-Initiated Review

2.22 The ARC’s Audit and Risk Committee provides oversight of the entity’s enterprise risk management framework for identification and management of financial risks, including fraud. The ARC’s Fraud Control Plan identifies reviews and internal audits as a way to minimise the impact of fraud. The ARC’s Audit and Risk Committee is provided with information on credit card risk, but there was no mention of credit card risk in the ARC audit committee minutes beyond consideration of the annual compliance reporting.

2.23 An internal audit was completed in 2021–22 on the ARC risk management framework to review arrangements for reporting and monitoring of operational risks that exceed the ARC’s risk appetite. The internal audit did not directly considered credit card risk, but stated that ‘the ARC’s overall approach to undertaking the review process provides adequate assurance that it is complying with its financial management obligations under Finance Law’. There were no internal audits on credit card compliance in 2022–23.

2.24 McGrath Nicol completed a series of risk workshops in June 2022, as part of the management-initiated review of the ARC’s fraud control arrangements. The aim of the review was to understand the level of fraud risk and control awareness by its staff. The review identified controls and gaps for a number of scenarios with a risk of occurrence (inappropriate disclosure to grant recipients, inappropriate use of Government assets). The misuse of credit cards and unauthorised purchases was considered as a specific scenario. The credit card scenario noted a control which limited transactions to $5,000, contradicting the ARC Credit Card Policy that sets transaction limits by the classification level of individual cardholders.

Has the ARC developed fit-for-purpose policies and procedures for the issue, return and use of corporate credit cards?

The ARC’s policies and procedures for the issue, return and use of credit cards included coverage of requirements within accountable authority instructions and other policies. There is scope to improve documentation of policies and procedures. Policies and procedures were not reviewed and updated in line with the ARC’s timeframes. Language in the documents could be strengthened.

Policies and procedures

2.25 The ARC has policies and procedures to cover the issue, return and use of credit cards. During 2021–22 and 2022–23 the following were in place:

- ARC Credit Card Policy (March 2010 and February 2023) for HSBC corporate credit cards;

- ARC Credit Card Procedure (March 2021) for HSBC corporate credit cards;

- ARC Chief Executive Instructions (September 2018 and May 2023);

- ARC Financial Delegations Matrix;

- ARC Financial Delegations Guidance (December 2022);

- ARC Travel Policy (January 2020 and December 2022);

- ARC Official Hospitality Guidelines (April 2019); and

- ARC Official Hospitality and Gifts Policy (June 2023).

2.26 Policies and procedures met the requirements of the AAIs for non-corporate Commonwealth entities set out by the Department of Finance (see Box 1). Policies did not explicitly include the AAI requirement to ensure individual card use, but the ARC uses a form to gain approval before using another person’s credit card. The form was last updated in 2014 and the requirement to use the form is not documented in policies or procedures.

2.27 The ARC Financial Delegations Matrix was in use during 2021–22 and 2022–23. This assigned financial delegations for approval of types of transactions over $150. Transactions, in accordance with the ARC Credit Card Policy, up to $150 do not require delegate approval. The ARC Financial Delegations Matrix assigned approval delegation for purchases related to hospitality and gifts, overseas travel and IT assets.

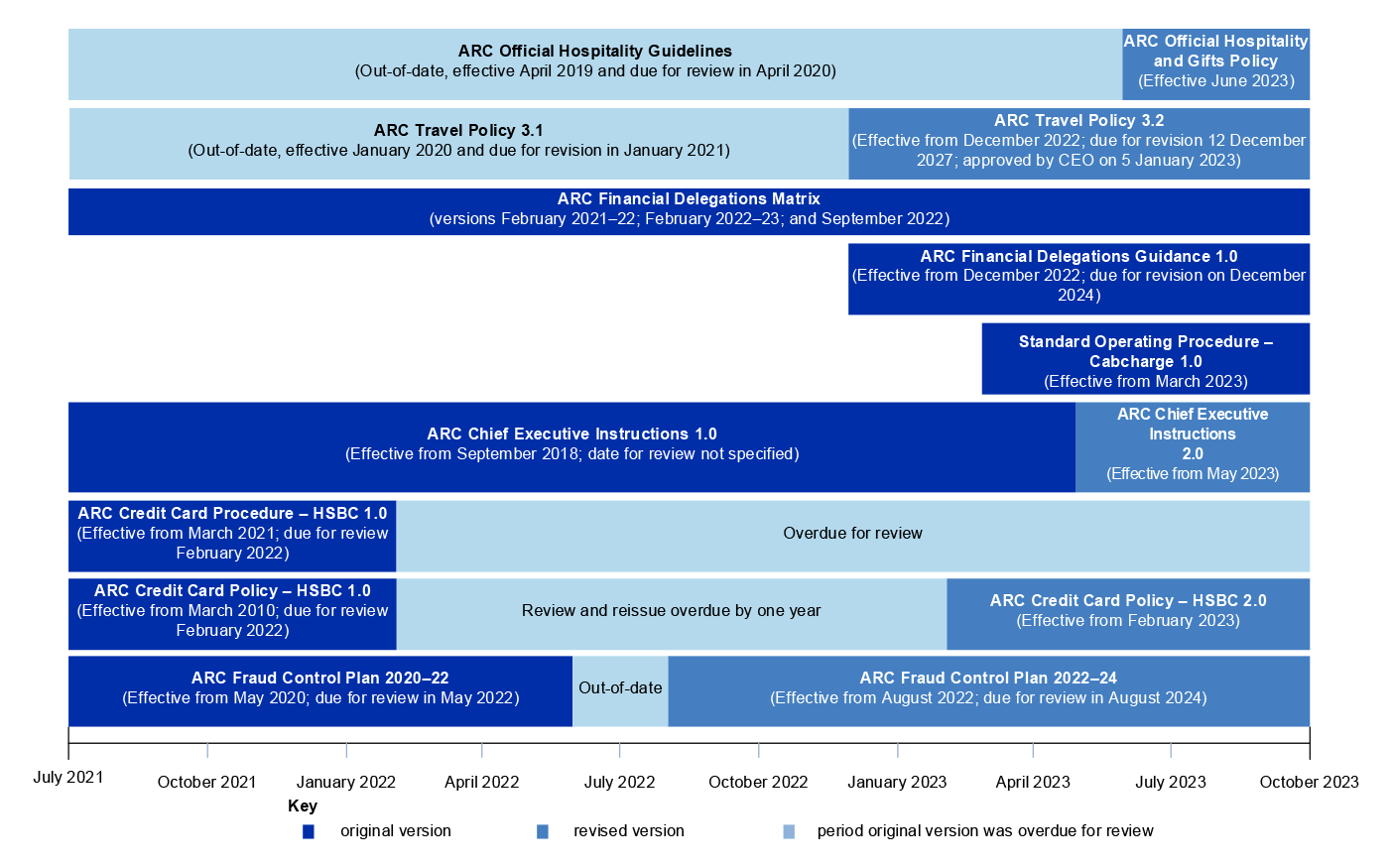

2.28 Figure 2.1 outlines policies and procedures in place during 2021–22 and 2022–23. There were policies and procedures which were not reviewed by the scheduled review date:

- ARC Credit Card Policy — HSBC 1.0 was due for review in February 2022. The new version 2.0 was in place in February 2023;

- ARC Credit Card Procedure — HSBC 1.0 was due for review in February 2022;

- ARC Fraud Control Plan — 2020–22 was due for review in May 2022. The new 2022–24 version was in place in August 2022;

- ARC Official Hospitality Guidelines — 1.0 was due for review in April 2020. It was subsequently replaced with the ARC Official Hospitality and Gifts Policy in June 2023; and

- ARC Travel Policy — 3.1 was due for review in January 2021. The new version was in place in December 2022.

2.29 The following policies and procedures were implemented during 2022–23:

- ARC Financial Delegations Guidance 1.0 —in place December 2022;

- Standard Operating Procedure — Cabcharge 1.0 was in place from March 2023; and

- ARC Official Hospitality and Gifts Policy 1.0 — in place June 2023.

2.30 The following policies were implemented after 2022–23:

- ARC Credit Card Policy — Diners Club Virtual Card Number 1.0, from November 2023; and

- ARC Financial Delegations Policy 1.0, from November 2023.

Figure 2.1: Summary of the ARC policies and procedures in place during 2021–22 and 2022–23

Source: ANAO analysis of ARC policies and procedures.

2.31 The ANAO identified language, such as ‘may’; and examples of instructions in the ARC Credit Card Policy and Procedures that were not followed in practice:

- ‘[t]he card is not transferable and may be cancelled by ARC Finance’ when ‘[t]he Cardholder ceases employment with the ARC’;

- ‘Credit Card Coordinator will lock the card in the Finance safe’; and

- ‘the supplier is then contacted to verify they are a legitimate business’.

|

2.32 The Australian Research Council consider:

- reviewing and updating its policies and procedures within the established timeframe; and

- strengthening language in policies and procedures.

|

Issue

2.33 Eligibility requirements for credit card applications are identified and documented in the ARC Credit Card Policy. These apply to ongoing and non-ongoing employees and eligible contractors, with a ‘genuine business need’. This business need is identified in the ARC Credit Card Policy to facilitate payment for minor purchases and travel expenditure. Cardholders are required to sign the Corporate Credit Card Agreement, which sets out cardholder responsibilities and terms of use, including limits.

2.34 The ARC has a procedure for the issue of corporate credit cards. The ARC Credit Card Procedure requires the supervisor, Executive Level 2 or higher (or equivalent) to send a recommendation to the Credit Card Coordinator, that the ARC staff member requires an HSBC corporate credit card. The procedure states that the recommendation should include what the card is to be used for (travel, purchasing or both) and the credit limits to be applied. The ARC Credit Card Policy requires all requests for the issue of a corporate credit card to be approved by the CFO or DCFO after director or branch manager approval. Once approved, the Credit Card Coordinator makes arrangements to issue corporate credit cards, including preparing an application form for completion by the proposed cardholder.

2.35 Once an HSBC corporate credit card is received by the Credit Card Coordinator after approval, the Corporate Credit Card Agreement is signed by the cardholder, who then takes possession of the card. The agreement requires the cardholder to acknowledge that the card will be used for either travel-related expenditures or minor purchases and identifies the monthly financial limit and transaction limit. The agreement seeks the cardholder to acknowledge that they have understood the following:

- ARC Corporate Credit Card Policy — HSBC;

- ARC Corporate Credit Card Procedure — HSBC;

- ARC Travel Policy;

- ARC Chief Executive Instructions; and

- HSBC Corporate Card and HSBC Business Card — User Condition of Use.

Use

Corporate credit cards

2.36 Arrangements are in place for corporate credit card and travel delegations, approvals and authorisations. The ARC Financial Delegations Matrix and ARC Financial Delegations Guidance determine approval levels for certain types of transactions over $150 (also refer to paragraph 2.27 for amounts up to $150). The policy and procedure set requirements for approvals and pre-approvals. The $150 amount that can be approved by delegates, as described in the ARC Financial Delegations Matrix, is not included in the policy and procedure; or the ARC Financial Delegations Guidance.

2.37 The ARC Credit Card Procedure requires cardholders to take the following steps when acquitting credit card transactions. Key requirements include:

- matching the supporting documentation for the transaction (for example, the tax invoice or receipt) to the statement;

- completing a credit card reconciliation form;

- each purchase on the statement needs to be coded to the appropriate general ledger account and cost centre codes; and

- reconciliations must be submitted to the ARC finance team by the deadline unless an alternative arrangement has been agreed by the ARC finance team.

2.38 The credit cardholder must attach all required supporting documentation at the time of acquittal.

Travel

2.39 The Department of Finance established and manages the Whole of Australian Government Travel Arrangements (Travel Arrangements). The objectives of these arrangements are to reduce travel costs, decrease administrative costs, simplify processes and optimise savings. Under the Travel Arrangements payments, such as for official airfares, accommodation and car rental expenses, are made through Diners Club. Other arrangements include travel through QBT; airfares purchased from a panel of 18 airlines; accommodation purchased through AOT; and vehicle rental services purchased through Hertz.

2.40 The ARC implemented Diners Club virtual card from 2010, without a Diners Club card policy. Diners Club virtual cards are not individually issued to ARC staff. Instead, a single virtual Diners Club card is managed by the ARC’s finance team for travel-related payments, such as airfares, accommodation, and vehicle rental expenses; and other travel-related costs booked through the Travel Arrangements. Travel was booked under Travel Arrangements, with the Diners Club card, as per the ARC Travel Policy. Executive assistants used individual travel spreadsheets as a tool to ensure travel policies, including approval procedures are followed.

Return

2.41 On cessation of employment, the employee is required to complete an exit notification form managed by the human resources team. The form requires the cardholder to confirm the return of their credit card.

2.42 A corporate credit card may be cancelled under certain circumstances. The ARC CEIs require ‘review [of] patterns of usage with a view to cancelling infrequently used cards’. The ARC advised the ANAO in November 2023 that usage trends are not reviewed.

2.43 Policies and procedures were in place to cover issue, use and return of credit cards. There are elements of processes that are not documented, these are the:

- process of applying for a new credit card on the HSBC portal;

- tracking process for pre-approvals for assets;

- timeframes for reconciliations; and

- recording of travel approvals through individual spreadsheets by executive assistants.

Has the ARC developed effective training and education arrangements to promote compliance with policy and procedural requirements?

The ARC Credit Card Procedure and acquittal form provide details for acquittal. The cardholder agreement form outlines the credit card usage requirements. The ARC provides mandatory Fraud Awareness and Commonwealth Resource Management Framework e-learning to all staff and access to relevant webinars on fraud and scams.

Credit card training

2.44 The ARC has training and education arrangements in place for cardholders and supervisors. The ARC Credit Card Procedure and acquittal form both describe the process for acquittal. The ARC advised the ANAO in December 2023 that training is provided one-on-one as needed. The ARC provides risk and fraud e-learning to all the ARC staff to ensure they understand their responsibilities under the PGPA Act; and HSBC — the credit card provider — provides relevant webinars on common types of fraud and scams.

2.45 A Fraud Awareness and Commonwealth Resource Management Framework e-learning course is available in the ARC’s LearnHub (an online training platform) and comprises mandatory training for all staff. In calendar year 2022 and 2023, completion rates were 99 per cent and 97 per cent, respectively. The ARC advised the ANAO in April 2024 that it obtains these levels of completion through active follow-up and that lack of completion by staff members was due to long-term leave. One staff member did not complete the mandatory training in 2022 and four staff members in 2023. The ARC advised the ANAO in April 2024 that reminder emails were sent to staff members that had not completed the training. There was no evidence to demonstrate how this was managed when the staff members continued to remain non-compliant.

Does the ARC have appropriate arrangements for monitoring and reporting on the issue, return and use of credit cards?

The ARC has arrangements for monitoring and reporting on the issue, return and use of credit cards. The ARC monitors statements and acquittals on an ongoing basis and can produce reports on issue, return and use of cards through the HSBC Online Portal, as required. The ARC reports on credit card use as part of the annual CEO compliance review and monitors credit card compliance. The ARC reported on credit card issue and use when requested by Parliament, which included an overstatement for two questions on notice.

Monitoring issue and return

2.46 The ARC uses the HSBC Online Portal to track and report on issued and cancelled corporate credit cards as required. The register provides details on:

- cardholder details;

- credit card number;

- credit card expiry;

- credit limit;

- current balance; and

- credit card open and close date.

Monitoring use and reporting

Internal reporting

2.47 The ARC reports on credit card use to the CEO, as part of the annual financial statement process. The finance team tracks statements and acquittals and can draw reports from the HSBC Online Portal, although these procedures are not documented. Reports required outside of the annual compliance review process are drawn from the online portal as required.

2.48 The ARC reported four credit card-related incidents in the relevant period, of two types (personal misuse and purchase of an asset without pre-approval), through the annual CEO compliance review. These were entered into the risk register as risk events that had occurred. Additional non-compliances with policy were noted in the annual CEO compliance review. In the annual CEO compliance review 2021–22, the results of the annual sampling of credit card transactions (three sampled per month) identified one instance where the transaction was not acquitted properly; but this was not linked to the risk register. The information was presented in the report in an aggregated way, and did not identify details of the sample transactions used to complete the review.

2.49 The HSBC Online Portal allows the ARC to track returned credit cards. The ARC advised the ANAO in April 2024 that credit cards were cancelled due to staff leaving, surrendered voluntarily due to lack of use, or staff reporting cards as ‘lost or stolen’.

Reporting to Parliament on corporate credit card use

2.50 The ARC provided responses to a series of questions on notice on credit card issue and use to the Standing Committee on Education and Employment following Senate Estimates hearings in 2022–23 and 2023–24. The ARC’s responses to a selection of questions are outlined in Table 2.2 (see Appendix 3 for the complete set of questions).

Table 2.2: ARC responses to Senate Estimates questions on notice on credit cardsa

|

Period covered by answer

|

Between 1 July 2022 and 28 February 2023

|

Between 1 July 2022 and 31 May 2023

|

|

Number of cards on issue

|

36

|

36

|

|

Largest reported purchase

|

$8,528

|

$8,995

|

|

No. of cards reported lost or stolen

|

0

|

0

|

|

No. of purchases deemed illegitimate or contrary to policy

|

3b

|

4c

|

|

Amount of illegitimate or contrary to policy purchases

|

$6,266.00d

|

$6,352.00e

|

|

Amount repaid

|

$50.00

|

$136.00

|

|

Highest value illegitimate or contrary to policy purchase repaid

|

$50.00

|

$85.79

|

| |

|

|

Note a: Figures reported in this table are GST inclusive.

Note b: Consists of purchase of two iPhones ($3,916.65), 12 headsets ($2,212.55) and a repaid personal transaction ($50.23).

Note c: Consists of purchase of two iPhones ($3,916.65), 12 headsets ($2,212.55) and repaid personal transactions of two employees ($50.23 and $85.79).

Note d: The ANAO queried a possible discrepancy in the calculations. The ARC confirmed in April 2024 there was an error in the calculations of the total amount of purchases made contrary to policy. The amount should equate to $6,179.43, which was an overstatement of $86.57. One purchase related to a personal transaction of $50.23 (see paragraph 3.46) and was repaid. The remaining two purchases ($3,916.65 and $2,212.55) were reported as minor assets without pre-approval from CFO. The ARC advised Parliament in its question on notice response that these were ‘a proper use of resources’, but ‘not in accordance with agency policy’ and ‘[c]orrective action was undertaken and all ARC Officials were reminded about the Agency’s policy in relation to the purchase of assets which requires the Chief Financial Officer to provide approval prior to an acquisition being made by credit card.’

Note e: The ANAO queried a possible discrepancy in the calculations. The ARC confirmed in April 2024 there was also an error in the calculations of the total amount of purchases made contrary to policy. The amount should equal $6,265.22, which was an overstatement of $86.78.

Source: Senate Estimates question on notice database.

2.51 The ARC’s responses to Senate Estimate questions reported the non-compliance identified through the ARC’s internal review process. The values reported to Parliament were inaccurate, resulting in an overstatement of the actual expenditure. The ARC advised the ANAO in May 2024 this was due to human error.

2.52 The ANAO identified that the ‘purchases’ reported in the questions on notice were the equivalent of 10 HSBC corporate credit card transactions. The ARC advised the ANAO in June 2024 that it had grouped transactions related to the same events and reported them as ‘purchases’ in the responses to questions on notice.

2.53 In the 2022–23 Supplementary Budget Estimates, the ARC reported three ‘purchases’ as contrary to policy, grouped as iPhones, headsets and personal misuse (meal purchase). These ‘purchases’ consisted of five HSBC corporate credit card transactions.

2.54 In the 2023–24 Budget Estimates, the ARC reported an additional illegitimate ‘purchase’ grouped as another personal use (taxi fare). This additional ‘purchase’ comprised a further five transactions.