Areas examined

This chapter considers whether the selected entities’ 2017–18 Corporate Plans supported appropriate performance measurement and reporting in the annual performance statements. It also summarises improvements made by the entities to their planned 2018–19 performance measurement and reporting.

Conclusion

The selected entities’ measurement and reporting of their performance through corporate plans and performance statements has generally improved. However, the reliability and completeness of performance criteria remain areas requiring improvement by all entities. While some improvements are already evident in the selected entities’ 2018–19 Corporate Plans, further work is necessary to establish the basis required to provide meaningful information to the Parliament and the public about the entities’ progress in achievement of their purposes.

Areas for improvement

The ANAO made two recommendations aimed at entities improving the reliability of performance measures and developing measures that provide the Parliament and public with an understanding of the entities’ efficiency in delivering their purpose/s.

The ANAO has also suggested improvements to:

- activities presented in corporate plans, through the use of more specific language to clearly describe the actions to be undertaken by the entity, and focus on those most relevant to the Parliament and the public;

- entities’ alignment of information presented in the PBSs, corporate plans and performance statements to establish a clear read between each; and

- the Finance Secretary’s Direction, to provide an improved basis to establish the line of sight between financial and non-financial performance as set out in entities’ PBS and corporate plans.

Did the selected entities’ corporate plans support performance measurement and reporting in the annual performance statements?

AGD’s corporate plan provides a clear basis to support its performance measurement and reporting by clearly expressing its purpose, and significant activities. DFAT, Education and PM&C could each improve their corporate plans by more clearly describing the activities to be undertaken to achieve their purpose/s. PM&C should relabel its mission as its purpose, and the stated purposes as objectives or priorities, to make clear to a user the impact intended to be measured. Establishing a ‘clear read’ between the PBS and corporate plan is also an area where AGD, DFAT and PM&C should improve, to support performance measurement and reporting in the performance statements.

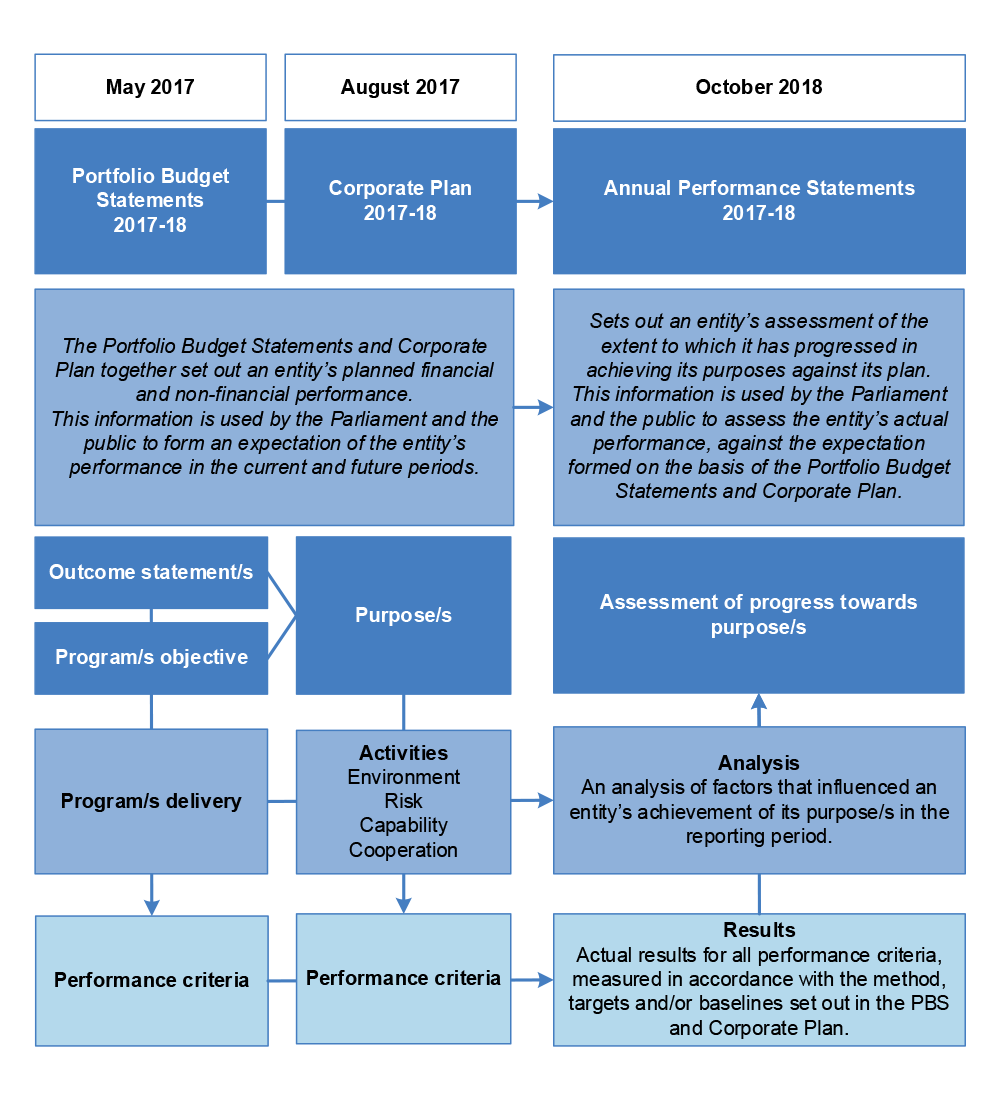

3.1 As demonstrated in Figure 1.1, an entity’s corporate plan, alongside the PBS, sets out an entity’s planned performance through the description of purposes, activities and performance criteria. The corporate plan is intended to be an entity’s primary planning document, and the key source of information for the Parliament and the public to form an expectation of an entity’s performance.

3.2 This expectation may then be compared to the actual performance set out by an entity in its performance statements through results and accompanying analysis. The Parliament and the public use this comparison to assess the extent to which the entity has met that expectation. As a result, it is important for an entity’s corporate plan to provide a clear basis to not only support an entity’s assessment of its performance, but also the Parliament’s and the public’s.

Purpose

3.3 Section 16E of the PGPA Rule requires an entity’s corporate plan to state the entity’s purpose/s over the next four years. The PGPA Act defines purpose/s as including the objectives, functions or role of an entity. The aim of the purpose/s statement is to give context to the significant activities that the entity will pursue over that period, and should be stated in a relevant and concise manner. Finance guidance notes that:

Well-expressed purpose statements make it clear who benefits from an entity’s activities, how they benefit and what is achieved when an entity successfully delivers its purposes. Essentially, purposes describe the value an entity seeks to create or preserve.

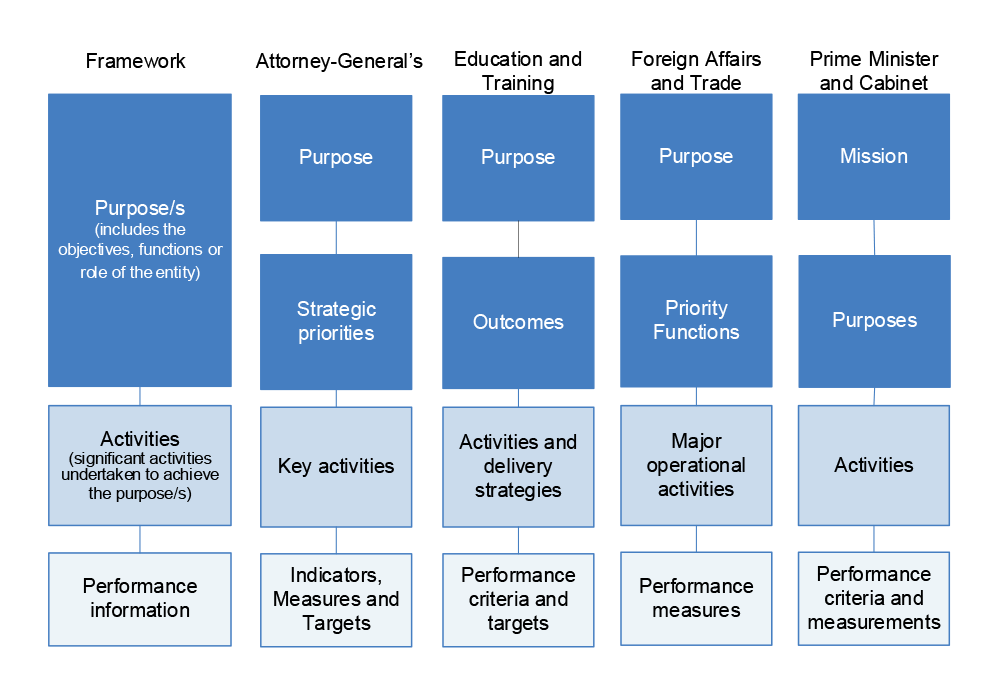

3.4 The purpose presented in the corporate plans of AGD, Education and DFAT demonstrate the required elements of a ‘well-expressed’ purpose statement. Each purpose was readily identifiable, makes clear who will benefit from the entities’ respective activities, how the entities will deliver that benefit and the impact intended to be achieved in delivery against their purposes. PM&C’s purposes require improvement to meet the characteristics set out by Finance guidance, as described below.

3.5 Education and PM&C’s 2016–17 Corporate Plans were both included in Auditor-General Report No.54 2016–17 Corporate Planning in the Australian Public Sector 2016–17. As part of this audit, the ANAO observed that Education’s purpose could be made more readily identifiable, and PM&C’s purposes were expressed as actions or activities rather than as an outcome or result to be achieved.

3.6 When comparing Education’s 2016–17 and 2017–18 corporate plans, the department replaced its vision and mission with a purpose statement. By removing the vision and mission, the purpose statement can be easily identified by a user as the definitive expression of the department’s intended purpose. This was also supported by an explanatory statement which assists to further describe who will benefit, and how the benefit is intended to be delivered by the department through achievement of its purpose. It also expands on the department’s intended impact, leading to an improved purpose statement, and addressing the observations made in the report.

3.7 In contrast, changes made to PM&C’s 2017–18 purposes from the previous corporate plan did not address the observations made in Auditor-General Report No.54 2016–17. The purposes continue to be activities based and do not describe the intended impact, with the exception of Purpose 3. However, PM&C did introduce the following ‘Mission’ in its 2017–18 Corporate Plan:

The Department of the Prime Minister and Cabinet (PM&C) advances the wellbeing of Australians by delivering high-quality support to the Prime Minister and Cabinet.

We take a whole-of-nation approach, working closely with communities, stakeholders and across all areas of government and acknowledge the special place of the first peoples of our nation. We lead the APS in rigorous and collaborative policy development, implementation and program delivery.

3.8 For comparison, the ANAO assessed the mission against the characteristics of a well-expressed purpose. The department’s mission addresses all of these characteristics, where its purposes do not. The mission sets out who will benefit (Australians), how they will benefit (supporting the Prime Minister, working with communities, rigorous and collaborative policy development, and implementation and program delivery) and the intended impact (advances the wellbeing of Australians).

3.9 Finance acknowledges that entities may wish to include strategic statements such as a Mission, however notes that ‘Strategic statements should not be included as a substitute for a clear statement of purposes.’ Presenting the mission above the labelled purposes may limit a reader’s understanding of whether it is intended to be read as the purpose, part of the other purposes, or excluded altogether for the means of performance reporting. On this basis, users of the corporate plan would benefit from PM&C relabelling the mission as its purpose and the purposes as objectives or priorities. This would make clear to a user which element is intended to have priority and how they should be interpreted.

Activities

3.10 Finance guidance notes that:

An entity’s corporate plan does not need to describe everything it does to deliver its purposes. It should focus on the high-level activities through which the results captured by its performance frameworks are achieved. A discussion of activities should provide a reader some insight and understanding of how purposes are pursued. Each activity should be explicitly linked to a purpose, together with the contribution it makes to achieving an entity’s purposes.

3.11 The ANAO assessed the activities listed by the selected entities in their 2017–18 Corporate Plans against the following criteria, sourced from Finance guidance:

- Are the activities readily identifiable?;

- Do the activities align with the entity’s purpose?;

- Do the activities clearly describe what actions the entity will undertake to achieve its purpose?; and

- Are the activities identified at an appropriate level?

3.12 Overall, all four of the entities’ activities presented in their corporate plans met, or mostly met the assessment criteria. DFAT’s, Education’s and PM&C’s activities could all be improved, through the use of more specific language, to more clearly describe the actions that were to be undertaken by the entity.

3.13 For example, Education’s activities frequently referred to the term ‘supporting’ and can reflect a number of different actions, such as: financial support in the form of payments or subsidies; or direct engagement or delivery of services; or a combination of the two. Similarly, DFAT used terms such as ‘lead’, ‘shape’, ‘advance’ and ‘contribute effectively’. Without further detail a reader is unable to determine the specific actions the departments are undertaking to pursue their purposes. Further, adjectives such as ‘vigorously’, ‘energetically’ and ‘proactively’ are unnecessary in conveying the activities to be undertaken.

3.14 In the absence of a clearer description of the activities, the degree of alignment between DFAT’s, Education’s and PM&C’s activities and purposes was not always clear. However, all activities were determined to address the entities’ purposes to some extent. An exception was the section in PM&C’s Corporate Plan outlining measures relevant to its corporate services. As noted above, the purpose of the corporate plan is to report an entity’s intentions to the Parliament and the public.

3.15 As such, the information presented should be tailored to these stakeholders and framed at an appropriate level. PM&C may consider whether the corporate services activity is presenting information of most relevance to the Parliament and the public, or whether it would be better communicated through another setting.

Alignment to Portfolio Budget Statements

3.16 As noted in paragraph 1.6, alignment across the elements of the Commonwealth performance framework is intended to improve the line of sight between the use of public resources and the results achieved by entities. Finance guidance notes:

To demonstrate the achievement of its purpose(s) entities will need to clearly map (or attribute) the performance information from the Portfolio Budget Statements to the entities’ purpose(s). This mapping will serve to establish a clear read between the entity’s corporate plan, relevant Portfolio Budget Statements, annual performance statements and the annual report, and ensure it is clear how (and how well) the entity is fulfilling its purposes.

3.17 All four entities followed Finance’s suggested presentation of performance information in the PBS, including mapping of the program/s to an accompanying purpose in accordance with the Finance Secretary’s Direction issued on 3 March 2017. However, given performance information has, in most cases, been set at a level lower than the purpose, the alignment between AGD’s, DFAT’s and PM&C’s financial and non-financial performance is not clear to a reader and could be improved.

3.18 The ANAO has previously noted that establishing links between the funding reported in the PBS and the performance information presented in corporate plans and performance statements can be difficult. This includes ensuring an entity’s funding and organisational structures facilitate the development and collection of meaningful performance information and reporting. This is particularly the case where an entity’s key activities are broadly captured by one or two PBS programs, or the nature of the entity’s role is one where coordination and collaboration activities cut across multiple programs.

3.19 AGD’s corporate plan provides a table which outlines the linkages between the PBS programs and the strategic priorities. As presented, a number of PBS programs address multiple strategic priorities. Strategic Priorities 3 and 5, the focus of this audit, are each aligned to four PBS programs and of those, three are the same. This makes it difficult for a reader to establish a clear read between the two documents, including determining the extent to which each program is attributable to the relevant strategic priorities.

3.20 Similarly, DFAT’s corporate plan provides a ‘plan on a page’ which outlines the connection between the department’s PBS Outcomes, and the priority functions presented in the corporate plan. It does not, however, provide any further insight as to how the department’s PBS programs align to the priority functions. DFAT advised the ANAO Program 1.1 was attributed to both Priority Functions 1 and 2. Without providing clear alignment, it is difficult for a reader to determine the extent of the program’s attribution to either function and, as a result, the connection between the department’s financial and non-financial performance.

3.21 Users of the performance statements would benefit from AGD and DFAT considering how the alignment between PBS programs and the lower level corporate plan elements may be simplified, to improve the line of the sight between financial and non-financial performance. Finance may also consider whether the Finance Secretary’s Direction is assisting to establish this alignment, or if requiring entities to map their PBS program performance information to a level lower than the purpose, such as objectives or activities, would improve this line of sight.

3.22 PM&C’s corporate plan notes that it should be read “in conjunction with the associated Portfolio Budget Statements and Portfolio Additional Estimates Statements for 2017–18…”, however there is no further direction to the reader as to how the Corporate Plan and relevant budget statements should be interpreted alongside one another. In comparing the two documents, it was unclear whether the PBS performance criteria were intended to stand alone, or if they presented a summary of all of the activities under the relevant purposes that would be measured. For example, one of the Program 1.1 performance criteria is:

Quality and timely policy advice, support and services to the Prime Minister, the Cabinet and key stakeholders

3.23 The criterion mentions three activities ‘policy advice’, ‘support’, and ‘services’ each of which are separately presented in the corporate plan, with multiple performance indicators and measurements. As a result, it is unclear how results against this measure were intended to be presented in the performance statements at year-end. There may be benefit in PM&C enhancing the corporate plan to make mapping of its activities and performance information to the PBS clearer for a reader.

Were the selected entities’ performance criteria relevant, reliable and complete?

Each of the entities’ performance criteria require improvement to fully meet the characteristics of appropriateness — relevant, reliable and complete. The majority of performance criteria were relevant, or mostly relevant, however the majority did not meet, or only partly met, the reliability criterion. The completeness of performance criteria also requires improvement by all entities through developing measures of efficiency, and demonstrating an entity’s intended progress across the life of the corporate plan and beyond.

Performance information hierarchy

3.24 As noted at paragraph 1.13, performance information should aim to address the accountability level of the performance information hierarchy. This level of information is essential to enable government to coordinate policy, clarify objectives, enhance transparency and accountability, improve service delivery, and keep the wider community informed.

3.25 Tactical and strategic information, which are focused on the activities and outputs that are intended to lead to fulfilment of an entity’s purpose, may be used to support higher level accountability information. Management information is an important input to determining whether an accountable authority is addressing their duties to govern an entity as set out in the PGPA Act. However, there is limited benefit for the Parliament and public where this information is solely used to demonstrate performance at the purpose level, as the connection can be too remote.

3.26 Table 3.1 summarises the mixture of management, tactical, strategic and accountability level information presented by each entity’s performance criteria. As noted in paragraph 1.15, an assessment of which level of the performance hierarchy is addressed by a performance measure is influenced by the information presented in an entity’s corporate plan. This may lead to differences in the categorisations applied when further contextual information outside the corporate plan is considered.

3.27 Of the four entities, AGD, Education and PM&C had the highest proportion of measures that addressed the two lowest levels of the performance information hierarchy, and would benefit from considering whether this mix is appropriate. Education and PM&C also had the highest number of total performance indicators — 43 and 37 respectively.

3.28 Finance guidance notes the quality of performance information should be emphasised over quantity, recommending a small set of measures that is sufficiently comprehensive to cover those factors that affect an entity’s performance. Education and PM&C would benefit from reviewing the number of indicators to improve the meaningfulness of performance information provided to the Parliament and the public. Both entities have reduced the total number of performance indicators presented in their 2018–19 corporate plans and PBSs.

Table 3.1: Assessment of the selected entities’ performance information hierarchy

|

AGD

|

4

|

2

|

2

|

4

|

12

|

|

DFAT

|

0

|

3

|

4

|

6

|

13

|

|

Education

|

3

|

27

|

8

|

5

|

43

|

|

PM&C

|

6

|

15

|

8

|

8

|

37

|

|

Total

|

13

|

47

|

22

|

23

|

105

|

| |

|

|

|

|

|

Source: ANAO analysis, as provided to entities during the progress of the audit.

3.29 The 13 performance criteria that addressed the management level of the hierarchy were excluded from the ANAO’s assessment for appropriateness in the following section. These measures were excluded as they would not significantly change an assessment of the entity’s performance, and in turn are not expected to significantly influence the decision making of the Parliament or public.

Appropriateness of entities’ performance criteria

3.30 As demonstrated by Figure 1.1, the PBS and corporate plan are the originating sources of an entity’s performance criteria. The corporate plan is also expected to ‘set the foundations upon which a reliable performance narrative can be built’, and appropriate performance criteria assists an entity in meeting this expectation.

3.31 Guidance from Finance notes that ‘appropriate’ performance information is ‘relevant, reliable and complete’. The ANAO assessed the selected entities’ performance criteria for these characteristics. The basis for this assessment is drawn from the characteristics of ‘good’ performance information as defined by Finance. The detailed criteria can be found at Appendix 5.

3.32 A summary of the ANAO’s assessment of whether the characteristics of ‘relevant’ and ‘reliable’ and ‘complete’ were suitably addressed by the selected entities’ performance measures is presented in Table 3.2. The scale used to rate the performance measures was:

- displayed all of the characteristics of the criterion (Yes);

- displayed most of the characteristics of the criterion (Mostly);

- displayed in part the characteristics of the criterion (Partly); and

- did not display the characteristics of the criterion (No).

3.33 Each of the entities’ performance criteria require improvement to fully meet the characteristics of relevant, reliable and complete. The majority of performance criteria were relevant, or mostly relevant, however most did not meet the reliability criterion and require improvement. The completeness of performance criteria is also a particular area requiring improvement, including developing measures of efficiency, and demonstrating an entity’s intended progress across the life of the corporate plan and beyond.

Table 3.2: Summary of ANAO assessment of the appropriateness of the selected entities’ performance criteria

|

AGD

|

Mostly

|

Mostly

|

Partly

|

|

DFAT

|

Mostly

|

No

|

Unable to determine

|

|

Education

|

Mostly

|

Partly

|

Mostly

|

|

PM&C

|

Mostly

|

Mostly

|

Partly

|

| |

|

|

|

Source: ANAO analysis.

Relevant — benefit, focus and understandable

3.34 In applying the ‘relevant’ criterion, the ANAO assessed whether each of the selected entities’ performance measures under review:

- clearly indicated who benefited and how they benefited from the entity’s activities;

- was focused on a significant aspect/s of the entity’s purpose/s, via the activity/ies, and the attribution of the entity’s activities to it is clear; and

- was understandable, that is, it provided sufficient information in a clear and concise manner.

3.35 More than three quarters of the selected entities’ performance measures were assessed as either demonstrating all, or most of, the characteristics of relevance. The summarised results of the ANAO’s assessment of the relevance of the selected entities’ performance measures are presented in Table 3.3.

Table 3.3: Summary of ANAO assessment of the relevance of the selected entities’ performance criteria

|

AGD

|

2

|

4

|

2

|

–

|

8

|

|

DFAT

|

4

|

7

|

2

|

–

|

13

|

|

Education

|

24

|

13

|

3

|

–

|

40

|

|

PM&C

|

15

|

5

|

2

|

9

|

31

|

|

Total

|

45

|

31

|

11

|

9

|

92

|

| |

|

|

|

|

|

Source: ANAO analysis.

3.36 For AGD, DFAT and Education, the majority of measures were either relevant or mostly relevant. Where the measures did not fully meet the characteristics of relevance, it was more commonly the result of the measure not adequately defining the beneficiary or benefit intended to be delivered, or not reflecting a significant aspect of the purpose.

3.37 Nine, or one-third, of PM&C’s performance criteria were assessed as not relevant. This was the result of measures not adequately fulfilling any of the characteristics of benefit, focus or understandability. For example the measure ‘At least 70 per cent of funded activities within this program met the mandatory KPI on the extent of compliance with Project Agreement terms and conditions’ does not make clear the beneficiary or benefit. It is not clear if it is Indigenous Australians, or PM&C and the government, receiving the benefits associated with compliance. This also affects a reader being able to determine whether the measure significantly addresses the purpose of improving the lives of Indigenous Australians (focus), or understand the intended result (understandable). The same measure was repeated for five Outcome 2 PBS programs.

Reliable — measurable and free from bias

3.38 In applying the ‘reliable’ criterion the ANAO assessed whether each of the selected entities’ performance measures under review were accompanied by sufficient information in the corporate plan, or PBS, to be:

- measurable, that is, it used and disclosed information sources and methodologies (including a basis or baseline for measurement or assessment, for example a target or benchmark) that were fit-for-purpose; and

- free from bias, allowing for clear interpretation and an objective basis for assessment of the results.

3.39 Compared to relevance, a far higher proportion of the selected entities’ performance measures did not meet, or only partly met, the characteristics of reliable, as the information presented in the corporate plan was insufficient for readers to form a view of the expected performance of the entity. The summarised results of the ANAO’s assessment of the reliability of the selected entities’ performance measures are presented in Table 3.4 below and accompanied by further commentary for each entity.

Table 3.4: Summary of ANAO assessment of the reliability of the selected entities’ performance criteria

|

AGD

|

4

|

2

|

–

|

2

|

8

|

|

DFAT

|

1

|

–

|

–

|

12

|

13

|

|

Education

|

14

|

1

|

22

|

3

|

40

|

|

PM&C

|

2

|

15

|

6

|

8

|

31

|

|

Total

|

21

|

18

|

28

|

25

|

92

|

| |

|

|

|

|

|

Source: ANAO analysis.

3.40 Finance guidance states a corporate plan should include a description of performance measures, when they will be reported on, the data collection techniques to be used and any targets the performance measures will be assessed against. This information can then be used by the Parliament and the public to assess the results presented by the entity in its performance statements at year-end.

3.41 This does not necessarily mean an entity needs to describe in intricate detail every element of the method of assessment or methodology to be applied. However, there should be sufficient information for a reader to make an assessment of the reliability of that method and the intended result. The method should also be underpinned by appropriate internal quality frameworks, developed contemporaneously, that support the reliability of the reported result.

3.42 For example, a corporate plan may set out a criterion and accompanying target and/or baseline that intends to measure the satisfaction of a particular stakeholder cohort. To fully address the requirements, the corporate plan would note that the method of assessment is an annual survey conducted by a qualified survey provider. This would be further supported by the entity’s internal policies and procedures for the engagement of that provider and delivery of the survey, including quality assurance mechanisms that provide confidence in the reported result.

3.43 Finance guidance notes the minimum content for corporate plans includes the planned performance of the entity including ‘details of the methodology, data and information that it will use to measure and assess its performance’. It is important for a reader to be able to understand the basic methodology supporting a measure for them to determine whether it can be relied upon.

Attorney-General’s Department

3.44 This was not demonstrated by four of the eight AGD performance measures assessed by the ANAO. For example, the performance measures ‘Civil justice policy advice, program work and legislative changes’ and ‘Policy advice, program work and legislative changes’ have the same target which is ‘Work is completed on time, within budget and in compliance with relevant guidelines’.

3.45 The broadness of the measure and targets means a reader is unable to determine what the intended result is to then enable an assessment against that expectation at year-end. The data collection technique is also not disclosed to enable a reader to determine whether it is fit for purpose or verifiable. The data collection technique was also absent from the two performance measures of stakeholder satisfaction.

3.46 An absence of targets, and/or only setting static targets, limits the ability of a reader to understand what an entity is aiming to achieve, and how incremental progress against that aim is expected to be measured over time. As noted above, the target ‘Work is completed on time, within budget and in compliance with relevant guidelines’ is used for two measures. Given there are three different assessments noted (time, cost and compliance), without a clear assessment method and defining the parameters of the assessments a reader cannot form an expectation of what ‘on time, within budget and in compliance’ looks like in advance, and as a result determine the potential for bias in either the expected, or reported, results.

Department of Foreign Affairs and Trade

3.47 Of the measures assessed, only one of DFAT’s performance measures demonstrated the characteristics of ‘measurable’. Six were intended to be measured through case studies, two planned reliance on reviews and two did not state a specific measurement method (those presented in the PBS).

3.48 As noted in paragraph 3.40, an entity’s corporate plan should describe the methodology and data intended to be used to measure performance. The department did not define, or provide the parameters for the case studies or reviews. This is demonstrated by the following measure:

Review the effective implementation of Australia’s FTAs, including commercially meaningful outcomes resulting from the General Review of the Association of Southeast Asian Nations (ASEAN)-Australia-New Zealand FTA (AANZFTA) and reviews of Australia’s bilateral North Asia FTAs.

3.49 Without the scope of the review, targets, benchmarks or timeframes, the reader is not informed of what constitutes ‘effective implementation’, or ‘commercially meaningful outcomes’, and how a conclusion about this will be formed. Furthermore, due to the use of the word ‘including’, it was unclear if the assessment of ‘commercially meaningful outcomes’ would be limited to the subset of FTAs mentioned, or all FTAs.

3.50 Consistent with the assessment for ‘measurable’, only one of the performance measures was determined to be ‘free from bias’. Without adequate disclosure of the basis for measurement, the potential for bias cannot be ruled out. For example, the measure of DFAT’s ‘whole-of-government coordination and leadership to advance Australia’s interests internationally’ is open to different interpretations. The absence of clear definitions for these terms — ‘coordination’ and ‘leadership’ — could lead to the result being biased towards a more favourable outcome, and it is unclear what conditions would lead to the measure not being met.

3.51 DFAT’s reliance on case studies and reviews, selected ex-post, provides further potential for bias. Where used, case studies can provide context to the department’s activities and achievements. However, case studies should not be relied upon as a stand-alone measurement, unless the scope is predetermined, activities clearly stated and measurement methods detailed in advance. The expected impacts can then be considered by readers in advance, and progress towards outcomes assessed on the basis of results, particularly in relation to the completeness of the reporting against program objectives.

Department of Education and Training

3.52 Education described the methods of assessment for measures in the corporate plan at a basic level, for example ‘qualitative assessment’ or ‘reporting’. Without being specific as to the method of measurement that will be used, a reader cannot reliably determine what will be measured, or whether reported results can be relied upon to assess Education’s progress in meeting its purposes.

3.53 Similarly, a number of PBS measures did not adequately describe the method of assessment that was intended to be used to determine the results. The department would benefit from providing further detail to assist a reader in better understanding and assessing the reliability of the information sources intended to be used to support its performance reporting.

3.54 Education has presented accompanying targets for all measures presented in the corporate plan and PBS. The use of targets provides some indication to a reader of the intended result, and provides a basis for comparing expected and actual performance, improving the reliability of the measures. However, there are opportunities for the department to further improve the reliability of measures and targets by better defining the parameters or benchmarks that would be used to assess performance.

3.55 For example, for the target ‘Eligible services and families transition from the Community Support Program and Budget Based Funded programs to new arrangements’, it is unclear whether the transition of all, some, or a proportion of, eligible services and families transitioning would see the target assessed as having been met.

3.56 Similarly, using language such as ‘ready to…’ when describing an intended result doesn’t provide a reader with sufficient understanding of the parameters that will be applied by the department when determining whether the target was met or not. For example, ‘Community Child Care Fund grants program is ready to start on 2 July 2018’ — does this mean the grant program is ready to accept submissions on 2 July 2018, all submissions are received by this date for assessment, or all recipients have been approved and payments will commence from 2 July. Without providing this specific detail, there is a potential for bias in the reported result as the reader has been unable to set an expectation against which to assess the department’s reported result.

Department of the Prime Minister and Cabinet

3.57 The design of some of PM&C’s measures provided an indication of the measurement method intended to be used, such as ‘feedback’ or ‘responses to request for briefs’. More commonly, PM&C has presented multiple methods without defining the particular one intended to be used. This is best demonstrated by ‘Use of case studies, independent panels or providers that show…’, which is repeated against multiple measures in the corporate plan. Without being specific as to which method of measurement will be used, a reader cannot reliably determine what will be measured, or whether reported results can be relied on to assess PM&C’s progress in meeting its purposes.

3.58 Of the 22 performance criteria presented in PM&C’s corporate plan, only six present accompanying targets. As noted earlier, the absence of a specific target affects a reader’s ability to determine the potential for bias in the reported result. This is demonstrated by PM&C’s performance criterion ‘Feedback from the Prime Minister, portfolio ministers, the Cabinet, ministerial officers and the Executives shows a high level of satisfaction with the quality and timeliness of advice received’. A ‘high level of satisfaction’ was not defined, and no accompanying target presented, in the corporate plan. As a result, PM&C could decide what constituted a ‘high level of satisfaction’ at any point up to publishing the performance statements, increasing the potential for bias.

3.59 PM&C provided targets for all measures presented in its 2017–18 PBS (nine), as required by the Department of Finance Secretary’s Direction. However the PBS is only required to present one high-level indicator for each existing program, and cannot be relied upon to present a complete picture of an entity’s performance. As a result, targets should also be presented against performance criteria in PM&C’s corporate plan to improve the reliability of measures.

Recommendation no.2

3.60 Entities improve the reliability of performance measures presented in their PBSs and corporate plans, by providing the Parliament and the public with information on the information sources and methodologies intended to be used to measure their performance. This information should be sufficient to enable a reader to make an assessment of the reliability of those methods, and develop an understanding of the intended result.

Attorney-General’s Department response: Agreed.

3.61 Following feedback from the ANAO during this audit, a section on methodology has been included in our 2018–22 Corporate Plan. We will continue to pursue improvements in the reliability of performance information presented in our annual performance statements to assist readers to understand the intended results.

Department of Education and Training response: Agreed.

3.62 The Department of Education and Training will publish additional information on its information sources and methodologies for performance measures in future corporate plans.

Department of Foreign Affairs and Trade response: Agreed.

Department of the Prime Minister and Cabinet response: Agreed.

Completeness — collective and balanced

3.63 The PGPA Act requires accountable authorities to govern their entities in a way that promotes the proper use and management of public resources, which is defined by the Act to mean efficient, effective, economical and ethical, and to measure and assess the performance of the entity in achieving its purposes. The Act also requires entities to provide meaningful information to the Parliament and the public to assist it in understanding how entities are performing, and how they are using the resources that have been entrusted to them.

3.64 This is fulfilled by entities meeting the requirements for corporate plans to include statements of how the entity will achieve its purposes, and how they will be measured and assessed, the results of which are reported in the entity’s performance statements. This requires the inclusion of relevant measures demonstrating the proper use of resources in achieving the entity’s purposes in the corporate plan.

3.65 Finance guidance outlines the critical considerations for developing good performance information include using an understanding of an entity’s purposes to identify a set of measures that demonstrate the extent to which those purposes and activities are being delivered efficiently and effectively. As it is rare for a single measure to be able to adequately determine the effectiveness of an activity, Finance guidance advises that good performance information will draw on multiple sources and the quality of performance information should be emphasised over quantity. The guidance recommends a small set of measures that is sufficiently comprehensive to cover those factors that affect an entity’s performance.

3.66 The guidance also notes that in some cases, effectiveness may not be measurable, due to cost or a lack of complete information. In these cases, other measures may be used as proxies for effectiveness. Entities are advised that in these circumstances, they should be clear on why effectiveness cannot be measured and how the proxy measures are suitable. Finance notes that activities often work on different timeframes, and information on one or more timeframes may not be available at the time of reporting. It is therefore recommended that the performance story reflect the outcome that can be reasonably expected from the relevant activities at that time.

3.67 In assessing the selected entities’ performance criteria for completeness, the ANAO considered whether the performance criteria present a basis for a collective and balanced assessment of the entity against its purpose. In particular, the ANAO considered whether the selected entities’ performance criteria:

- collectively address the entity’s purpose through the activities identified in the corporate plan (collective);

- provide a basis for assessment of the efficiency and effectiveness of the entity in fulfilling its purpose either directly or through the use of proxies (balanced);

- relied on a mixture of quantitative and qualitative measurement bases (balanced); and

- assess a mixture of short, medium and long-term objectives (balanced).

3.68 None of the four entities presented measures of efficiency in their 2017–18 PBSs or corporate plans. As noted above, entities should identify a set of measures that demonstrate both efficiency and effectiveness. This is to support the Parliament and the public in the assessment of how well Commonwealth entities are performing, including how they are using the resources that have been entrusted to them.

3.69 With the exception of Education (refer paragraph 3.82), entities are also not realising the full potential of the minimum four year horizon of the corporate plan, by developing performance measures that assess a mixture of short, medium and long-term objectives. Commonly, where targets were set by an entity they were constant across the four years of the corporate plan and assessed as short-term measures as a result. A users’ understanding of an entity’s proposed performance would be enhanced by including in the corporate plan a description of an entity’s rationale for setting targets. In particular, where the target has been historically met, or is static across the corporate plan, and how incremental improvement is expected to be demonstrated over time.

Attorney-General’s Department

3.70 Most of AGD’s performance measures were able to be aligned to the activities outlined in the corporate plan, providing a collective basis for assessing progress against the purpose. In reviewing the alignment between the key activities presented for Strategic Priority 3 and 5 and accompanying performance criteria, the broad description of measures required a reader to assume the connection to the activities.

3.71 For example, ‘Civil policy advice, program work and legislative changes’ does not explicitly demonstrate alignment to ‘develop and implement reforms to the family law system’, or ‘undertake international parental child abduction casework’, however it is reasonable to assume a reader would make this connection, due to the proximity of information on the activities. There would be benefit in AGD considering how the presentation of performance criteria may be improved to more specifically address its key activities and collectively improve their completeness.

3.72 AGD presents four different categories of ‘KPI’ in its corporate plan: ‘effectiveness’, ‘efficiency’, ‘professionalism, skills and commitment’ and ‘impact’. The measures presented against the ‘effectiveness’ (stakeholder satisfaction) and ‘impact’ (Rule of Law Index) KPIs have been designed to reflect its categorisation — either effectiveness or impact. The measures categorised as ‘efficiency’ KPIs do not reflect measurements of efficiency, rather the activities or outputs of the department. For example, the measures ‘justice policy advice, program work and legislative changes’ and accompanying targets ‘Work is completed on time, within budget and in compliance with relevant guidelines’ are not measures of efficiency as presented. The remaining measures also considered activities or outputs of the department.

3.73 The majority of AGD’s performance measures are qualitative in nature (four of seven). Observations made in regard to the reliability of AGD’s measures in the previous section also impacted an assessment of whether they represented qualitative or quantitative information. The only quantitative measures were those presented in the PBS for Program 1.9. The department would benefit from considering whether this mix is appropriate.

3.74 None of AGD’s measures under Strategic Priority 3 or 5 presented targets across the four years of the corporate plan. All measures instead presented a target, without an explanation of whether they applied to all, or only some, of the future years of the corporate plan. The measures were assessed as short-term as a result. AGD would benefit from reviewing how to demonstrate to readers the expected timeframes of activities, and expected incremental progress over the forward years, through its performance measures.

Department of Foreign Affairs and Trade

3.75 Overall, it is unclear whether the performance measures presented in DFAT’s corporate plan and PBS for Priority Functions 1 and 2 provide a complete basis to assess the department’s progress in achieving these priority functions. Most of DFAT’s major operational activities were able to be mapped to an accompanying performance measure, however it could not be determined whether these presented a complete picture of performance.

3.76 This was largely due to the absence of clear methods of assessments as noted in paragraphs 3.47 to 3.51. As a result, the measurement basis and/or timeframe for four of the 13 measures assessed could not be determined. For example DFAT noted it would use case studies to assess:

‘Our promotion and protection of Australia’s economic interests in bilateral, regional, multilateral and plurilateral outcomes’

3.77 No further information about the focus, type or number of case studies intended to be used to assess the performance criterion was provided. As a result it could not be determined whether the basis for assessment would be qualitative, quantitative or a mixture of the two. As noted above, this also influenced an assessment of the extent to which the criterion would address DFAT’s activities.

3.78 Of those that had sufficient information, there appeared to be a mixture of type and bases — effectiveness, activity and output and qualitative and quantitative. However, none presented in Priority Function 1 or 2 were determined to measure the department’s efficiency. Two measures were also presented that were relevant to 2020–21, reflecting a medium term outlook, however the remainder appeared to be an annual assessment.

Department of Education and Training

3.79 Education’s purpose is ‘maximising opportunity and prosperity through national leadership on education and training’, however, there are no measures that seek to demonstrate the department’s ‘national leadership’. Similarly, while all of Education’s measures were able to be mapped to an activity in the corporate plan in some way, none appeared to fully address the activity ‘Strengthening the national evidence base and lifting outcomes in Australian schools’. The activity’s accompanying delivery strategies listed a number of key actions of the department, including:

- Contributing to national policy on the most effective teaching and learning strategies; and

- Leading efforts to improve our national education evidence base and data for schools and preschools.

3.80 While a number of measures appear designed to measure ‘lifting outcomes’, none provided an assessment of the department strengthening the national evidence base, or contributing to national policy. The department would benefit from considering how this may be addressed in future reporting periods to collectively improve the completeness of their measures.

3.81 The majority of Education’s corporate plan criteria measure effectiveness, while the PBS criteria largely address activities and/or outputs. None of Education’s performance measures address the department’s efficiency. The group of performance criteria also provide a balance of qualitative and quantitative information, however there were some measures where the measurement basis could not be determined due the method for assessment not being clear.

3.82 The department has also presented a balance of short, medium and long-term measures. In particular, the corporate plan presents the department’s planned progress over the four years of the corporate plan for particular activities. For example, for the criteria ‘Capacity and capability of child care services to include children with additional needs’, the department has an accompanying target for 2018–19 of ‘establish baseline data through new reporting tool’. The final two years of the corporate plan then both present the target of ‘Improved inclusion for children with additional needs’. Showing the progression of the department’s intended measurement over the life of the corporate plan provides the reader with a more holistic understanding of what the department is aiming to achieve, and the steps being taken in the short term and medium term to do so.

Department of the Prime Minister and Cabinet

3.83 PM&C’s corporate plan clearly outlines activities with accompanying performance criteria and measurements. Overall, the activities, criteria and measurements collectively address the department’s purposes.

3.84 More than half of PM&C’s criteria measure effectiveness, while the remaining criteria measure outputs or activities. None of PM&C’s criteria measure efficiency. The following criterion was presented in the department’s 2017–18 PBS, ‘Efficient department support to the six Indigenous Advancement Strategy programs’ and the accompanying target of ‘At least 70 per cent of key performance measures in the Corporate Plan are met or are on track’, however it is unclear how the accompanying target is intended to demonstrate the department’s efficiency.

3.85 The group of performance criteria provides a balance of qualitative and quantitative information, however, as noted in paragraph 3.58, in most cases no targets have been set against the performance criteria in the current year, or in the future periods covered by the corporate plan. As a result, all performance criteria were assessed as only addressing the short-term timeframe. The exception was the COAG target ‘Halve the gap for Indigenous students in year 12 (or equivalent) attainment rates by 2020’ which addresses the medium term.

Recommendation no.3

3.86 Entities review their performance measurement and reporting frameworks to develop measures that also provide the Parliament and public with an understanding of their efficiency in delivering their purposes.

Attorney-General’s Department response: Agreed with qualification.

3.87 The department is committed to supporting the Parliament and the public in assessing how well Commonwealth entities are performing, including how they are using the resources that have been entrusted to them. Identifying appropriate and cost-effective efficiency measures for policy development can be a complex matter.

3.88 The Department of Finance’s RMG 131 Developing good performance information defines efficiency as the unit cost (such as in terms of dollars spent or human resources committed) of an output (for example, a service) generated by an activity, stating that an activity is most efficient when the unit cost of delivering an output at a given quality is a minimum. Similarly, the ANAO’s recent Insights from reports tabled July to September 2018 suggests that in developing a set of measures to consider efficiency, it can be helpful to compare input to output ratio over time or to identify a suitable comparator. We note there are a range of challenges in this regard, including:

- attributing the impact of policy outcomes in complex environments

- measuring potentially intangible outputs (feelings of safety, understanding of how to access services, confidence in business dealings)

- that policy development is not always linear with a clear beginning, middle and end

- the ongoing impact of innovation, particularly in the digital space

- that agencies do not control all elements of the policy cycle, and

- identifying suitable comparators noting the breadth and diversity of policy matters within and across agencies.

3.89 We also acknowledge that many of these issues have been raised previously in the performance context, but it is important to note that this is still an area of development. We caution that simply using a unit cost calculation to demonstrate policy development efficiency may generate a misleading result and that identifying a suitable comparator in an increasingly complex environment will often be difficult.

3.90 Noting the above, we will continue seeking out examples of best practice and exploring a greater mix of measure into the future to reflect our efficiency in achieving our purpose.

Department of Education and Training response: Agreed.

3.91 The Department of Education and Training will incorporate this focus in its forward looking review of its performance measurement and reporting framework.

Department of Foreign Affairs and Trade response: Agreed with qualification.

3.92 The department agrees in part to Recommendation 3. We agree that efficiency measures, although challenging to develop, are useful, especially with respect to program and service delivery. The department agrees to review our measures and frameworks with this in mind. We note that the development of meaningful measures in policy performance is nascent across the Australian Public Service, especially with respect to efficiencies. As such, the department will work closely with the Department of Finance and other policy entities to consider options for new efficiency measures.

Department of the Prime Minister and Cabinet response: Agreed with qualification.

3.93 We agree that efficiency measures, although challenging to develop, are useful, especially with respect to program and service delivery. Noting that it is difficult to frame meaningful measures that are both insightful to readers of the Annual Report and PM&C operations, as well as cost effective to implement, PM&C will continue to work closely with the Department of Finance and the ANAO to identify suitable measures.

Have the selected entities made improvements to their proposed performance measurement and reporting for 2018–19?

PM&C’s 2018–19 Corporate Plan provides the Parliament and the public with limited insight into how the department intends to measure its performance compared to 2017–18. The remaining entities have made changes to their 2018–19 corporate plans which provide an improved basis for performance measurement and reporting. However, Education would benefit from reintroducing activities to its 2018–19 Corporate Plan that describe what the department does, or intends to do.

3.94 An entity is required to publish a corporate plan, relevant to the current and three future reporting periods, by 31 August each year. Subsection 16E(6) of the PGPA Rule also allows an accountable authority to vary an entity’s corporate plan at any time. Finance guidance provides examples of circumstances where an accountable authority may wish to do so including ‘new activities that warrant inclusion in the corporate plan; significant new performance criteria, targets or tools that will be used to measure or assess performance; and key changes in the capability of the entity or in its risk management approach’.

3.95 The timing of this audit provided an opportunity to review the selected entities’ 2018–19 PBS and proposed corporate plans to identify any further opportunities for improvement to the performance measurement and reporting. The ANAO provided each entity with feedback during the course of the audit that could then be used in the entities’ development of the 2018–19 Corporate Plans.

3.96 Each of the entities improved elements of their corporate plans in some way by addressing ANAO feedback, or matters already highlighted through the entities’ own improvement processes. Specific elements of Education’s and PM&C’s 2018–19 corporate plans, when compared to the previous year, do not provide an improved basis for performance measurement and reporting.

3.97 AGD incorporated feedback provided by the ANAO during this audit to improve its 2018–19 Corporate Plan, including:

- adding a section for methodology that describes the different sources that support the performance information and how it is collected;

- including a performance measure in the corporate plan focused on the departments’ work in regard to royal commissions; and

- presenting targets across the four years of the corporate plan.

3.98 Similarly, DFAT improved its corporate plan by mapping performance measures to specific delivery strategies, and presenting more succinct and understandable descriptions of the priority functions, which assisted the reader to understand the type of work that DFAT undertakes. These were also supported by the identification of DFAT’s delivery partners for each priority function. A new feature of the 2018–19 Corporate Plan was the inclusion of a table for each priority function, which listed the relevant PBS programs for that priority function. This establishes an alignment between the PBS and corporate plan at a high level.

3.99 Further improvements could still be made by AGD and DFAT to their performance measures to fully meet the characteristics of ‘relevant’, ‘reliable’ and ‘complete’. However, the changes made by both entities to the 2018–19 Corporate Plans provide an improved basis for performance measurement and reporting.

Department of Education and Training

3.100 Education provided its 2018–19 Corporate Plan to the ANAO on 21 August 2018. The department published the corporate plan on its website on 24 August 2018.

3.101 In reviewing the 2018–19 Corporate Plan, there are areas where improvements had been made by the department, including seeking to better describe the key elements of its purpose. This was achieved through the introduction of ‘themes’ that sought to explain what ‘maximising opportunity and prosperity’ meant. For example ‘Access and participation — everyone in Australia has access to and opportunity to participate in quality education’.

3.102 A ‘National Leadership’ section has also been introduced which outlines five key areas where the department intends to deliver national leadership. These included areas such as policy excellence and relationships and networks and collaboration. However, in reviewing the performance measures presented in the 2018–19 Corporate Plan, this particular aspect of the department’s purpose is still not reflected.

3.103 An area where the department’s corporate plan has not improved is in regard to its activities. As noted in paragraph 3.13, the activities presented in Education’s 2017–18 Corporate Plan could have more clearly described the specific actions the department is undertaking to pursue its purpose. The 2018–19 Corporate Plan no longer presents activities. The ‘Sustainability and Efficiency’ theme goes some way by discussing the department’s funding initiatives and compliance arrangements, however the others are presented as detailed objectives, providing only a very broad indication as to what the department intends to do to fulfil its purpose.

3.104 Finance guidance acknowledges that a corporate plan does not need to describe everything an entity does, however it recommends that ‘It should focus on the high-level activities through which the results captured by its performance frameworks are achieved. A discussion of activities should provide a reader some insight and understanding of how purposes are pursued.’ In the absence of key activities, a reader is left with a limited understanding of what the department will do to fulfil its purpose. It is also difficult to determine whether the measures presented will be representative of Education’s performance.

3.105 In responding to the above, the department noted that the activities had not been focused on early enough in the planning process with the senior leadership team, and it was decided that the previous year’s activities would not roll forward into the 2018–19 Corporate Plan. Instead the themes noted above were used, which better link to the department’s purpose, with the intention of presenting activities under these headings in the future. The department acknowledged that this approach ‘comes at the expense of clear attribution re-how we achieve this purpose’.

3.106 The ANAO notes the department’s ongoing efforts to improve its performance measurement and reporting. However, 2018–19 is the fourth year of the Commonwealth performance framework, and it is expected that entities have by now embedded adequate processes to support the timely consideration and development of their corporate plan.

Department of the Prime Minister and Cabinet

3.107 PM&C provided its 2018–19 Corporate Plan to the ANAO on 27 August 2018. The department published the corporate plan on its website on 31 August 2018.

3.108 The mission and purposes of the department have not changed in the 2018–19 Corporate Plan. As noted in paragraph 3.7, the department’s purposes are activity-based, with the exception of Purpose 3, and do not reflect the intended result. The mission on the other hand contains these characteristics and better describes the department’s ‘purpose’ as required by the framework. Reviewing the presentation of PM&C’s mission and purposes, and making clear the intended relationship between these elements in the corporate plan, would assist a users’ understanding.

3.109 When comparing the ‘Purposes’ sections between the two corporate plans, the 2018–19 plan provides clearer, and more concise, descriptions of the role/activities of the department. This has improved the readability of the corporate plan, and assist a reader’s understanding of what the department actually does when it refers to ‘support’ or ‘provide advice’.

3.110 The performance section of the 2018–19 Corporate Plan has also been changed by the department and is presented on a single page — a significant reduction compared to the eight pages of the 2017–18 Corporate Plan. However, this has not led to an improvement to the appropriateness of the performance criteria.

3.111 The 16 key performance indicators and accompanying 27 measurements presented in the department’s 2017–18 Corporate Plan have been replaced by the following five ‘assessment’ points:

- the Australian Government relies on our expertise and innovative advice

- our advice is timely, of high quality and impactful

- the public service and key stakeholders capitalise on our whole of government perspective to best deliver priorities

- we achieve our objectives under key focus areas identified in this Corporate Plan

- our people demonstrate the qualities articulated under our four pillars of transformation.

3.112 Given the measures are presented at a high level, their relevance to the department’s purposes, when considered alongside the activities, is demonstrable in most circumstances. However, the reliability of the measures is limited. The measures are accompanied by a footnote that states assessments are measured annually, and lists a number of methods. As noted in paragraph 3.57, by referencing multiple potential assessment methods, readers are unable to determine the standard against which the department’s performance is to be measured. As a result, there continues to be limited insight for a reader as to how the department will demonstrate its performance.

3.113 In addition, without knowing the specific measures that will be used to measure performance, a reader cannot determine whether the corporate plan enables a complete assessment of the department’s intended performance. For example, for the measure ‘We achieve our objectives under key focus areas identified in this Corporate Plan’, there are 22 key focus areas across the three purposes, the majority of which are framed as ongoing departmental objectives.

3.114 Within the focus areas and the measure there is no indication of timeframes for achievement, including how, and whether all or only some of, the focus areas will be reported against each year. There is also no longer an indication of the measurement bases to determine a balance of quantitative versus qualitative information, and no demonstration of progress/improvement over time as the points are described as being measured annually — presenting a static view across the four years of the corporate plan.

3.115 As noted in paragraph 3.30, the role of the corporate plan is to ‘set the foundations upon which a reliable performance narrative can be built’. To fulfil this role, it is important that a corporate plan provides a reader with a clear basis from which to set an expectation of an entity’s performance. PM&C’s 2018–19 Corporate Plan does not sufficiently fulfil this requirement and should be reviewed by the department.