Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 43 of 2008–09

Construction of the Christmas Island Immigration Detention Centre

Published

Tuesday 23 June 2009

Portfolio

Finance & Deregulation

Entity

Department of Finance and Deregulation

Sector

Attorney-General's

Finance

Immigration

The objective of the audit, in examining the construction of the CIIDC, was to assess:

- the adequacy of the planning and delivery processes for the project;

- the value-for-money achieved in the delivery of the project, including with regard to the suitability of the centre for its intended purpose; and

- the extent to which the Public Works Committee Act.

Summary

Introduction

In the latter part of 2001 several measures were introduced to address an increase in unauthorised arrivals to Australia. These measures included legislation excising Christmas Island, Ashmore and Cartier Islands and Cocos (Keeling) Islands from the migration zone for the purposes of unauthorised arrival as well as arrangements for the reception and accommodation of unauthorised boat arrivals and the processing of their claims for protection at various offshore locations.

In addition, on 11 March 2002, the Government decided to proceed urgently to construct a new purpose built permanent Immigration Reception and Processing Centre1 on Christmas Island, together with the construction of essential infrastructure associated with the construction and on-going operation of the Centre. In terms of project delivery:

- the then Department of Immigration and Multicultural and Indigenous Affairs (DIMIA)2 was to be responsible for the construction of the facility; and

- the then Department of Transport and Regional Services (DOTARS)3 was responsible for all associated infrastructure and headworks to support the facility, construction of staff housing in the Island's residential area and provision of the construction camp.

The project approved in March 2002 had been for a 1200 person facility to be built in 39 weeks for an indicative budget of $242.9 million. By June 2002, architects and a Construction Contractor had been appointed. However, delays in the project timelines and increases in project costs had begun to emerge. By September 2002, the project estimate had increased to $427 million with a delivery period in the order of 120 weeks.

After considering the work of a departmental taskforce as well as commercial and legal advice, in November 2002 the Government reaffirmed the need for the CIIDC project. However, following discussions with the appointed Construction Contractor, it was concluded that construction of a 1200 place purpose-designed and built facility could not be achieved within the budget, and it was decided to terminate the contract with the Construction Contractor.4 After considering options, on 18 February 2003, the Government decided to respecify the project to an 800 place facility at a forecast estimate of $276.2 million.

Respecified project

Prior to the termination of the original construction contract entered into by DIMIA, a fully operational construction camp had been built, and some land clearing bulk earthworks for the CIIDC facility had been undertaken.

At the time the project was respecified, responsibility for delivering the CIIDC facility was transferred from DIMIA to the Department of Finance and Deregulation5 (Finance), with a more conventional delivery method6 to be adopted in an endeavour to provide greater cost certainty. Responsibility for the provision of associated infrastructure remained with DOTARS. Finance was to manage the facility construction project from 19 February 2003 to completion, which was expected to take 34 months (that is, practical completion by December 2005). The budget of $276.2 million was allocated as follows:

- a facility construction budget of $197.7 million (referred to in this report as the Finance Budget Allocation);

- $58 million in budgeted costs for DOTARS to deliver housing and infrastructure works7 and resume the mining lease on which the CIIDC would be constructed (the DOTARS Budget Allocation); and

- $20.5 million in budgeted costs associated with DIMIA's management of the project up to the February 2003 transfer of responsibility to Finance. DIAC was allocated a further $3.1 million for project supervision and consultancies for the period from the February 2003 transfer of project management to Finance until project completion, but this allocation was not included in the $276.2 million figure. Collectively, these amounts are referred to as the DIMIA Budget Allocation.

In June 2003, the proposal to construct a respecified, purpose-built CIIDC was referred to the Public Works Committee (PWC) for its consideration. The PWC's December 2003 report recommended that the respecified project proceed at its estimated facility construction cost of $197.7 million.

A two-stage project delivery model was adopted by Finance for the remaining construction work for the CIIDC facility. The first stage was the ‘Early Works', which were carried out under a lump sum contract arrangement and involved bulk earthworks. The second stage was the ‘Main Works'.

The planned Main Works delivery strategy was to involve a modified lump sum form of contract that included a Guaranteed Maximum Price (GMP). GMP construction contracts are arrived at through a staged process that involves the construction tender being carried out prior to the completion of the design, and the Preferred Tenderer being involved in the final documentation of the design. Each party participating in the tender process is provided with construction drawings and specifications to a sufficient level of detail to allow them to submit a fixed price for the works based on the required dates for practical completion.

A three phase open tender process to appoint the Main Works Contractor was conducted between February and December 2004. Two tenders were received in August 2004, with prices of both tenders being above the available budget. As a result, the Finance Budget Allocation was increased by $59 million. The Main Works Contract was signed in January 2005, with a stated GMP of $207.9 million and a date for Practical Completion of 31 August 2006. A second budget increase (of $60 million) was obtained by Finance in August 2006, during the construction stage.

Practical Completion by the Main Works Contractor of the CIIDC occurred in October 2007. However, various deferred and additional works had to be completed by Finance (through its contracted Project Manager) in order to bring the facility to a ‘fit for purpose' condition such that it could be handed over to DIMIA. This handover occurred in April 2008. The estimated out-turn cost of the facility works is within the amended Finance Budget Allocation of $317.0 million.

The PWC Manual requires8 that, if there are significant changes to a project after it has been considered by the Committee and approved by the Parliament, proponent agencies are to report these changes and, if necessary, seek the Committee's concurrence. Finance advised the PWC of the budget increases in January 2008. In June 2008, the Committee announced that it would receive a briefing from Finance and DIAC on the development of the CIIDC, focusing on the increase in the total budget from $276 million in 2003 to $396 million. After a public briefing was held in June 2008, the PWC wrote to the ANAO advising that it had concerns about the costing provided to it in September 2003, and the subsequent management of the project. ANAO advised the PWC that the audit of the project, which at that time was underway, would assess the rigour of the project estimates and budgets as well as the management of the project in terms of its cost, timing and scope.

Audit scope and objective

A performance audit of the CIIDC construction project was first included as a potential audit in ANAO's Planned Audit Work Program for 2006–07. As the project was not completed in 2006–07, the audit of the construction of the CIIDC was not commenced that year but was rescheduled as a potential topic in the 2007–08 Planned Audit Work Program.

The objective of the audit, in examining the construction of the CIIDC, was to assess:

- the adequacy of the planning and delivery processes for the project;

- the value-for-money achieved in the delivery of the project, including with regard to the suitability of the centre for its intended purpose; and

- the extent to which the Public Works Committee Act 1969 (PWC Act) and approved procedures have been complied with.

Audit Conclusions

The CIIDC was a more difficult construction project than many others undertaken by the Australian Government. It involved numerous challenges and risks including the isolation of Christmas Island, shipping being adversely affected by the swell season (which typically runs for five months from November to March), the absence of a wharf suitable for ships to berth alongside and the facility being constructed on reclaimed mining land that was surrounded by a National Park. In addition, the construction works were of considerable scale (the CIIDC facility comprises more than 50 buildings and associated landscaping works) with an ambitious design and delivery timetable, and a tight budget.

The CIIDC facility has been completed, has been accepted by DIAC as fit for its purpose and is now operational. However, this result has come at a considerably greater cost than budgeted at the time the project was respecified and over a substantially longer timeframe than had been expected. In this context, the audit has underlined several important messages for agencies to bear in mind when managing future construction projects.

The first is that it is only after sufficient scoping and planning work has been undertaken that reliable estimates and delivery timeframes can be established. The scope, budget and timeframe for the respecified project was established after nine months of detailed design work, market place investigation and cost reviews incorporating expert costing advice. Nevertheless, the revised delivery timeframe of 34 months (as opposed to 39 weeks for the original project) was exceeded by 27 months and Finance's Budget Allocation was increased by 60 per cent. Factors contributing to this outcome included that, at the time the respecified budget was approved, the design brief had not been finalised, a concept design had not yet been prepared and the revised budget included very little in the way of a contingency allowance for risk.

The second message relates to the importance of managing a project as a whole when individual agencies have separate budgets for sub-parts that are interdependent.9 For the CIIDC project, Finance was responsible for the facility construction aspect with DOTARS responsible for most of the infrastructure works necessary to connect the facility to the services on the Island, as well as for an upgrade of the Island's port crane. Early in the project, Finance consulted with DOTARS to ensure there were sufficient spare parts on the Island for the port crane (given its importance to project logistics) but Finance (and prior to February 2003, DIMIA) was not involved in DOTARS' decision-making processes relating to the construction of the additional port facility at Nui Nui, and the subsequent procurement of a new crane or the upgrade to the existing pedestal at Flying Fish Cove (due to the decision to relocate the existing, older, crane to Nui Nui). For budgetary reasons DOTARS decided to have the crane pedestal upgraded rather than a new pedestal constructed. The relatively modest initial saving in capital expenditure was more than offset by the effects on the facility construction project of the crane being taken out of service due to the discovery of major foundation faults in the pedestal.10 This example emphasises the importance of a whole-of-government perspective in such decisions by agencies.

Thirdly, it is important that agencies manage projects by developing and following delivery strategies that reduce identified risks to acceptable levels. There are a number of possible approaches to the development and delivery of Commonwealth capital works projects, each involving different risks and having advantages and disadvantages. To provide greater cost certainty given the original project had been respecified partly due to significant budget increases, Finance's chosen project delivery strategy was to involve the main works contract being tendered based on a detailed and developed design, and the contract being signed based on a completed design.11 The strategy was sound but was not followed. Instead, the design and tendering processes were overlapped and the design was not completed until some time after the construction contract was signed.12 The departures from the planned approach contributed to the project delays and increased costs to the Commonwealth.

To capture both industry and its own experience in managing construction projects, Finance has developed a better practice guide to the delivery of major capital works, which at the time of the audit was being updated. The first draft of this guide was introduced in July 2005, during the construction phase of the CIIDC project. Where the guide has adequately addressed matters identified by this audit as requiring attention, this has been recognised (in lieu of an ANAO recommendation being made). ANAO has made six recommendations relating to:

- greater emphasis being given in the management of construction projects to the requirement to provide the PWC with advice on the extent and nature of project uncertainties, and their potential effect on the project budget. This can assist agencies to meet statutory obligations as well as better manage Parliamentary expectations as to the likely project timing and out-turn cost. It addition, timely advice should be given to the Committee of significant project changes;13

- the importance of infrastructure works being effectively integrated with the facility construction work, particularly where different Australian Government agencies are responsible for the infrastructure and facility works;

- agencies working to implement planned project delivery strategies and, where departures are proposed, providing decision-makers with a comprehensive assessment of risks and how they can best be managed; and

- agencies measuring construction projects' performance, including through formal post-project ‘lessons learned' exercises, as this is central for ensuring that planned improvements in cost, time and quality are achieved, and for identifying potential for improved approaches.

Key Findings

Key Adviser Contracts (Chapter 2)

Finance engaged three key advisers to assist it deliver the CIIDC project: a Project Manager, a Principal Consultant (for design and construction services) and a Cost Manager.

The Project Manager engagement was particularly significant. An independent review of the original project commissioned in September 2002 had concluded that a Project Manager should be engaged to overview the project delivery, including the CIIDC facility, interface with the associated infrastructure provision and liaise with the Island community. Consistent with the outcome of this review, one of the first actions taken by Finance following the then Government's 18 February 2003 decision to respecify the CIIDC project and transfer delivery responsibility from DIMIA, was to commence the procurement process to appoint a Project Manager.

The Project Manager was appointed via a two-stage public tender process. The Project Manger was responsible for delivering the project in the time allocated and, in consultation with the contracted Cost Manager, at a cost no more than that allocated in the Project Cost Plan. The successful tenderer had been assessed as the best candidate against the qualitative evaluation criteria but was also the most expensive. Finance considered that, while the cost was more expensive than the next highest scoring tenderer, it was ‘highly likely' that the better resources would result in a superior project outcome for the Commonwealth.

When it was responsible for the original project, DIMIA had appointed an architect (the same firm that later became Finance's Principal Consultant14) and the Cost Manager. Finance continued with these engagements under the existing terms following the transfer of delivery responsibility from DIMIA to Finance.

Between June and October 2003, Finance's Project Manager negotiated a scope of work for both the Principal Consultant and the Cost Manager, and draft contracts were prepared. However, some eight months after taking responsibility for the project and five months after appointing its Project Manager, Finance then decided to undertake a sole-source tender process15 for the Principal Consultant and Cost Manager engagements based on its perspective that, while the existing arrangements could continue to be used on an hourly basis, better value for money could be achieved by a lump sum arrangement. The late decision to undertake a sole-source tender for the Principal Consultant engagement had an adverse impact on the design timetable for the facility.16

Delays were experienced with the finalisation and signature of the contracts with the Principal Consultant and the Cost Manager. For the Principal Consultant, contract negotiations extended from December 2003 to June 2004. The Principal Consultant proposed a substantial number of changes to the contract, many of which were agreed to by Finance and reflected in the contract that was signed in July 2004. The Cost Manager contract had been signed in June 2004. Each contract had a commencement date of July 2003.

Having regard to the timeframe requirements for approaches to the market under the current Commonwealth Procurement Guidelines and the greater emphasis now placed on open approaches to the market, for future projects it is unlikely Finance would have been able to adopt the procurement strategies used on the CIIDC project. In this respect, Finance advised ANAO that it is involved with an exercise being conducted by the Department of Defence (Defence) to establish panel arrangements for project management and other key resources needed by Defence to deliver construction projects. Other Commonwealth agencies will also be able to engage consultants from the Defence Infrastructure Panel.

The form of contract employed by Finance provided the advisers with no financial incentives for early completion of all necessary works, and included no financial penalty in situations where the project was delayed. The respective Contract Sums were varied in response to delays in the project given that resources were required to be deployed for a longer period and/or a change in scope that required an increased commitment of resources. As it eventuated, each adviser contract was amended a number of times to increase the total amount payable by Finance (by between 42 per cent and 230 per cent).17 Most of the increases for the key advisers related to extensions of time as a result of delays in developing and finalising the facility designs, as well as further delays with construction of the facility.18

In light of this experience, it will be important that Finance improve the contractual framework for key adviser appointments to future construction projects. In May 2009, Finance advised ANAO that, to provide incentives for timely completion of major capital works, it has introduced incentivised contracts into recent major projects such as the National Portrait Gallery.

Project governance (Chapter 3)

Key governance aspects of the respecified project included:

- an Interdepartmental Committee comprising Finance as Chair, DIMIA, the Department of the Prime Minister and Cabinet (PM&C), DOTARS, the Department of Employment and Workplace Relations (DEWR) and Environment Australia;

- a Memorandum of Understanding between Finance and DIMIA;

- a Project Control Group involving Finance, DIMIA, the Project Manager and Main Works Contractor (to provide the formal interface between Finance and DIMIA);

- the Project Control Group reporting to a Steering Committee that comprised senior DIAC and Finance officials; and

- fortnightly project implementation meetings comprising Finance and its Project Manager, Principal Consultant and Cost Manager.

In addition, a number of plans were prepared to guide the facility construction project. However, some of these plans were not maintained and updated throughout the project, or did not reflect all relevant project activities. There were also some gaps in the framework, including in relation to risk management. For example, an internal audit conducted between November 2007 and January 2008 found that risk assessments for the project were not updated with the frequency required by Finance's guidance.

Whole-of-Government budgeting and cost control

Australian Government consideration of the respecified CIIDC project was undertaken on the basis of a whole-of-project budget that included the costs of facility construction (managed by DIMIA in respect to the original project, and Finance for the respecified project), the cost of undertaking infrastructure works necessary for the Centre to be made operational (the responsibility of DOTARS) and DIMIA's ongoing involvement as the facility user.

In circumstances where there is more than one agency involved in the delivery of a project, one agency is undertaking the delivery of works on behalf of another, or funding is obtained from a number of sources, it is important that a comprehensive approach be taken to preparing the overall project budget, comparing estimates to the overall budget and accounting for the final (out-turn) cost. However, there was no authority for Finance and its Project Manager and Cost Manager to exercise any oversight or authority over the DIMIA and DOTARS Budget Allocations. DIAC's actual costs were $26.2 million. The final out-turn cost of the project is not known because DOTARS was not able to assemble information on its actual project-related costs. Had the cost management format covered all project expenditure as originally envisaged, it would have also established a clear and regular interface between the various agencies involved in the project, as well as providing for improved accountability, including to the PWC.

Interface between infrastructure works and facility construction works

It is important to the delivery of construction projects that there is an effective interface between the infrastructure and facilities works packages, as there can be areas of common risk as well as interrelationships between the two. In respect to the CIIDC project, the provision of the infrastructure works was an integral part of the overall project in connecting the CIIDC facility to the services on the Island—without the infrastructure works the facility would be unable to be constructed and operated.

However, a governance structure was not developed and implemented between Finance and DOTARS for the works being managed by DOTARS.19 This was notwithstanding Finance's documented risk assessments identifying the provision of utilities and support trades on the Island as a risk to be managed. For example, early in the project, Finance consulted with DOTARS to ensure there were sufficient spare parts on the Island for the port crane (given its importance to project logistics) but Finance (and prior to February 2003, DIMIA) was not involved in DOTARS' decision-making processes relating to the construction of the additional port facility at Nui Nui, and the subsequent procurement of a new crane or the upgrade to the existing pedestal at Flying Fish Cove.

DOTARS conducted a tender between February and April 2003 for a new (or near new) crane at Flying Fish Cove after the decision was made to relocate the existing, older, crane to the additional port facility at Nui Nui. The crane could be either a fixed ships cargo crane or a fixed tower crane, with the scope of work for the latter option involving the tower crane to be installed onto a new pedestal. However, for budgetary reasons DOTARS decided to have the crane pedestal upgraded rather than a new pedestal constructed (a new pedestal was estimated to cost $700 000 more than upgrading the existing pedestal). DOTARS also did not address, or discuss with Finance, the costs and benefits of constructing a new pedestal as a means of managing some of the logistical risks for shipping materials to the Island. Specifically, had a new pedestal been constructed, the existing pedestal could have been retained as a back-up platform in the event of problems with the new crane on a new pedestal.

The estimated savings of $700 000 realised by DOTARS in its budget were small given the importance of an operating port crane on the CIIDC facility construction project and the budget at that time for these works of $197.7 million. The initial saving in capital expenditure was more than offset by the effects on the facility construction project of the crane being taken out of service due to the discovery of major foundation faults in the pedestal. In this respect, ANAO has estimated a net delay effect on the project of one month and additional costs of $6.4 million.20

Facility design and construction (Chapters 4, 5 and 6)

In deciding to respecify the project and transfer delivery responsibility to Finance, the Government had been advised that re-tendering of the project on the basis of a detailed design and delivery of the project through a fixed price contract would provide greater costing certainty prior to construction commencing and address allocation of risk by integrating it into the price. Consistent with this advice, the Government decided that a more conventional delivery method should be adopted in an endeavour to provide greater cost certainty.21

Following its appointment in May 2003, Finance's Project Manager commenced the development of a project management framework. This included renegotiation of the architect's engagement to become a Principal Consultant engagement22 and Cost Manager engagements and development of a Communications Plan, a documented Brief and Design Endorsement Process and a documented Project Delivery Strategy.

The Project Manager's June 2003 Project Delivery Strategy report to Finance analysed various project delivery models/strategies that could be applied to the CIIDC project. It proposed that a GMP delivery method be adopted for the Main Works. The Project Delivery Strategy stated that:

This is a variation on the traditional lump sum form of tender. The Guaranteed Maximum Price provides the client with the least risk to out-turn cost. The contractor is required to deliver the project within the fixed time, cost, quality and scope as defined by the client. This includes the acceptance of risk for design errors and omissions. Therefore the contract sum cannot be varied unless the client requires a significant scope change.

The engagement process involves a competitive tender with documentation at approximately 80 per cent completion. The preferred tenderer enters into a due diligence deed. During this phase the preferred tenderer works with the design consultants to finalise the design documentation, price and the program. This process allows the contractor to provide a proactive role during the finalisation of design. Buildability23 input and coordination between disciplines is managed by the contractor. The contractor has responsibility to ensure the client's briefed requirements are achieved and all site and sub-surface conditions are addressed.

Facility design

Shortly after its appointment, Finance's Project Manager undertook a detailed review of the project program. The Project Manager's initial assessment was that project completion could be delayed by six months from December 2005 to June 2006. At the completion of the program review, a provisional revised date for practical completion of March 2006 was established. Nevertheless, the revised project timetable was based on a short timetable for developing designs and having them endorsed by DIMIA. In addition, the facility construction budget was consistently under pressure from an early stage of the design development process.

The facility design was to be prepared in four stages, with each of the stages constituting a ‘hold point' such that design work would stop until DIMIA endorsement of that stage of the design was secured. The planned approach explicitly recognised that:

- this process may cause delays but that delays during the design phases would ultimately cost less in time and money than delays in the construction phase; and

- the level of risk and associated impact on cost and quality, for delay and changes during the construction is usually higher and is expected to be significantly increased for this project by the remote location of Christmas Island.

However, due to time pressures associated with an overly-ambitious project timetable and delays in the development of the design documentation, the management of the project departed from the identified risk management strategy of design hold points and the detailed design being completed before the Main Works tender was undertaken and construction commenced.

Instead, the procurement strategy was revised to allow for concurrent conduct of the Main Works Contract tender and completion of design documentation and later design stages were commenced without waiting for DIMIA's endorsement of the prior stage. Specifically:

- it was originally intended that design briefs would be completed by the time the Project Manager was engaged (in May 2003) and that schematic design would commence concurrently with the appointment of the Project Manager.24 However, after appointment in May 2003, the Project Manager advised Finance that it had become apparent that the CIIDC project requirements had not been endorsed by DIMIA resulting in a new stage being added to the project master program. This new stage was to involve the design brief and the concept design being completed by the end of July 2003 but this did not occur until 24 September 2003;

- preparation of the schematic design then commenced prior to endorsement of concept design, but its completion was delayed;25 and

- the tender was conducted on a less mature design than originally envisaged, with delays in providing information to tenderers extending the tender closing date.

Further delays occurred after a preferred tenderer was selected. This was reflected in an unplanned further issue of design documentation (so as to allow a final GMP to be set), a delay in the completion of the Investigation Period (the third and final stage of a GMP procurement process) and in the Main Works Contract being amended prior to signature to include a new clause as follows:

The parties agree that as at the date of this Contract, the drawings26 have not been provided to the Contractor. The drawings will be progressively provided to the Contractor in accordance with a program to be agreed between the parties.

The Main Works Contract was signed in late January 2005 with an amended date for Practical Completion of 31 August 2006, a delay of five months compared to that included in the Request for Tender (RFT). Construction work did not commence on site until April 2005 and Approved for Construction designs were not completed and accepted by the Contractor until September 2006 (they had been scheduled for completion in November 2004). The design documentation issues led to a number of time extensions being approved for the Main Works Contractor.27

Project budgets and estimates

The original $197.7 million facility construction budget had been based on ‘order of magnitude' amounts developed by DIMIA and Finance in December 2002. Subsequently, the Cost Manager prepared Project Cost Reports for the Concept Design and Schematic Design, and Pre-Tender Estimates for the Early Works and Main Works.

The Concept Design Cost Report dated September 2003 stated that the project was within the allocated budget. The Confidential Cost Breakdown provided to the Public Works Committee (also in September 2003) was based on the Concept Design Cost Report. However, the Committee was not informed that the estimate on which it had been based had been tailored to match the budget such that it did not reflect a genuine estimate of the cost to complete the works as designed at the Concept Design phase.28 In particular, the Committee was not informed that:

- the estimate included a contingency figure 46 per cent lower than that recommended by the Cost Manager; or

- the Government decision to respecify the project and transfer delivery responsibility to Finance had provided a mechanism for the provision of additional funding following market testing, should it be agreed by Government.

In addition, advising the Committee that the construction estimate as $177.8 million implied a level of precision that was at odds with the level of project uncertainty at this stage. An estimate to the nearest $20 million, or more, would have been more commensurate with the state of development of the design and the procurement plan. Similarly, the Schematic Design Cost Report included an estimate of $232 948 096 when, for this level of design, an order of accuracy of +/- 30 to 40 per cent may generally be expected.

Main Works tender

At the time Finance issued the RFT for the Main Works Contract, its Cost Manager had estimated (in the Schematic Design Cost Report) that the facility construction project was $35 million over budget. Finance advised ANAO that market testing (a prerequisite to seeking additional funding from Government) was to occur prior to investigating budget reduction measures. On the basis of the tenders received,29 Finance obtained a $59 million increase to the original Finance Budget Allocation of $197.7 million.

Finance decided to enter into the Main Works Contract on the basis of its assessment that the GMP was $207.949 million. However, this was not the maximum amount that could become payable under the contract. Specifically, through the contract, Finance had agreed to underwrite potential ‘value engineering savings' of $13.054 million and the Main Works Contractor was entitled to a bonus of $200 000 if a sufficient amount of work was awarded to Christmas Island businesses. This meant that, at the time it was signed, the ‘true' GMP was over $221 million such that the budget increase of $59 million (including a contingency of $6 million) was likely to be insufficient to fund the cost of construction. As it eventuated, the local business development bonus was paid in full and $4.9 million of the ‘value engineering savings' could not be realised, with the shortfall met by Finance.

In addition, the decision to undertake the main facility works tender process and sign a construction contract prior to detailed design being completed inhibited the planned transfer of risk to the construction contractor under a GMP contract. This was reflected, for example, in the amount of Provisional Sums30 included in the contract price.31

A second budget increase was obtained by Finance in August 2006. The second increase, $60 million, included the amount of $4.9 million arising from the shortfall of expected savings. However, the second budget increase was necessary, in large part, due to increased external costs that resulted directly or indirectly from design delays and the change in Main Works delivery approach from a traditional sequential process to instead involve an overlap of the design and tendering processes, with the tendering process completed and a contract signed based on incomplete design documentation. ANAO estimated that the design-related costs required two-thirds of the $60 million second budget increase.

Construction cost increases and delays

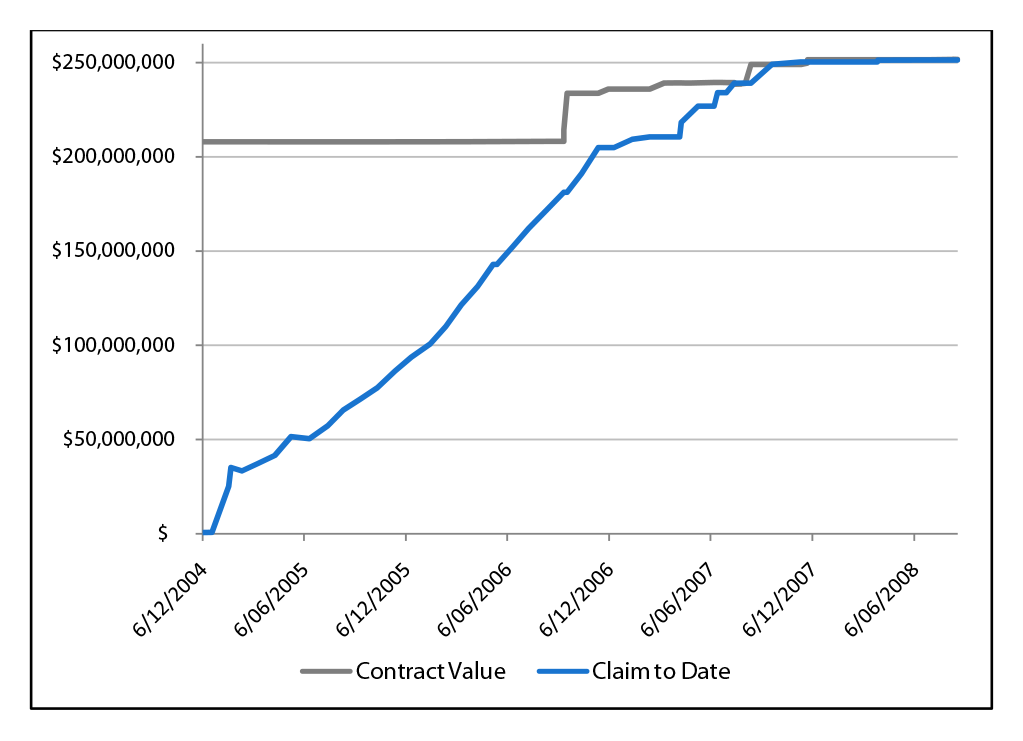

The majority of Finance's second budget increase was used to fund a $43 million increase in the value of the Main Works Contract. In this respect, the value of the Main Works Contract was varied on 25 occasions between May 2006 and August 2008. As illustrated by Figure 1, the final value of the Main Works Contract was $251.6 million, a figure 21 per cent higher than the ‘headline' GMP of $207.9 million assessed by Finance at the time the Contract was signed. In addition to payments attributed to the Contract, a further $1.34 million was paid to the Main Works Contractor in relation to repairs and maintenance of the construction camp ($605 516) and three of the four crane journeys ($736 263). There were also other works originally intended to be delivered under the Main Works Contract that were delivered through other means, specifically:

- a variation to the Early Works Contract was negotiated to include $1.3 million of civil works at the northern boundary of the CIIDC site; and

- various deferred and additional works that were completed by Finance (through its contracted Project Manager acting as a Construction Manager) in order to bring the facility to a ‘fit for purpose' condition such that it could be handed over to DIMIA—$2.35 million including $115 275 in contract administration fees paid to the Project Manager (in effect, the Project Manager performed a role similar to that of a Construction Manager although its contract was not amended to address this extended and different role).

Figure 1 Main Works Contract Value and Contract Payments

Source: ANAO analysis of Finance data.

Delays in the delivery of the Main Works Contract, and additional costs, also resulted from:

- the new crane at Flying Fish Cove being taken out of service in January 2006 due to the discovery of major foundation faults during routine maintenance. The crane was out of service for some six months while the foundations and footings were repaired and/or replaced;

- on 31 August 2006, power to the CIIDC site failed due to a fault in the underground high voltage main cable connecting the facility to the Island's power supply.32 Power was interrupted fully for two days and was not fully restored until 9 September 2006.33 In addition to the cost increases borne by Finance for this failure, the DOTARS Budget Allocation was increased in October 2007 by $5 million for DOTARS to replace the main power supply cable to the site that had been installed as part of the DOTARS infrastructure works but which had subsequently failed;34 and

- inclement weather—in total, nine extensions of time were granted for wet weather between September 2006 and May 2007 (as part of the negotiation of the Second Deed of Settlement Finance agreed to release to the Main Works Contractor liquidated damages it withheld in respect of the failure to achieve Practical Completion by 19 April 2007, and waived its right to impose liquidated damages up to and including 13 October 2007 with the Second Deed also providing for a payment by Finance of $10 million).35

Project outcomes and evaluation (Chapter 7)

The objectives of the project were to:

- build the first purpose-built CIIDC in Australia that met the design brief and was in accordance with the time, cost and quality requirements;

- achieve the successful completion of the project whilst maintaining support from the Christmas Island community;

- deliver the project with environmental excellence;

- build the project with better than industry performance in respect of Occupational Health and Safety;

- deliver the project in a collaborative environment; and

- enhance the reputations of the Principal (Finance), the Project Manager, and subcontractors of the Project Manager and/or Principal and Works Contractor for excellence in construction.

The monitoring of achievement against the first objective was a key ongoing task for Finance and its advisers. Whilst the measurement of performance against the remaining project objectives was not carried out in a formal sense, Finance advised ANAO that it monitored aspects of these objectives during the course of the project. However, as measuring construction projects' performance is essential for ensuring that planned improvements in cost, time and quality are achieved and for identifying potential for improved approaches, there would have been benefits in Finance developing procedures that require:

- a formal post-project review of major construction projects to be undertaken soon after they are completed so as to identify aspects and processes that have been particularly successful as well as those where lessons can be learned; and

- significant project changes, including to the budget, to be promptly reported to the Public Works Committee.

Project time and cost

As noted earlier, Australian Government consideration of the respecified CIIDC project was undertaken on the basis of a $276.2 million whole-of-project budget that included the costs of facility construction (managed by DIMIA in respect to the original project, and Finance for the respecified project), the cost of undertaking infrastructure works necessary for the Centre to be made operational (the responsibility of DOTARS) and DIMIA's ongoing involvement as the facility user. The final budget was $400.5 million but the out-turn cost of the overall project is not known because, whilst Finance's and DIMIA's costs have been established, DOTARS was not able to assemble information on its actual project-related costs.

In terms of the CIIDC facility, the key project delivery parameters of the then Government's February 2003 decision to respecify the CIIDC project and transfer delivery responsibility to Finance involved a Budget Allocation of $197.7 million for Finance to manage the project from February 2003 to completion, which was expected to take 34 months (that is, practical completion by December 2005). In these respects:

- the final approved budget for the facility aspects of the project was $317.0 million, an increase of 60 per cent. As at February 2009, the out-turn cost of the facility works was $311.7 million, $5.3 million or 1.7 per cent below the final budget; and

- the transfer of the CIIDC facility to DIMIA occurred on 7 April 2008. This represented a total project elapsed time of 61 months from the date the project was transferred to Finance, 27 months (79 per cent) longer than the anticipated timeframe when the respecified project was transferred to Finance for delivery.

Meeting client agency needs

DIMIA commissioned a review of the CIIDC and its security arrangements so as to report on whether the facility meets the stated intent of the PWC submission on the proposed facility, and whether it conforms to the recommendations of the Palmer Report, the Comrie Report and the PWC findings in relation to the Maribyrnong Immigration Detention Centre. The review was completed in December 2007, at which time the facility works were close to being completed. It concluded that the purpose of the design brief had been met. Subsequently, DIAC has experienced some shortcomings in the quality of some of the work and issues with the maintenance of the facility and rectification of defects during the Defects Liability Period.

Summary of agency responses

A copy of the proposed report was provided to Finance, DIAC, AGD and DITRDLG. Comments were provided by each agency and have been incorporated in the body of the report. Summary comments were also provided, as follows.

Finance

Finance was responsible for managing the delivery of the CIIDC on behalf of DIAC. This project was unique in that it was the first purpose-designed and built Immigration Detention Centre in Australia, and as such there were no established benchmarks with which it could be compared. The difficulties associated with constructing such a unique project were compounded by the remoteness of Christmas Island, with it being some 1500 kilometres from the nearest point on the Australian mainland, yet only 360 kilometres from Indonesia. There were also significant local challenges to overcome including the sensitivity of the natural environment (most of the Island is designated national park), limited Island infrastructure and seasonal conditions to name a few.

Whilst Finance acknowledges the programming delays and cost increases that were associated with delivering this project, we consider that it is important to recognise that, subsequent to experiences on this and other projects, the Government has implemented two processes aimed at providing improvements in cost certainty and to facilitate greater scrutiny, namely; the two-stage Cabinet approval process for capital works and the Gateway Review process. For the CIIDC these processes may not have foreseen all the issues resulting from the complexity of this particular project, however it is reasonable to expect that they would have narrowed the gap between the initial budget and the final out-turn cost. Finance has also put considerable effort into improving its business processes and has, since receiving responsibility for this project, developed a Better Practice Guide for delivery of capital works projects we deliver. Finance continues to review and improve this guide, and to this end we welcome the ANAO's audit and findings into our project management processes in the context of this project.

Department of Immigration and Citizenship

As you know DIAC does not deliver major works itself, and I note all six recommendations are addressed to the Department of Finance and Deregulation who have a key responsibility to deliver major projects on behalf of other Commonwealth Agencies. Nevertheless, I support all recommendations and recognise the sound principles behind them apply to all works projects irrespective of size.

I am pleased to advise that the key findings and audit recommendations will be carried forward and considered in relation to future works to be undertaken by the Department. This includes the proposed Villawood redevelopment which is in concept stage at present.

Specifically, I note the recommendation for a post-project review of completed works. Now that the facility has been in operation for several months it would be appropriate to do this. I strongly support this happening.

Attorney-General's Department

The Attorney-General's Department supports the recommendations. Implementation will provide robust governance for major capital projects undertaken by the Commonwealth.

Extracts of the proposed reports were provided to Finance's Project Manager, Principal Consultant and Cost Manager. Detailed comments were provided by the Project Manager and Principal Consultant and have been reflected, as appropriate, in the body of the report.

Footnotes

1 The project is now referred to as the Christmas Island Immigration Detention Centre (CIIDC).

2 The department is now known as the Department of Immigration and Citizenship (DIAC). It is referred to as DIMIA in relation to actions prior to its renaming and as DIAC in relation to actions since that time.

3The department is now known as the Department of Infrastructure, Transport, Regional Development and Local Government (DITRDLG). As a result of the November 2007 Federal election and subsequent changes to the Administrative Arrangements Order, all relevant Territories staff and records associated with the CIIDC project and related infrastructure services for which DOTARS had been responsible were transferred to the Attorney-General's Department (AGD). The formal transfer occurred on 25 January 2008, with the physical relocation of the Territories staff occurring in March 2008. Local government services are provided on Christmas Island by the Shire of Christmas Island.

4 Termination took effect on 31 May 2003.

5 Prior to the change of Government following the 2007 Federal Election, the department was known as the Department of Finance and Administration.

6 As opposed to the ‘fast-track' process, involving parallel design and construction for the purpose-built CIIDC proposed for the original project.

7 Specifically, DOTARS was provided with funding for an additional port facility at Nui Nui (the main port is at Flying Fish Cove) and an associated upgrade to the link road, upgrade of other roads (including the construction of crab crossings), provision of housing for facility staff, construction of sports facilities and the provision of water, communications and power to the facility site.

8 Parliamentary Standing Committee on Public Works, Manual of Procedures for Departments and Agencies, March 2008, Edition 7.2, p. 38.

9 ANAO has outlined in other reports the importance of having a lead agency, allied with associated risk management and whole-of-government performance management arrangements (see ANAO Audit Report No.50 2004–05, Drought Assistance, Canberra, 2 June 2005, pp. 24–25). Similarly, in March 2005, all Departmental Secretaries endorsed a guide entitled ‘Working Together' that emphasised the importance of a whole-of-government approach to inter-agency work.

10 In this respect, ANAO has estimated a net delay effect on the project of one month and additional costs of $6.4 million (a new pedestal was estimated to cost $700 000 more than upgrading the existing pedestal).

11 The strategy recognised that:

- tendering the Main Works Contract before a well-developed design had been prepared and/or signing the construction contract before the design had been completed adversely affects the Commonwealth's ability to transfer the risk of design errors and omissions to the construction contractor; and

- delays during the design phases would ultimately cost less in time and money than delays in the construction phase.

12 The second budget increase (of $60 million) was necessary, in large part, due to increased costs that resulted directly or indirectly from the change in approach.

13 As noted in ANAO Audit Report No.20 2008–09, Approval of Funding for Public Works, this feedback ‘loop' can provide incentives for agencies to be rigorous in developing project proposals before they are presented to the Committee, as well as providing valuable information to the Committee on agency performance in delivering projects that the Committee has previously considered.

14 In June 2009, the Principal Consultant (PSC) commented to ANAO that it had initially been appointed by DIMIA under a Deed of Standing Offer to provide architectural services only and that: ‘Later in the process, PSC was engaged by Finance in the role of architect, however this was changed to the role of Principal Consultant when Finance requested PSC to also provide a range of consultant services including Civil Engineer; Structural Engineer; Mechanical; Electrical; Security; Hydraulics; Fire Services; Fire Engineering; Kitchen Design; Furniture, Fittings and Equipment; Acoustics; Access; Building Certifier; Landscape Architect. The terms design consultant, architect and Principal Consultant are not interchangeable.'

15 The Request for Tender informed each firm engaged by DIMIA that it was Finance's intention, pending agreement on contract terms, to continue to engage the existing firm for the duration of the project. An alternative approach would have been to leave open the possibility that other firms were being asked to tender, thereby providing the potential for competitive pressure within the engagement process.

16 Specifically, reporting to Finance by the Project Manager stated that whilst schematic design had commenced on 6 October 2003 it was suspended on 23 October 2003 for nearly six weeks as a result of Finance's decision to undertake a tender process for the Principal Consultant. See further at paragraph 2.36 in the body of the report.

17 This figure relates to the Project Manager and Superintendency Contract, and includes amounts associated with the Project Manager engaging subcontractors to undertake various deferred and additional works. Excluding the amounts payable to subcontractors, the value of the Project Management and Superintendency Contract was increased by 149 per cent.

18 In respect to the Principal Consultant contract, see further at paragraph 2.44 in the body of the report.

19 By way of comparison, there was one important piece of infrastructure works (the construction of a rising sewer main and pump station) that Finance was responsible for delivering and the progress with those works and any impact on the Main Works Contract was addressed each month by the Project Manager in its reports to Finance. Costs were included against Finance's Budget Allocation.

20 This comprised: $577 630 in repair costs met by DOTARS; $4.63 million in increased payments to the Main Works Contractor under the Main Works Contract; $736 263 paid to the Main Works Contractor (outside the scope of the Main Works Contract) for it to provide a temporary crane facility at the port, using the 100 tonne crane from the CIIDC site and a tugboat and barge from Indonesia; and $501 994 in additional payments by Finance to its Project Manager, Cost Manager and Principal Consultant for six weeks of the 13 and a half month delay in the construction stage of the project.

21 The Memorandum of Understanding signed by Finance and DIMIA stated that: ‘The project will be undertaken via a traditional delivery method. Traditional delivery, including a fixed price contract, will provide greater costing certainty prior to construction commencing, and will address allocation of risk by integrating it into the price.'

22 See footnote 14.

23 Buildability is an issue that affects the method of construction, coordination of design elements, temporary works, safety or works sequencing or duration.

24 Tenderers for the Project Manager role were further advised that the first phase of the project would involve the development of a project delivery model and Schematic Design, a process that was expected to take two months.

25 One factor in the delayed completion was that, according to the Project Manager's reporting to Finance, the architect stopped work on the schematic design in order to prepare a response to the Request for Tender for a Principal Consultant issued by Finance in November 2003 for the Principal Consultant contract. See further at paragraph 2.36 in the body of the report.

26 The contract defined ‘drawings' as ‘the for Construction Drawings and the specifications for the work under the Contract to be provided by the Principal to the Contractor'.

27 Extensions of time are granted where there is an allowable delay under the contract and the assessment of any claim is to compare what was supposed to happen with what actually occurred and then identify the reasons for any difference. In June 2009, the Principal Consultant advised ANAO that: ‘The Main Works Contract was executed prior to the completion of the construction documents. The contract required the Contractor to accept these documents so that the risk of documentation discrepancies, errors and omissions transferred to the Contractor. During the procurement process, PSC had expressed concern to Finance and the Project Manager that, having executed the contract, there was no incentive for the Contractor to accept the documents and the risk. It was our concern that acceptance of these documents would be used as a lever by the Contractor in contractual negotiations.'

28In June 2009, the Principal Consultant advised ANAO that it ‘had recognised that there was a fundamental mismatch between the government budget and the government brief. The result of not addressing the budget issues was that, although design started in early 2002 with the design competition, basic design issues affecting scope and centre layout were still being resolved late in 2004.'

29The construction cost of one of the tenders was below the Cost Manager's pre-tender estimate. The other tender was $23 million above the pre-tender estimate. Nevertheless, the lower priced tender still involved a tendered GMP that was expected to result in a budget overrun of $59 million (including $6 million contingency allowance). The Cost Manager advised Finance that:

'The tenders received compare favourably to the pre-tender estimate and generally reflect fair and reasonable pricing given the prevailing market conditions where resources are stretched and competitive interest is perhaps less keen than in recent years.'

30 Provisional sums for certain items of work or equipment in a construction contract are estimates only, and do not represent a maximum limit for that item of equipment or work. This is because it is not possible to accurately predict the cost of those items or work at the time of entering into the contract, or it is uncertain as to whether items of work will be required.

31 The contract price included $9.6 million in Provisional Sums relating to 20 work items. The two largest Provisional Sum items totaled $8 million ($5 million for ‘Loose Furniture, Fixtures and Equipment' and $3 million for the ‘Complete landscaping and irrigation') with Finance's second budget increase nearly doubling the allowance for these items as it included an additional $7.7 million provision for ‘Escalation of provisional sum items currently being tendered for landscaping and furniture, fixtures and equipment'.

32 In November 2002, DOTARS had installed on Christmas Island an 11kV power cable running between the Christmas Island Power Station and the CIIDC in two sections (the first of 4400 metres and the second of 5880 metres).

33 Amongst other things, the power failure resulted in Finance increasing the value of the Principal Consultant contract by $20 580 in October 2007 for the design and documentation of a temporary power solution for the CIIDC so as to mitigate the risk of further power failures to the facility.

34 This was on the condition that, when the contractual matter was settled between the original contractor and DOTARS, funds from any settlement were to be returned by DOTARS. In May 2009, AGD advised ANAO that: ‘The power cable was replaced in 2008 at a cost of $2 720 677. Settlement has not been reached with the original supplier. The Australian Government Solicitor has been engaged to seek compensation from the original supplier and is pursing the matter.'

35 In May 2007, the Main Works Contractor had lodged seven notices of dispute with Finance. At that time, the Contractor claimed that the extension of time that was in dispute was 198.8 days and the amount of extension of time costs in dispute was $40.1 million. As of August 2007, after allowing for prolongation of Principal-caused delays, the Contractor claimed that an extension of 234.9 days was in dispute with costs of $46.89 million. After allowing for the concurrency of some claims, the days in dispute were identified by Finance as representing a delay of 89 days with an amount in dispute of $19.45 million.