Areas examined

This chapter examines whether the Productivity Commission (the Commission) has implemented effective controls and processes for credit cards in accordance with its policies and procedures.

Conclusion

The Commission’s controls and processes for managing credit card issue, usage and return were partly effective in controlling the risk of credit card misuse. Preventive controls were not effective in preventing non-compliant taxi card transactions. There were weaknesses in detective controls relating to the provision of supporting documentation when reconciling taxi transactions. Positional authority risks could be better managed by clarifying delegation and approval requirements for senior executive cardholders. While the Commission has recovered funds from cardholders where instances of personal misuse have been identified, it has not documented its processes for escalating and managing identified non-compliance.

Areas for improvement

The ANAO made three recommendations aimed at: improving controls to prevent non-compliant credit card use (paragraph 3.23); increasing documentation requirements for monthly reconciliations (paragraph 3.37); and documenting processes for managing identified instances of non-compliance (paragraph 3.50).

The ANAO also identified three opportunities for improvement for the Commission to: establish a systematic approach to assessing and recording business needs for issuing credit cards (paragraph 3.7); maintain a complete and accurate record of monthly spending and individual transaction limits (paragraph 3.11); and clarify approval requirements and delegations for senior executive cardholders, and official hospitality and catering purchases (paragraph 3.20).

3.1 Preventive controls work by reducing the likelihood of inappropriate credit card use before a transaction has been completed. Preventive controls for credit cards can include: policies and procedures; education and training; deterrence messaging; declarations and acknowledgements; blocking certain categories of merchants; issuing cards only to those with an established business need; placing limits on available credit; and limiting the availability of cash advances.

3.2 Detective controls work after a credit card transaction has occurred by identifying if there is a risk that it may have been inappropriate. Detective controls for credit cards can include: regular reconciliation processes (with segregation of duties between cardholder and approver); exception reporting; fraud detection software; tip-offs and public interest disclosures; monitoring and reporting; and audits and reviews.

3.3 When detective controls identify instances of fraud or non-compliance, entities should have effective processes in place for managing investigations and follow-up actions (such as further training, sanctions, or referral to law enforcement agencies).

Has the Productivity Commission implemented effective preventive controls on the use of corporate credit cards?

Preventive controls implemented by the Commission could be improved by strengthening visibility of cardholder spending and transaction limits. Preventive controls for hospitality and catering expenditure, purchases covered by whole-of-government arrangements, and to prevent non-compliant taxi card transactions were not operating effectively. Positional authority risks could be further managed through clarifying delegation and approval requirements for senior executive cardholders.

Issuing credit cards

3.4 Issuing corporate credit cards to staff with an established business need is a key preventive control to reduce the risk of inappropriate use.

3.5 The June 2022 internal audit of key financial controls (see paragraphs 2.9 to 2.11) identified that credit cards were obtained for Commission staff without prior confirmation of a business need (although cards obtained were not always provided to staff). In response, the Commission committed to review current corporate credit cards to determine if there was a continuing need for them, and schedule periodic reviews of ongoing business needs. The first action was closed in October 2023, noting that a preliminary review of credit card utilisation had been completed and further action was delayed until the implementation of a new credit card provider in 2024. The second action was closed in April 2023, noting that a quarterly review schedule had been implemented by the finance team.

3.6 The Commission provided four emails between the finance team and cardholder managers from October 2023 as evidence of its a review of the cardholder register. The emails noted that the finance team was seeking to determine if corporate cards held in the safe were still required. The Commission had not completed subsequent quarterly reviews.

|

3.7 The Commission could establish a more systematic approach to assessing and recording business needs for issuing credit cards and undertake a thorough review of the ongoing business needs of existing cardholders.

|

Managing transactions

Credit card spending limits

3.8 As noted in paragraph 2.13, the Corporate Credit Cards Policy and Procedure identifies that limits of $3,000 per month and $300 per transaction apply for taxi cards issued to the Chair, Commissioners, Senior Executive Service (SES) and Executive Level 2 employees and no limits apply to their virtual travel cards. The policy does not define any limits for procurement cards or taxi and travel cards held by other staff.

3.9 Limits for taxi cards had generally been adhered to, with one non-compliant airline transaction exceeding the $300 individual transaction limit, which the Commission attributed to a Diners Club administration error (non-compliant taxi card purchases are discussed at paragraphs 3.21 and 3.22).

3.10 As noted at paragraph 2.35, the Commission does not have a complete cardholder register that records cardholders’ monthly spending and individual transaction limits for other card types. This control weakness impedes the ability of the Commission to monitor adherence with spending limits for procurement cards. The Commission advised the ANAO in March 2024 that the credit card limit report can be downloaded from the Diners Club system anytime. Documenting assigned monthly and individual transaction spending limits within a register is an important control to ensure cards have been set up correctly by the credit provider, in alignment with entity delegations and guidance, as well as to facilitate assurance activities.

|

3.11 The Commission could establish a process to ensure that it has a complete and accurate record of monthly spending and individual transaction limits for all credit card types, and that limits align with the Commission’s delegations instrument.

|

Pre-approval for credit card purchases

3.12 Pre-approval and documentation of rationale for expenditure is a key control to ensure purchases are appropriate and can withstand public scrutiny.

Purchases covered by whole of Australian Government arrangements

3.13 As noted at paragraph 2.19, the Commission’s Accountable Authority Instructions (AAIs) state that staff must ‘use any mandated whole-of-government [procurement] arrangement’ (such as arrangements established by the Department of Finance and Digital Transformation Agency for accommodation and travel services, stationery and office supplies, and ICT equipment).

3.14 Analysis of the Commission’s credit card transactions shows there were transactions in categories covered by mandatory coordinated procurement arrangements in 2022–23 (see Table 3.1).

Table 3.1: Transactions not using whole-of-government arrangements in 2022–23

|

Apple

|

ICT equipment

|

4

|

$9,053.90

|

|

Officeworks

|

Stationery and office supplies

|

5

|

$302.25

|

|

Ergonomic Office

|

Stationery and office supplies

|

4

|

$610.00

|

|

Enterprise Rent a Car

|

Car rental services

|

2

|

$904.07

|

| |

|

|

|

Source: ANAO analysis based on transaction data provided from the Productivity Commission.

3.15 The Commission provided a rationale to the ANAO in March 2024 for each of the identified transactions where coordinated procurement arrangements were not used.

- For Apple charges, three transactions were originally placed through the panel, but Apple cancelled orders through the reseller to prioritise fulfilling direct orders. The other transaction was for an urgent repair that was deemed to be cheaper to repair directly through Apple. There was supporting documentation for three of the four transactions.

- Both car rental transactions were for rental cars in remote locations not covered by whole-of-government providers. There was supporting documentation for both transactions in the form of email correspondence and receipts.

- For the nine stationery and office supplies transactions, expenditure was for ergonomic equipment that was not available through the coordinated procurement arrangements or required immediately.

- For the four transactions from Ergonomic Office, there was documentation noting that the whole-of-government supplier did not supply the product required in three instances, and that urgent delivery was required for the other purchase.

- For the five transactions from Officeworks, two transactions were supported by documentation justifying the purchases. These purchases were made in relation to equipment recommended in Workstation Assessment Reports, which was not available through the whole-of-government supplier. Supporting documentation was not provided for the remaining three transactions. The Commission advised in March 2024 that the items were for ergonomic equipment either not available from the whole-of-government supplier or required immediately.

Official hospitality and business catering expenditure

3.16 As noted at paragraph 2.19, the Commission’s AAIs state that decisions to spend relevant money on official hospitality and business catering must be publicly defensible. In addition, the AAIs note that to enter into an arrangement to provide official hospitality, employees must be delegated the power to enter an arrangement, act in accordance with the Commonwealth Procurement Rules, and complete an official hospitality form for fringe benefit tax requirements.

3.17 The Commission’s AAIs and Delegations Instrument do not define or limit who has a delegation to authorise expenditure on official hospitality related goods and services. The only references to delegations are on the Commission’s hospitality and catering form. The form identifies expenditure relating to social functions, restaurant meals, business meetings with lunch and employee achievement functions as hospitality expenses that can only be approved by the Head of Office (SES Band 3) or the Chair. For catering expenditure (morning and afternoon teas and light lunches), the form notes ‘current delegations apply’. The Commission advised the ANAO in April 2024 that:

The intent of the wording on the hospitality form is to guide the admin staff and not a delegation listed in our AAI.

3.18 The Commission’s credit card transactions in 2021–22 and 2022–23 shows there were a low number of transactions on food and beverage related transactions (see Table 3.2).

Table 3.2: Food and beverage related credit card expenditure, 2021–22 and 2022–23

|

|

No. of transactions

|

Expenditure

|

No. of transactions

|

Expenditure

|

|

Liquor store

|

0

|

$0.00

|

1

|

$77.20

|

|

Restaurant/café

|

10

|

$939.99

|

9

|

$1345.39

|

|

Supermarket

|

20

|

$741.77

|

14

|

$747.55

|

|

Total

|

30

|

$1,681.76

|

24

|

$2,170.14

|

| |

|

|

|

|

Source: ANAO analysis based on data provided from the Productivity Commission.

3.19 The ANAO conducted targeted testing on ten food and beverage related transactions from 2022–23. Based on supporting documentation, the purchases were for: a social function (1); catering for internal events (coffee, bakery and supermarket purchases) (4); a restaurant meal (1); food items for an interstate trip (1); and attendance at external events including lunch (3).

- The one hospitality transaction for a social function (a seminar for internal and external participants) involved purchasing alcohol from a liquor store. It was supported by an itemised receipt, hospitality and catering form and documentation confirming attendees for the event. The purchase was pre-approved by a First Assistant Commissioner (SES Band 2) and advice was sought from the finance team prior to the purchase being made. As noted in paragraph 3.17, the Commission has not clearly defined who is delegated to authorise expenditure on official hospitality.

- Three of the four catering transactions were supported by hospitality and catering forms and emails confirming purchase pre-approval. The fourth transaction was a $73 purchase made by the Head of Office on 13 April 2023 (to buy coffees for Commissioners whilst visiting Melbourne). The transaction was not raised in TechnologyOne and did not have a supporting receipt retained. The Commission informed the ANAO in April 2024 that the Head of Office acknowledged this purchase was non-compliant and repaid the transaction on 17 April 2024. There was no pre- or post-approval recorded for this transaction. Under the Commission’s Travel Guidelines, the Chair or the Assistant Commissioner Corporate Group (if required) are expected to approve the Head of Office’s transactions. As the Assistant Commissioner Corporate Group is junior to the cardholder, this introduces positional authority risk. There was no evidence the potential for positional authority risk related to credit card use, including travel, had been appropriately assessed and managed by the Commission.

- The three external event transactions were supported by tax invoices and learning and development forms with pre-approval from appropriate delegates.

- The $306 restaurant meal transaction was supported by an itemised receipt, seminar agenda, and undated hospitality and catering form. There was no evidence of transaction pre-approval. In 2022 the Commission’s Research Committee approved broader funding for seminar services, but specific details on costings and timings were not discussed. The restaurant meal formed part of a lunch and seminar hosted by the Commission in April 2023. Supporting evidence indicated that the transaction was for six Commission staff and two external speakers.

- Two transactions were non-compliant taxi card purchases (non-compliant taxi card purchases are discussed at paragraphs 3.21 and 3.22).

- One was the $73 catering purchase (noted above) made by the Head of Office.

- The other transaction was a supermarket purchase of food items for an interstate meeting with a supporting receipt but no evidence of pre-approval.

|

3.20 The Commission could clarify approval requirements and delegations for senior executive cardholders, purchases covered by mandatory coordinated procurement arrangements, and official hospitality and catering purchases. Additional guidance could also be provided on alcohol purchases.

|

Merchant blocking

3.21 As noted in Box 2, the Commission’s Corporate Credit Cards Policy and Procedure includes a requirement to only use a taxi card for official domestic taxi travel and taxi alternatives. ANAO analysis of the Commission’s taxi card transactions identified 24 non-compliant purchases in 2022–23 (see Table 3.3).

Table 3.3: Non-compliant taxi card transactions in 2022–23

|

Diplomat Hotel

|

Hotel

|

1

|

$195.00

|

|

Jetstar

|

Airlines

|

1

|

$37.38

|

|

KSBN Investments Pty Ltda

|

Restaurant

|

1

|

$73.00

|

|

Qantas Airwaysb

|

Airlines

|

1

|

$962.87

|

|

QBT Pty Ltdb

|

Airlines

|

2

|

$13.21

|

|

Quizletc

|

Other

|

2

|

$20.00

|

|

Ryan Traders Pty Ltd

|

Retail

|

1

|

$49.80

|

|

Spar Express

|

Retail

|

2

|

$15.72

|

|

Spotifyc

|

Other

|

7

|

$97.93

|

|

Uber Eatsd

|

Restaurant

|

1

|

$41.69

|

|

Woolworths

|

Retail

|

5

|

$345.82

|

|

Total

|

24

|

$1,852.42

|

| |

|

|

|

Note a: Transactions with these merchants were included the ANAO’s targeted testing discussed at paragraph 3.19.

Note b: The Commission advised the ANAO in April 2024 that the QBT Pty Ltd and Qantas Airways transactions were made on a virtual travel card, and not a taxi card, and there was an error with Diner Club administration.

Note c: The Commission identified Spotify and Quizlet transactions that were instances of fraud activities, cancelled the relevant cards and recovered $86.93 through alerting its credit provider to the fraudulent transactions.

Note d: The Uber Eats transaction was identified as accidental personal use and repaid by the cardholder. The transaction was recorded in the Commission’s misuse register as accidental misuse.

Source: ANAO analysis based on taxi card transaction data provided from the Productivity Commission.

3.22 The Commission’s control over taxi card compliance relies on staff adhering to its taxi card policy requirements and the finance team manually checking for non-compliant transactions each month. There are no processes in place to block or restrict certain merchant categories on taxi cards. As noted in Table 3.3, some of the non-compliant transactions were identified by the Commission as fraudulent or accidental misuse and recovered. For the remaining transactions, the Commission advised the ANAO in April 2024 that, despite being non-compliant with policy requirements, the purchases were made for acceptable business purposes.

Recommendation no.4

3.23 The Productivity Commission establish arrangements to ensure corporate credit cards are only used for the purposes defined within its policy requirements.

Productivity Commission response: Agreed.

3.24 The Commission accepts the recommendation and is reviewing the policy and the types of cards that are issued.

Returning cards

3.25 When ceasing employment or taking extended leave, cardholders are required to complete a clearance certificate to ensure that all types of credit cards are returned. The finance team signs off on the form once employees have returned the cards. The form outlines that:

All employees of the Commission who are leaving permanently, or who are expected to be on any type of extended leave for more than six months, must obtain the clearance required below before ceasing duty with the Commission, and before any final salary or cashed out leave entitlements will be paid.

3.26 The cessation form includes fields for finance, library, IT, human resources and payroll teams to sign off on the return of relevant equipment, including credit cards and outstanding monies.

3.27 In cardholder agreements for taxi cards and purchasing cards, cardholders are required to acknowledge that lost or stolen cards will be reported immediately to Diners Club, supervisors and the finance team.

3.28 The finance team maintains a card tracking and closure spreadsheet containing data extracted from the Diners Club system and employee cessation data obtained from human resources. There was one instance where the spreadsheet did not contain sufficient information to determine if cardholders had used their cards after they had ceased employment. The cardholder’s cessation date (provided by the human resources team) was recorded as January 2023, but credit card activity occurred after that date.

3.29 The Commission advised the ANAO in April 2024 that the employee had retired from the Commission in January 2023 and then returned as a casual employee, and as such the transactions identified after the date of cessation were acceptable. The card number identified in the card closure spreadsheet was different to the card number used in the transaction report and cardholder register, indicating that a new card was issued to the employee.

3.30 While the card tracking and closure spreadsheet stated that six cardholders had lost or stolen credit cards in 2022–23, the Commission advised the ANAO in April 2024 that cards marked as lost or stolen cards were cards that were cancelled due to fraudulent Spotify and Quizlet transactions. The Commission viewed the cards as compromised and not physically stolen, so it did not report them in its answers to Senate Estimates questions on notice (see Table 2.3).

Has the Productivity Commission implemented effective detective controls on the use of credit cards?

The Commission’s finance team reviews, acquits and verifies transactions manually each month. The Commission has not developed an approach to retaining and storing receipts for all taxi card transactions, which heightens the risk of errors, irregularities and fraud going undetected.

Verifying transactions

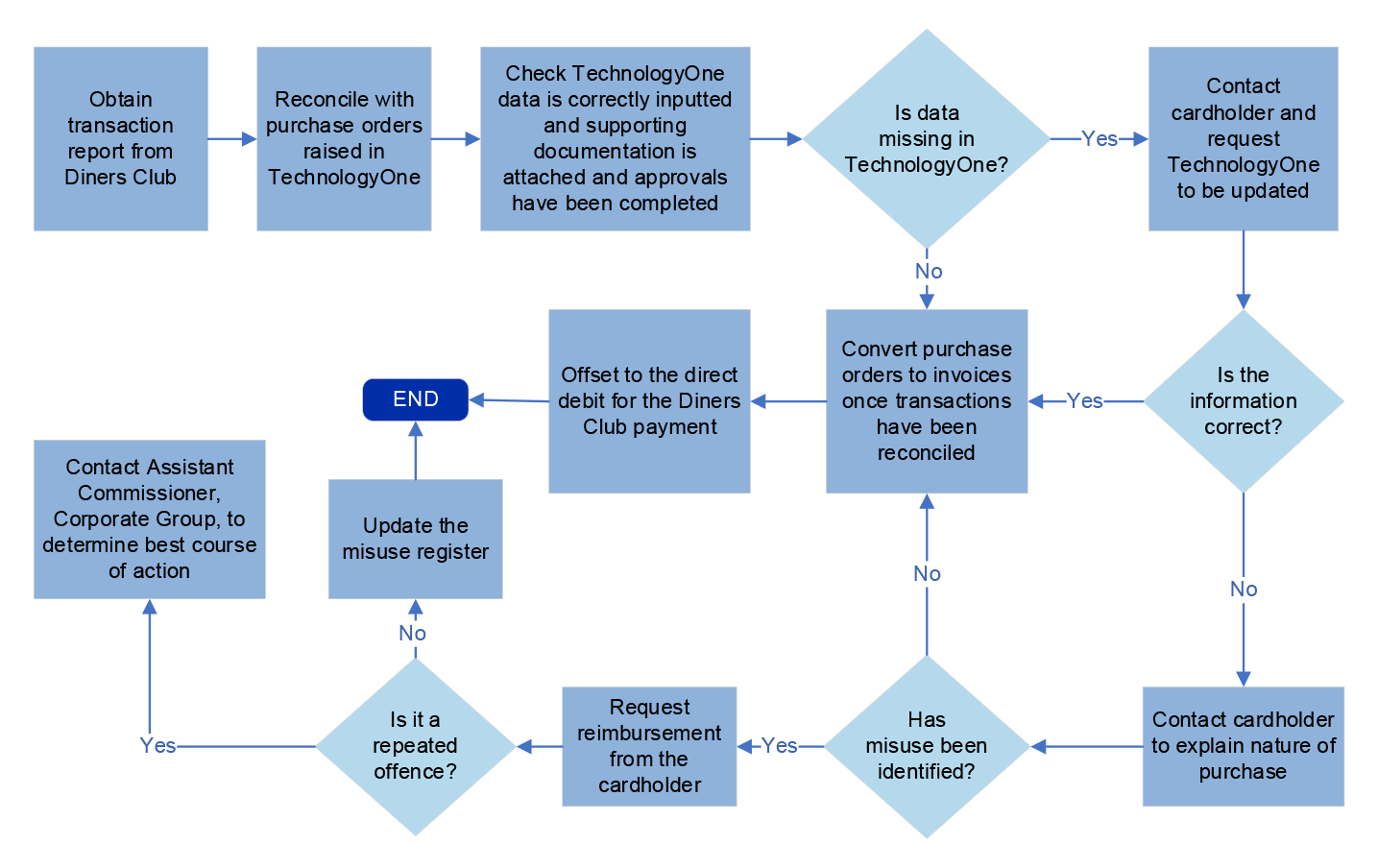

3.31 The Commission’s finance team is responsible for reconciling all credit card transactions following the end of a statement cycle each month. This process involves manually reconciling movement requests from TechnologyOne and Diners Club transaction reports. Figure 3.1 outlines the process for the finance team reconciliation transactions once a purchase has been made and raised in TechnologyOne.

Figure 3.1: Credit card acquittal process

Source: ANAO process map analysis based on the Commission’s procedural documentation.

3.32 When misuse has been identified, the finance team adds it to a misuse register to record transactions that do not comply with the Commission’s policies and procedures. The finance team also follows up with the cardholder and queries the transaction. If the transaction is not recognised by the cardholder, it is reported to Diners Club for investigation. If the cardholder has charged a private expense, they are provided with the Commission’s bank details for repayment. If the cardholder continues to charge private expenses to the card, their manager and the Assistant Commissioner, Corporate Group, will be advised, and the cardholder may have their card cancelled.

3.33 The accuracy of the reconciliation process relies on the finance team manually reconciling each individual transaction each month. The Commission advised the ANAO in November 2023 that this is not an efficient process and advised the ANAO that it was seeking to introduce new measures to enhance the system in the next financial year. As identified in paragraph 2.40, the Commission has developed a proposal to support the delivery of a new credit card management system. The proposal is yet to be endorsed.

Procurement and taxi card acquittals

3.34 The Corporate Credit Cards Policy and Procedure requires procurement and taxi card holders to raise transaction or movement requests in TechnologyOne prior to or within 48 hours of transactions occurring. Requests are then submitted for delegate approval by managers. As outlined at paragraph 2.22, there is a lack of clarity in the Commission’s policies and procedures about supporting documentation requirements, but the Commission’s AAIs state that supporting documentation (either a tax invoice, receipt, credit card docket or statutory declaration) is required for all transactions. The policy does not set out timeliness requirements for the reconciliation process.The ANAO conducted testing on a random sample of 47 procurement and taxi card transactions to assess compliance with policy requirements. The sample comprised 13 procurement card transactions and 34 taxi card transactions. The following instances of non-compliance were identified:

- 16 transactions were not raised in the system prior to or within 48 hours of the transaction occurring;

- 13 transactions were not reconciled in a timely manner (under 50 days);

- 19 transactions did not have any form of supporting documentation and all 34 taxi card transactions did not include receipts;

- two travel-related transactions occurred on weekends, when the approved travel dates in TechnologyOne only covered weekday travel; and

- there was one instance of personal misuse (an Amazon Prime subscription), which was identified by a member of the finance team and reimbursed by the cardholder.

3.35 There were limitations in the reconciliation process to ensure all transactions were appropriately evidenced and justified. The lack of supporting documentation attached to taxi card transactions increases risks of non-compliance with internal policy requirements. The current process does not provide the entity with sufficient assurance that cardholders are using their taxi cards for valid business needs. Without visibility over supporting receipts for transactions, the delegate or finance team cannot appropriately determine the validity of charges.

3.36 The Commission advised the ANAO in January 2024 that it was aware of the shortcomings of the current system for performing reconciliations, and it intended to implement enhancements that would facilitate the collection and storage of taxi receipts.

Recommendation no.5

3.37 The Productivity Commission improve reconciliation of corporate credit card transactions by ensuring appropriate documentation is provided to approvers and the finance team as part of monthly reconciliation processes.

Productivity Commission response: Agreed.

3.38 The Commission agrees with the recommendation, is implementing upgrades to the finance system to support the collection of all documentation and has consistently reflected the requirements in its policies and procedures.

Travel acquittals

3.39 All official travel and related expenses need to be recorded and approved by raising a movement requisition in TechnologyOne. The Commission’s travel procedures outline that travellers should obtain verbal or email pre-approval from a delegate prior to booking, movement requisitions with all attachments and entries should be completed within 24 hours of booking, and approval should be given within 48 hours of booking. The Commission’s travel approval delegations are outlined in Table 3.4.

Table 3.4: Travel approval delegations identified in the Commission’s Travel Guidelines

|

Chair, Deputy Chair, Commissioners and Associate Commissioners

|

Head of Office

|

|

Head of Office

|

Chair through Assistant Commissioner Corporate (if required)

|

|

First Assistant Commissioners, Assistant Commissioner Corporate, and Assistant Commissioner Strategic Communication and Engagement

|

Head of Office

|

|

Assistant Commissioners

|

First Assistant Commissioner in home office

|

|

Executive Level 2 (EL2) employees

|

Assistant Commissioners

|

|

Other employees

|

EL2s, Assistant Commissioners or First Assistant Commissioner

|

|

Urgent cases

|

Chair, Head of Office, Assistant Commissioner Corporate, First Assistant Commissioners

|

| |

|

Source: Productivity Commission, Travel Guidelines.

3.40 The ANAO conducted testing on 11 travel card transactions, which found the following:

- All transactions used the mandated Whole of Australian Government Travel Arrangements and were supported by receipts and travel itineraries.

- Three transactions did not have email evidence of pre-approval by a delegate and were not raised and approved in TechnologyOne within 48 hours of booking. For these three transactions, approval was received 10, 34 and 156 days after booking.

Fraud detection

3.41 The finance team does not have a systematic process to detect instances of fraud. The current process relies on the finance team reviewing each transaction manually and identifying anomalies. There is not a structured, analytical approach in place to detect potential instances of fraud at the Commission. The Commission advised the ANAO that it does not undertake such analysis due to the small volume of credit card transactions.

3.42 The Commission’s finance team received an email in September 2022 from the Department of Finance’s whole of Australian Government travel team noting that Diners Club had advised there was a high volume of fraudulent transactions mimicking subscription fee charges for common merchants (including Spotify and Quizlet). As noted in Table 3.3, the Commission subsequently identified fraudulent subscription payments on its taxi cards.

Does the Productivity Commission have effective processes for managing identified instances of non-compliance?

The Commission’s credit card control framework could be strengthened to ensure it identifies all potential instances of non-compliance. While the Commission has recovered funds from cardholders where instances of personal misuse have been identified, it has not documented its processes for escalating and managing identified non-compliance.

3.43 The ANAO’s assessment of the Commission’s credit card control framework demonstrates that there are deficiencies in implementation of preventive and detective controls that heighten the risk that non-compliant transactions could go undetected by the Commission. Deficiencies in preventive controls related to a lack of restrictions placed on taxi cards to prevent non-compliant purchases. Deficiencies in detective controls related to the provision of supporting documentation when reconciling taxi transactions.

Management and escalation processes

3.44 For all card types there is a cardholder acknowledgement of the consequences for credit card misuse, ensuring that cardholders are aware of their responsibilities and obligations. However, the process for managing misuse once it has been identified has not been documented. The Corporate Credit Cards Policy and Procedure does not include detail on the processes for managing repeated instances of non-compliance.

3.45 As noted at paragraph 3.32, the finance team maintains a misuse register through its monthly reconciliation process. The misuse register included 28 transactions totalling $601.30 that were recorded as accidental misuse for personal expenditure from July 2022 to October 2023. The full amount of these transactions was recovered by the Commission.

3.46 One cardholder made multiple non-compliant transactions in 2023, resulting in action to cancel their procurement card (see Case study 1).

|

In May 2023 a procurement card holder alerted the finance team of unintended Apple transactions on her card that dated back to February 2023. While these charges were repaid by the cardholder, the card continued to be stored in a digital wallet on her mobile phone, resulting in additional Apple transactions in May, August, September and October 2023.

Following acknowledgement from the cardholder that Apple had stored the card information and repeatedly charged it in error, the finance team recommended the card be cancelled. The Assistant Commissioner, Corporate Group, authorised the finance team to reissue the card under strict instructions that it would be cancelled if the issue happened again. This decision was later overturned after further advice was received from a senior executive, who recommended the card not be reissued to the cardholder.

The cardholder was responsible for 17 of 30 instances recorded in the Commission’s misuse register between February and October 2023, with transactions totalling $184.69. The individual continues to be identified in the Commission’s cardholder register as an active cardholder.

|

3.47 As noted in paragraph 3.34, there was one instance of personal misuse identified through ANAO sample testing. While this misuse had been identified by the finance team and reimbursed by the cardholder, it was not identified in the misuse register. This indicates that the misuse register is not being regularly updated to ensure that instances of misuse are being actively monitored.

3.48 The Commission advised the ANAO in March 2024 that instances of fraudulent activity are not identified in the misuse register. As such, instances of fraudulent activity identified in Table 3.3 were not included in the misuse register. The Commission advised the ANAO in April 2024 that it would extend its definition of what is recorded in the misuse register to account for these types of transactions.

3.49 The Commission advised the ANAO in November 2023 that actions would be taken if a pattern of repeated non-compliance was identified, but it had not yet adopted a formal mechanism to manage non-compliance due to the low number of breaches being identified. The repeated instances of misuse identified in Case study 1 were escalated to the cardholder’s manager and Assistant Commissioner, Corporate Group.

Recommendation no.6

3.50 The Productivity Commission document its process for managing identified instances of credit card non-compliance.

Productivity Commission response: Agreed.

3.51 The Commission accepts this recommendation and has incorporated the process for managing non-compliance into the credit card policy and processes.