Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 24 of 2009–10

Procurement of Explosive Ordnance for the Australian Defence Force

Published

Wednesday 10 March 2010

Portfolio

Defence

Entity

Department of Defence; Defence Materiel Organisation

Sector

Defence

The objective of this audit was to examine the effectiveness of Defence and the DMO's management of procurement and through life support arrangements to meet the explosive ordnance requirements of the ADF, particularly the non-guided munitions requirements of Army. This included a review of the progress of Defence and the DMO in implementing the recommendations of ANAO Audit Report No.40 2005–06.

Summary

Introduction

1. The effective management of explosive ordnance is integral to military capability and essential to the operations of the Australian Defence Force (ADF). The procurement activities managed by the Defence Materiel Organisation (DMO), which involve significant levels of ongoing expenditure, are central to ensuring the ongoing availability of explosive ordnance1 to the ADF. The DMO's sustainment budget for explosive ordnance for 2008–09 was $425.8 million2 of which 85.6 per cent, or $364.7 million, was spent on non-guided explosive ordnance. Of the expenditure on non-guided explosive ordnance, $238.3 million was for Army.

2. Following the 2003 Defence Procurement Review , the arrangements for the management of explosive ordnance were changed, with functions that were previously the responsibility of the Joint Ammunition and Logistics Organisation (JALO) reallocated between Defence and DMO.4 Under this arrangement, logistics issues such as warehousing and distribution became the responsibility of Joint Logistics Command (JLC) in Defence5 while the DMO retained responsibility for the procurement and through life support of explosive ordnance.

3. Initially the Guided Weapons and Explosive Ordnance (GWEO) Branch in the Electronic and Weapon Systems Division managed the explosive ordnance functions retained within the DMO. In February 2008, the Explosive Ordnance Division was established within the DMO to provide a dedicated focus to the ongoing reform of acquisition and sustainment of explosive ordnance.

4. The procurement and through life support of explosive ordnance for the ADF is a complex process and includes:

- fulfilling the explosive ordnance requirements of a variety of stakeholders within available funding;

- developing procurement strategies that are responsive to market conditions, reflect differing supplier arrangements and take into account varying and sometimes extended procurement lead times;

- ensuring effective administration of domestic manufacturing arrangements, which were put in place to ensure the continuity of supply of certain types of explosive ordnance to the ADF; and

- optimising, to the extent possible, explosive ordnance inventory holdings including ensuring that inventory is held at appropriate levels of serviceability.6

5. In May 2006, ANAO Audit Report No.40 2005–06, Procurement of Explosive Ordnance for the Australian Defence Force (Army) found that extensive improvements were required within Defence and the DMO, to better align explosive ordnance procurement processes with ADF preparedness requirements to train and meet contingency requirements should they eventuate. The report concluded that addressing the issues identified by the audit would require the effective implementation of long term remediation strategies by Defence and the DMO.

6. Since the 2005–06 audit, a number of subsequent reviews and studies have concluded that Defence's explosive ordnance arrangements are characterised by fragmented lines of accountability, structures and practices and an absence of a Defence wide ‘end-to-end system perspective'.7

7. Given the ongoing high tempo of operations for the ADF and the materiality (both in terms of financial investment and capability) of explosive ordnance, the ANAO considered it timely to conduct another audit of Defence and the DMO's procurement of explosive ordnance, particularly for Army. This audit provided the ANAO with the opportunity to assess Defence and the DMO's current administration of this key function, including the agencies' progress towards implementing the recommendations of the 2005–06 audit, and other developments in the explosive ordnance domain since the previous audit tabled in May 2006.

Previous ANAO audits

8. This audit is the sixth ANAO performance audit of the explosive ordnance area in Defence since 1987.8 Four of these previous audits, including the 2005–06 audit, dealt specifically with the procurement of explosive ordnance. The findings and recommendations of these audits encompassed stockholding policy, procurement planning, stock management procedures, serviceability of explosive ordnance, contract management and financial management.9 The 2005–06 audit report made 15 recommendations related to the areas of procurement planning, financial management, inventory management, contract management, and safety and suitability for service assessments. In addition to the four previous ANAO performance audits that specifically addressed explosive ordnance procurement, two other ANAO performance audit reports conducted in the last decade have included significant findings related to explosive ordnance. These include:

- ANAO Audit Report No.30 2002–03, Defence Ordnance Safety and Suitability for Service: This audit noted that significant proportions of explosive ordnance inventory could be regarded as legacy ordnance.10 In response to ANAO concerns raised during this audit, the DMO agreed that there was a need to take urgent action to address the legacy explosive ordnance issues. However, subsequently Audit Report No.40 2005–06 found that there had been limited progress in this area.

- ANAO Audit Report No.3 2006–07, Management of Army Minor Capital Equipment Procurement Projects: This audit found a lack of transparency in the slippage from the original service date in the Medium Artillery Replacement Ammunition Project (MARAP), a high value Army minor capital equipment project procuring explosive ordnance.11 The audit report noted that there are a range of complexities associated with this project including linkages to unapproved Major Capital Acquisitions, and issues surrounding domestic manufacturing capability and projects intended to replenish explosive ordnance warstocks through Joint Project (JP) 2085.

Audit objective, scope and criteria

9. The objective of this audit was to examine the effectiveness of Defence and the DMO's management of procurement and through life support arrangements to meet the explosive ordnance requirements of the ADF, particularly the non-guided munitions requirements of Army. This included a review of the progress of Defence and the DMO in implementing the recommendations of ANAO Audit Report No.40 2005–06.12

10. The audit scope covered:

- the explosive ordnance procurement and through life support arrangements for which the DMO retained responsibility following the 2003 Defence Procurement Review;

- the procurement of non-guided munitions for Army, which represents the largest proportion of expenditure of the annual explosive ordnance sustainment budget;13 and

- Defence and the DMO's progress in implementing the recommendations of the 2005–06 performance audit report.

11. The high level audit criteria, based on the findings and recommendations of the previous audit, and taking into account any outcomes or developments that have occurred subsequently, were:

- Defence and the DMO have appropriate processes to forecast demand for14, and plan procurements of, explosive ordnance for training and contingency requirements;

- the DMO has implemented appropriate arrangements for inventory management of explosive ordnance, including to ensure that the serviceability of explosive ordnance inventory is maintained;

- the DMO has implemented effective contract management processes to procure explosive ordnance from domestic and overseas suppliers;

- the DMO effectively manages the budgets for recurrent explosive ordnance procurement and the replenishment of explosive ordnance reserve stocks; and

- the DMO and Defence have effective processes in place to monitor the Implementation of ANAO audit recommendations.

Conclusion

12. The procurement and through life support arrangements for explosive ordnance is a complex activity and is a critical input into ADF capability. A series of performance audits conducted by the ANAO over a number of years has reported on Defence's management of explosive ordnance procurement. In particular, the ANAO's 2005–06 performance audit of the procurement of explosive ordnance15 identified that improvements were required in the areas of procurement planning (in particular the determination of explosive ordnance requirements to inform this activity); inventory management; contract management; financial management; and safety and suitability for service assessments.

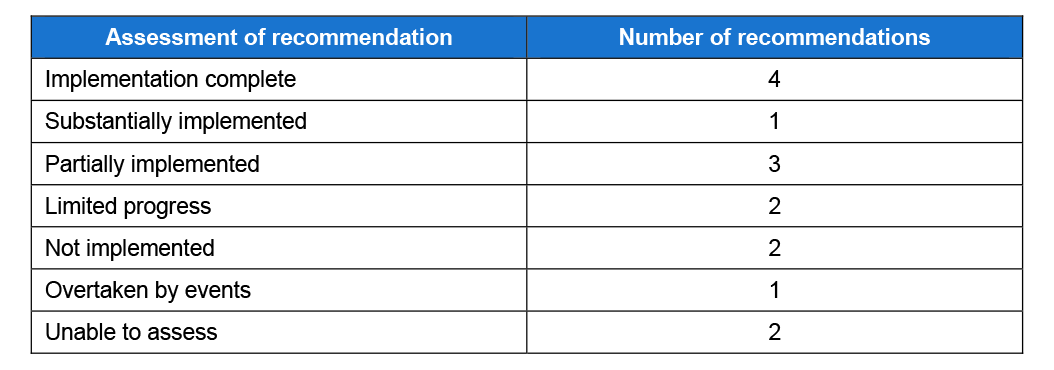

13. In the 2005–06 audit report the ANAO made 15 recommendations which were directed towards addressing the issues identified above. This audit identified that only four of the recommendations of the 2005–06 audit report had been fully implemented16 but all 15 of these recommendations had been closed as complete in Defence's system for managing recommendations. Defence and the DMO have since informed the ANAO that they have improved their internal control arrangements surrounding the monitoring and closure of audit recommendations.

14. Since the 2005–06 audit report was tabled, Defence and the DMO have worked to gain an increased understanding of the issues that need to be addressed to improve performance in the explosive ordnance domain through a series of reviews. These reviews have encompassed explosive ordnance management processes within Defence and the DMO. The findings and recommendations of these reviews have had a high degree of similarity to those contained in the ANAO's performance audits and confirm the need for ongoing improvement.

15. As a result of the ANAO's work in this current audit, which focused on the procurement of non-guided explosive ordnance for Army, the ANAO identified there were a range of ongoing issues which detracted from the effective procurement of explosive ordnance for the ADF. These range from moderately significant issues, including the adequacy of the DMO's management of prepayments to suppliers, to issues with greater significance such as the management of the serviceability of explosive ordnance inventory, explosive ordnance requirements determination and the strategic management of domestic manufacturing arrangements. Cumulatively, the impact of these issues is substantial. In this light, there remains considerable scope for improvement in the management of explosive ordnance and it will be important for Defence and the DMO to effectively implement the current reform programs underway that seek to remediate them (see paragraph 23).

16. Inventory serviceability is an area requiring ongoing attention. At 30 June 2009, Defence's total stock holdings of explosive ordnance inventory were valued at $2.9 billion with some 42 per cent of the value of the explosive ordnance inventory categorised as other than ‘serviceable'17 by the DMO. At 30 June 2009, the value of Army explosive ordnance inventory categorised as other than ‘serviceable' was 57 per cent of the Army explosive ordnance inventory stock holdings valued at $437.7 million. The DMO informed the ANAO in October 2009 that it has recently developed a staged approach to addressing the other than ‘serviceable' inventory and has been undertaking for some time a disposals backlog project which aims to progressively address this element of other than ‘serviceable' explosive ordnance.

17. The 2005–06 ANAO audit of explosive ordnance found that, at the time, funding that was being allocated to the procurement of explosive ordnance during the financial year was being expended through significant prepayments to suppliers with limited or no associated benefits for the Commonwealth from advancing the payments. Accordingly, the ANAO recommended that the DMO's business processes be strengthened to include in the business cases for such prepayments a risk analysis to determine the likelihood of associated benefits being realised. In other words, there should be a business benefit to the DMO from making prepayments in recognition of interest foregone by the Commonwealth and the inherent risks in advancing payments ahead of the receipt of supplies.18

18. Through this audit the ANAO sought to confirm that the issues previously identified surrounding prepayments had been addressed. The DMO has introduced changes to its prepayments Standard Operating Procedures (SOP) that addressed the intent of the ANAO's recommendation. However, the ANAO obtained a sample of prepayments from the DMO and noted that differing approaches to prepayments were being adopted based on the supplier.

19. Many prepayments for explosive ordnance relate to purchases under the Foreign Military Sale (FMS) system19 and the Strategic Agreement for Munitions Supply (SAMS).20 The ANAO acknowledges that the DMO has limited capacity to alter payment arrangements under either the FMS system or the SAMS Agreement, both of which involve some level of prepayment. The ANAO also accepts that the substitute processes21 the DMO has indicated it has in place in relation to these purchases, if properly applied, should provide the protection envisaged by Recommendation No.12 of the previous audit.

20. The DMO informed the ANAO that, of the $29.18 million in prepayments for commercial purchases for Army in 2008–09, only one transaction was a genuine prepayment. This was a $28.55 million prepayment for 25mm ammunition.22 The DMO provided the ANAO with supporting documentation and a copy of the risk assessment for this prepayment. The supporting documentation supplied by the DMO did not include all the required information as identified by the prepayment SOP and did not include calculations required under the Finance Circular No. 2004/14 Discounts for prepayment and early payment. Accordingly, there would be benefit in the DMO reviewing whether current practices give sufficient weight to the business benefits to the Commonwealth of the DMO making such prepayments for explosive ordnance.

21. The explosive ordnance requirements determination process is an area where significant improvement is required and this is supported by a number of Defence reviews. This process is central to inventory management and procurement planning, and is primarily focused on enunciating the explosive ordnance requirements to enable alignment of the procurement processes with the training and operational requirements. While the requirements determination process has been the subject of ongoing review and improvement efforts, further work is required to improve the coordination, timing and quality of forecasts provided to the DMO to inform procurement planning. The 2008 appointment of the Vice Chief of the Defence Force (VCDF) as the single point of accountability for explosive ordnance provides an opportunity to improve the requirements determination process. In particular, it offers the opportunity to achieve better coordination of the inputs to this process from the various stakeholders in the explosive ordnance domain within Defence in order to improve the quality and timing of the forecasts of explosive ordnance requirements provided to the DMO.

22. Domestic manufacturing arrangements for explosive ordnance currently represent an area of significant expenditure that needs to be more strategically managed. The domestic explosive ordnance manufacturing arrangements established under the SAMS and Mulwala Agreements constitute a key measure for ensuring continuity of supply of certain types of munitions.23 Defence spends an average of $20 million on SAMS items each year and, in 2008–09, paid capability payments to the contractor, Thales Australia24, of $63.2 million25 and $29.7 million under the SAMS and Mulwala Agreements respectively.26 In accordance with the provisions of the SAMS and Mulwala Agreements, the DMO informed the contractor in 2008 that these agreements would not be extended beyond 2015. In the period between now and 2015, Defence is obliged under these agreements to continue to make substantial annual capability payments to the contractor. In addition, in 2007 Defence commenced the Mulwala Redevelopment Project at a cost of $431 million to remediate and improve the Mulwala facility. At the time of the audit, there was an absence of strategic planning surrounding domestic manufacturing arrangements and an absence of contemprary investment analysis to support the decision to enter into a contract for the upgrade to the Mulwala facility.

23. With the establishment in 2008 of Explosive Ordnance Division in the DMO, and of Explosive Ordnance Branch in Joint Logistics Command in Defence, there have been a number of reforms introduced to address the ongoing issues. As many of these reforms are still in the early phases of development, and many of these issues have remained unresolved for a long time despite earlier efforts to address them, it is too early to confirm that these reforms will provide enduring improvement to Defence and the DMO's management of the procurement and sustainment of explosive ordnance.27

24. The Government is seeking to derive substantial savings through the Strategic Reform Program28 (SRP) to fund necessary investments in Defence. Over the 10 years to 2019, Defence aims to deliver through the SRP gross savings of around $20 billion. The DMO's major contribution to the overall SRP is entitled the Smart Sustainment Program.29 In total, $180.2 million has been identified to be saved in respect of explosive ordnance under this program over the 10 year time-frame of the SRP, with the savings target for explosive ordnance within the non-equipment procurement stream expected to be $132.2 million, and the savings to be achieved through the reduction in excess holdings of explosive ordnance inventory expected to be $48.0 million. The DMO informed the ANAO in January 2010 that ‘while the total savings targets have been agreed, their phasing over the 10 year SRP period is still under review and negotiation with the Services'.

25. As identified in the 2008 Audit of the Defence Budget and other work by Defence, there are clear opportunities to derive savings in the explosive domain. These savings need not be at the expense of capability but rather as a result of improvements in explosive ordnance management practices within Defence and the DMO. While some savings may be realisable in the short-term, there are likely to be costs associated with past explosive ordnance management practices that will continue to be incurred into the future including rebalancing inventory, addressing serviceability and personnel issues, and ongoing payments under domestic manufacturing arrangements.

Key findings by Chapter

Progress of Reform in the Explosive Ordnance Domain (Chapter 2)

26. Defence's explosive ordnance environment has been the subject of a number of reviews30 over the last decade. These reviews have highlighted a range of shortcomings in Defence and the DMO's management of explosive ordnance including in the areas of:

- governance and accountability related to explosive ordnance;

- procurement planning and requirements determination;

- contract management;

- personnel and training issues; and

- financial management.

27. In response to the findings and recommendations of these reviews, there have been a number of reform programs initiated within Defence and the DMO. These reforms have ranged from initiatives which have targeted specific areas in explosive ordnance management to strategic reforms of explosive ordnance arrangements within Defence and the DMO. Key amongst the strategic reforms was Chief of Defence Force (CDF) Directive 4/2008 in which CDF assigned the VCDF as the single point of accountability for explosive ordnance within Defence. Within the DMO, the primary strategic reform was the establishment of the Explosive Ordnance Division in February 2008, which comprises the Munitions Branch and the Guided Weapons Branch.

28. Prior to the establishment of Explosive Ordnance Division, there were a number of reform initiatives underway in the DMO. These sought to address technical, personnel and structural issues. The outcomes of these reforms are addressed in later parts of this report. Since the establishment of the Explosive Ordnance Division, a number of new and replacement explosive ordnance reform activities have commenced. The majority of these initiatives are still in their early stages and have yet to deliver enduring improvements in the explosive ordnance domain.

Recommendations of the 2005–06 ANAO performance audit report

29. Management Audit Branch (MAB), the area responsible for Defence's internal audit function, uses a database known as the Audit Recommendation Management System (ARMS) to record progress in implementing recommendations for both internal and external reviews undertaken in Defence and the DMO, including the timeframe and reasons for closing particular recommendations. In contrast to the ANAO's findings in this audit (as summarised in Table S 1), including that only four of the recommendations of the 2005–06 audit report had been fully implemented, the status of all 15 recommendations from the previous ANAO audit report were recorded as closed in the ARMS database prior to fieldwork commencing for this audit. The reasons set out in ARMS for this are included in the relevant chapters of the report, where the individual recommendations are discussed in detail.

Table S 1 ANAO assessment of Defence and the DMO's progress in implementing the recommendations of ANAO Audit Report No.40 2005–06

Source: ANAO assessment

30. Given the discrepancy between the ANAO's findings in relation to the progress in implementing the recommendations and the status of the recommendations as recorded in the ARMS database, Defence and the DMO have now implemented improvements to procedures for monitoring the implementation and authorising closure of ANAO recommendations.

Requirements Determination (Chapter 3)

31. The requirements determination process is a fundamental input to the effective management of explosive ordnance inventory within Defence. For any given type of explosive ordnance there are three key elements that the requirements determination process assists in informing, namely the quantity to be acquired; the re-order point; and how much safety stock needs to be maintained for uncertainty. The requirements determination process for the management of explosive ordnance in Defence requires the DMO to engage with a range of stakeholders to plan procurement activities, as listed below.

- Joint Operations Command (JOC) determines the explosive ordnance requirements to support ADF operations and joint activities.

- Capability Managers in the Services31 determine Raise Train Sustain (RTS) requirements32 and provide input into the Materiel Sustainment Agreements (MSAs) with the DMO.

- VCDF is responsible for the determination of reserve stock requirements.

- Capability Development Group (CDG) is the coordinating body for the explosive ordnance requirements to be procured as part of the process of acquiring a new weapons capability under a Materiel Acquisition Agreement (MAA) with the DMO.33

32. Table S 2 summarises the ANAO's assessment of Defence and the DMO's progress in implementation of the recommendations from the ANAO Audit Report No.40 2005–06 covered in Chapter 3.

Table S 2 ANAO assessment of Recommendations Numbers 1, 2 and 3 from ANAO Report No.40 2005–06

Source: ANAO assessment

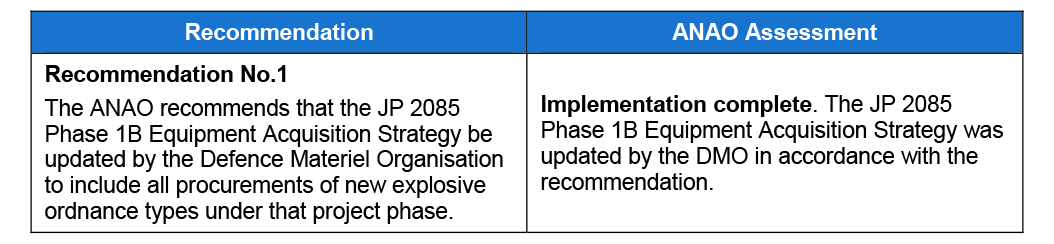

33. All of the recommendations in Table S 2 relate to elements of the requirements determination process. Recommendation No.1 in that table related to Project JP 2085 which is intended to build up explosive ordnance inventory holdings. Recommendation No.3 was concerned with adjusting inventory holdings to reflect the changing requirements brought about by the introduction of weapons platforms through major capital acquisitions.

34. Recommendation No.2 in Table S 2 focused on the interaction between Defence and the DMO for the requirements determination process and was one of the higher priority recommendations from the 2005–06 audit. Supporting the need for priority in this area was a series of reviews carried out subsequent to that audit including the 2007 Review of Defence Policy and Procedures for the Management of Explosive Ordnance (EO), the 2008 Audit of the Defence Budget and the explosive ordnance component of the Logistics Companion Review to the Defence White Paper 2009. All of these reviews commented that the requirements determination process was an area that needed to be improved.

35. Since the previous audit, there has been a focus on improving communication with the Services through high-level Explosive Ordnance Coordination meetings involving representatives from the Services and the DMO's Explosive Ordnance Division. However, this audit identified that requirements determination arrangements continue to be fragmented. Issues identified by the audit included planning horizons for Raise Train Sustain (RTS) requirements not being aligned to procurement lead times, insufficient forecasting of operational requirements and uncertainty surrounding reserve stock holdings. While there have been developments in the issues surrounding the operational requirements and reserve stock holdings during the course of this audit, the nature of explosive ordnance inventory management is such that the impact of these developments will not be able to be assessed for several years.

36. While better defining RTS, operations and reserve stockholding requirements may clarify some of the inputs to an inventory management strategy these elements cannot be considered in isolation of each other as they interact. For example, unplanned consumption in one area may limit availability in others. Additionally, there are a range of other inputs which need to be taken into account in developing an inventory management strategy. These include the serviceability of existing inventory, procurement lead times and differing supplier arrangements. All these inputs need to be consolidated at an appropriate level to optimise inventory holdings from a capability and value for money perspective. This audit identified that inventory management currently occurs within the Munitions Branch of Explosive Ordnance Division using an inventory management tool that has known deficiencies.

Sustainment of Explosive Ordnance (Chapter 4)

37. The responsibility for sustainment of explosive ordnance in Defence is shared across the DMO and JLC. JLC is responsible for warehousing, stock maintenance, national logistics and in-theatre support of explosive ordnance inventory. Munitions Branch in the Explosive Ordnance Division of the DMO is responsible for the management of inventory and addressing serviceability issues.34

38. Table S 3 summarises the ANAO's assessment of Defence and the DMO's progress in implementation of the recommendations from the ANAO Audit Report No.40 2005–06 covered in Chapter 4.

Table S 3 ANAO assessment of Recommendations Numbers 4, 5 and 11 from ANAO Audit Report No.40 2005–06

Source: ANAO assessment

39. While Recommendation No.4 and Recommendation No.5 from the previous audit are assessed as having been ‘overtaken by events' and ‘implementation complete' respectively, these assessments were made because the recommendations were framed around reforms that the DMO had in place at the time that are no longer ongoing. In both cases, these processes have been subsumed into other activities but the underlying issues giving rise to these recommendations remain.

40. Recommendation No.4 was focused on the serviceability of explosive ordnance. At 30 June 2009, Defence's total stock holdings of explosive ordnance inventory were valued at $2.9 billion with some 42 per cent of the value of the explosive ordnance inventory categorised as other than ‘serviceable' by the DMO. At 30 June 2009, the value of Army explosive ordnance inventory categorised as other than ‘serviceable' was 57 per cent of the Army explosive ordnance inventory stock holdings valued at $437.7 million. While not directly comparable with the other than ‘serviceable' figures in the previous audit, these figures suggest that strategies implemented to date have achieved only limited improvement in this key area of explosive ordnance inventory management.

41. During 2009, the DMO developed a staged approach to addressing the other than ‘serviceable' inventory with phase 1 planning and scoping ongoing at the conclusion of audit fieldwork. The DMO has also been undertaking a disposals backlog project which is aimed at progressively addressing one element of other than ‘serviceable' explosive ordnance.

42. The previous ANAO audit report identified skills shortages in explosive ordnance within Defence and the DMO as a major issue. Recommendation No.5 was linked to strategies the DMO had in place at that time. In June 2009, the explosive ordnance component of the Logistics Companion Review to the Defence White Paper 2009 identified skills shortages as an area of ongoing concern. Explosive Ordnance Division has established a Professionalisation Project with the aim of addressing skill shortages in the Division and difficulties associated with the attraction and retention of staff with engineering and technical skills. During the course of this audit the implementation date for completion of this Professionalisation Project slipped from May 2010 to June 2011, which was attributed by the DMO to scope growth in this Project.

Contract Management (Chapter 5)

43. The Mulwala Agreement and the SAMS Agreement are two interrelating contracts that were originally framed to guarantee the future of ADI (now Thales Australia)35 as the Australian Defence Force's ‘first choice source of a specified range36 of explosive ordnance'.37 The Munitions Branch of the Explosive Ordnance Division within the DMO is responsible for the ongoing management of these contracts.

44. The SAMS Agreement requires Thales Australia to maintain a capability to manufacture certain types and quantities of explosive ordnance required by the ADF. This manufacturing capability is located at a munitions manufacturing facility near Benalla in Victoria known as the ‘Benalla Facility'. The SAMS Agreement covers the provision of 13 of the approximately 830 explosive ordnance items in Defence's inventory.38 Defence spends an average of $20 million on SAMS items each year. In addition to payments for the delivery of specific munitions orders, Defence is required to make capability payments39 to the supplier of $63.2 million per year (indexed annually) to retain an agreed level of manufacturing capability.

45. The Mulwala Agreement relates to a Defence owned, Thales Australia operated, propellant and high explosive production facility located at the Mulwala Facility in southern New South Wales. The Mulwala Facility's product is supplied to the Benalla Facility for incorporation into ammunition purchased by Defence; supplied to Defence as a finished product; or sold into the commercial propellant and specialty chemicals market. Under the Mulwala Agreement, Defence pays a capability payment to the supplier of $29.7 million per year (indexed annually) to retain an agreed level of production capability.

46. Table S 4 summarises the ANAO's assessment of Defence and the DMO's progress in implementation of the recommendations from the ANAO Audit Report No.40 2005–06 covered in Chapter 5.

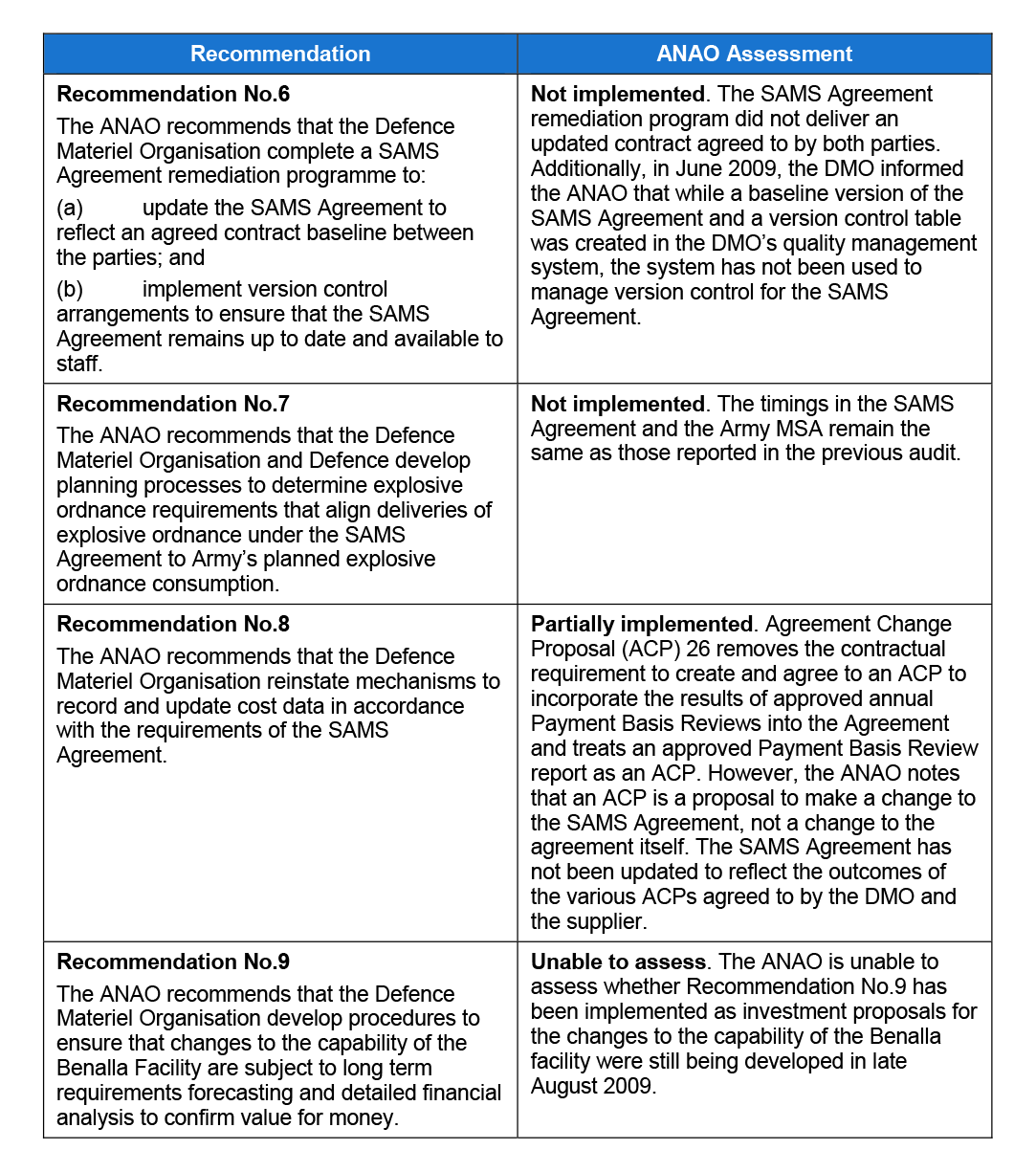

Table S 4 ANAO assessment of Recommendations Numbers 6, 7, 8, 9 and 10 from ANAO Audit Report No.40 2005–06

Source: ANAO assessment

47. As Table S 4 illustrates, the DMO was unable to overcome many of the contract management issues identified by the last audit. Since the 2005–06 audit there have been several significant developments in the area of domestic explosive ordnance manufacture.

48. The SAMS Renegotiation Project was established in January 2006 to review and renegotiate the SAMS Agreement. The objective of the renegotiation project was to ‘deliver a negotiated SAMS contract that better aligns risk and returns in keeping with contemporary expectations'. The SAMS Renegotiation Project failed to achieve this aim.

49. Defence has acknowledged that ‘both Benalla and Mulwala are under utilised, with capability often based on increasingly irrelevant items, and an inability to meet preparedness requirements'.40 The SAMS agreement required the DMO to advise the contractor whether the DMO intended to extend that agreement beyond 2015 by the end of June 2008.41 Consequently, the DMO undertook work to inform this decision and provided advice to the Chief Executive Officer (CEO) of the DMO in June 2008 recommending that the CEO allow the SAMS Agreement to expire at the end of its initial term in June 2015.42 The CEO of the DMO accepted this recommendation and advised the contractor accordingly. In December 2008, a recommendation was also agreed to by the CEO of the DMO that the Mulwala Agreement should also be allowed to expire in 2015 with the contractor subsequently notified of this decision. Unless an alternative arrangement is negotiated, the DMO will continue to be liable for capability payments under the two agreements totalling more than $92 million per annum (indexed annually) until they expire, and may be liable for additional payments upon expiry which have yet to be fully defined.

50. The Mulwala Redevelopment Project aims to replace the existing propellant manufacturing capability that dates back to the 1940s and includes the construction of new nitrocellulose, solvent and propellant production plants, a confined burn facility and a performance and safety testing centre. In March 2007, on the basis of a submission from Defence, the Parliamentary Standing Committee on Public Works recommended that a redevelopment of the propellant manufacturing facility at Mulwala proceed. The approved expenditure for the project is $368 million with an additional $63 million required for environmental remediation works. This Project was experiencing ongoing difficulty at the time of this audit.

51. In July 2009, the ANAO sought confirmation that the investment in the Mulwala facility had been reviewed to confirm that it remains consistent with contemporary requirements and developments in domestic manufacturing arrangements.43 The DMO was unable to demonstrate any such review, relying on a 2001 decision by the Defence Capability Investment Committee. In January 2010, the DMO informed the ANAO that the inaugural meeting for the Project Management Stakeholder Group (PMSG) for the Mulwala Redevelopment Project was held in September 2009. This was more than two years after the contract was signed in June 2007 for the design and construction of the modernised facility. The minutes of the inaugural PMSG, and of the subsequent meeting in December 2009, indicate that these meetings had commenced considering the production capability at Mulwala. The ANAO notes that this has occurred eight years after the 2001 decision by the Defence Capability Investment Committee which set the rate of production for Mulwala.

52. The decision has been taken to allow the SAMS and Mulwala agreements to expire in mid-2015, at the end if their initial terms. In the period between now and when the agreements expire, the DMO will continue to make significant ongoing expenditure under these agreements and on redeveloping the Mulwala facility. There is currently uncertainty within Defence surrounding the form of future domestic manufacturing arrangements for explosive ordnance. In these circumstances, the ANAO considers there would be benefit in the DMO undertaking a strategic review of the domestic manufacturing arrangements to assess the benefits and viability of investment in domestic manufacturing capabilities. At the conclusion of the audit, the DMO was undertaking ongoing investigation and consideration of options to maintain a domestic manufacturing capability post 30 June 2015. The DMO informed the ANAO that options would be presented to Defence Capability Investment Committee in March 2010 prior to a submission to Government.

Financial Management (Chapter 6)

53. The 2005–06 ANAO audit report concluded that weaknesses in procurement planning for explosive ordnance contributed to a poor alignment between explosive ordnance budgets and actual expenditure and also noted that a significant proportion of Defence's prepayments related to procurement of explosive ordnance.

54. Table S 5 summarises the ANAO's assessment of Defence and the DMO's progress in implementation of the recommendations from the ANAO Audit Report No.40 2005–06 covered in Chapter 6.

Table S 5 ANAO assessment of Recommendations Numbers 12, 13, 14 and 15 from ANAO Audit Report No.40 2005–06

Source: ANAO assessment

Note:

A COMSARM (Computer System for Armaments) is Defence's explosive ordnance inventory management system.

B ROMAN (Resource Output Management and Accounting Network) is Defence's financial management information system.

55. A significant issue in the previous ANAO audit of explosive ordnance was that funding was being allocated to the procurement of explosive ordnance during the financial year. This funding was being expended through significant prepayments with limited or no associated benefits. That audit recommended that arrangements surrounding prepayments should be strengthened.

56. The ANAO considers that it remains important that prepayments are only undertaken in circumstances where there is a clear benefit to the Commonwealth and risks are appropriately managed. Notwithstanding that the DMO introduced changes to its prepayments SOP that addressed the intent of the recommendation in the previous audit, the ANAO obtained a sample of prepayments from the DMO and noted that differing approaches to prepayments were being adopted based on the supplier.

57. The DMO informed the ANAO that of the $97.6 million for Army operations explosive ordnance expenditure for 2008–09, $51.2 million represented prepayments made during 2008–09. Some $22 million of this $51.2 million related to purchases under the FMS system and contracted milestone payments under the SAMS Agreement.44 The ANAO acknowledges that the DMO has limited capacity to alter payment arrangements under the FMS system and the SAMS Agreement, both of which require some level of prepayment. The ANAO also accepts that the substitute processes45 the DMO has indicated it has in place in relation to these purchases, if properly applied, should provide the protection envisaged by Recommendation No.12 of the previous audit.

58. The DMO informed the ANAO that, of the $29.18 million in prepayments for commercial purchases in 2008–09, only one transaction was a genuine prepayment. This was a $28.55 million prepayment for 25 mm ammunition.46 The DMO provided the ANAO with supporting documentation and a copy of the risk assessment for this prepayment. The supporting documentation supplied by the DMO did not include all the required information as identified by the prepayment SOP and did not include calculations required under the Finance Circular No. 2004/14 Discounts for prepayment and early payment. Accordingly, there would be benefit in the DMO reviewing whether current practices give sufficient weight to the business benefits to the Commonwealth of the DMO making such prepayments for explosive ordnance.

59. Other recommendations in the previous audit report sought to address budgeting issues, as there was a poor alignment between budget allocations and annual expenditure. The ANAO reviewed expenditure against budget allocations for 2005–06 and 2006–07 and all showed significant variance against the discrete lines of funding that combine to provide the entire annual explosive ordnance budget for Army. For 2007–08 and 2008–09, the variance across the lines of funding was significantly reduced. In 2008–09, the operations budget represented just over 60 per cent of the entire explosive ordnance budget allocation for that year, which was a significantly higher proportion than in the previous years. Of the $97.6 million expended against the operations portion of the budget in 2008–09, $51.2 million related to prepayments.

60. A February 2009 internal review of Munitions Branch procurement practices identified a number of less than adequate practices in relation to the contract and financial management within the branch, including a number of potential breaches of the Commonwealth and Defence financial management and accountability framework, and a limited awareness and use of the Defence Procurement Policy Manual. The Head of Explosive Ordnance Division accepted the findings of the report and requested monthly progress reports in addressing the findings and recommendations of the review from the Director-General of Munitions Branch. The final progress report, dated 31 August 2009, noted that: ‘the critical items are closed and only the ongoing items are being captured as part of normal business'.47A follow-up internal review of Munitions Branch procurement practices is planned for early 2010 to assure the efficacy of the remedial actions.

61. The Accurate Monthly Financial Reporting project is an ongoing initiative within the Explosive Ordnance Division which aims to improve reporting of prepayments; develop and manage budgets on an accruals basis; and introduce other improvements including Financial Management and Accountability Regulation (FMAR) 10 compliance and improvements to the reconciliation process.48 The DMO informed the ANAO in November 2009 that there has been schedule slip in the Accurate Monthly Financial Reporting initiative due to the complexity of reconciliation activities and lack of staff knowledge due to staff turnover.

62. At the conclusion of the previous audit, the ANAO identified that the issues with procurement planning, financial management, inventory management, safety and suitability for service assessments, and contract management required the effective implementation of long term remediation strategies. At the time of that audit the DMO had a number of remediation activities underway and the ANAO acknowledged that this was a positive outcome noting that the DMO was in the initial phases in a process of ongoing reform.

63. This audit identified that there were a range of ongoing issues which detracted from the effective procurement of explosive ordnance for the ADF, a number of which had been identified by previous ANAO audits. In early 2008, structural changes to the way explosive ordnance procurement is managed by the DMO led to the establishment of the Explosive Ordnance Division and the implementation of an ongoing process of reform. Given the limited progress in addressing fundamental issues of explosive ordnance procurement over a long period of time, it is apparent that ongoing and future reform activities need to be closely monitored and refined to ensure that they are delivering enduring improvements.

Defence and the DMO's response

64. Defence and the DMO's response to the proposed audit report was as follows:

Defence welcomes the ANAO audit report on Procurement of Explosive Ordnance for the ADF which examined the effectiveness of Defence and DMO's management of procurement and through life support arrangements to meet the explosive ordnance requirements of the ADF. In particular this report reviewed the progress of Defence in implementing the recommendations of Audit Report No.40 2005–06 of Procurement of Explosive Ordnance for the Australian Defence Force (Army).

The procurement and through-life support of explosive ordnance is a complex process and Defence has implemented considerable changes following the ANAO's 2005–06 report. However, Defence accepts that reform must continue and agrees with the two recommendations in the audit.

Footnotes

1 Explosive ordnance includes: bombs and warheads; guided and ballistic missiles; artillery, mortar, rocket and small arms ammunition; all mines, torpedoes and depth charges, demolition charges; pyrotechnics; clusters and dispensers; cartridge and propellant actuated devices; electro-explosive devices; clandestine and improvised explosive devices; and all similar or related items or components explosive in nature. Source: Defence Policy for the Management of Explosive Ordnance, DI(G) LOG 4-1-013 (in draft).

2 The DMO's forecasted explosive ordnance sustainment budget for 2009-10 is $345 million.

3 Also known as the Kinnaird Review.

4 JALO was established in 1998 in response to a recommendation in the 1997 Defence Efficiency Review and merged the single service explosive ordnance management system into a single tri-service organisation. ‘The Review of Defence Policy and Procedures for the Management of Explosive Ordnance (EO)', 14 December 2007, p. 9.

5 In March 2008, the Chief of the Defence Force (CDF) appointed the Vice Chief of the Defence Force (VCDF) as the single point of accountability within Defence for explosive ordnance. Subsequently, in April 2008, the Explosive Ordnance Branch within Joint Logistics Command was established to, amongst other things, undertake some logistics functions and implement governance for Defence explosive ordnance and weapons security.

6 The successful conduct of these activities is reliant on the availability of a sufficient number of appropriately skilled personnel to undertake them, supported by clear policy, procedures and lines of accountability.

7 Department of Defence, explosive ordnance component of the ‘Logistics Companion Review' to the Defence White Paper 2009.

8 The preceding five audits were: Auditor-General, Efficiency Audit Report, Department of Defence: RAAF explosive ordnance, December 1987; Efficiency Audit Report, Department of Defence: safety principles for explosives, April 1988; ANAO Audit Report No.5 1993–94, Explosive Ordnance, Department of Defence, September 1993; ANAO Audit Report No.8 1995–96, Explosive Ordnance, Department of Defence, November 1995; ANAO Audit Report No.40 2005–06, Procurement of Explosive Ordnance for the Australian Defence Force (Army), May 2006.

9 Since 1987 the explosive ordnance domain has undergone significant changes in structure. In February 1998, as result of the 1997 Defence Efficiency Review, Defence fundamentally changed all aspects of explosive ordnance management through the establishment of the Joint Ammunition Logistics Organisation (JALO). The JALO assumed responsibility for most explosive ordnance functions for the Services, and established new structures and processes to discharge these responsibilities. As noted in paragraph 2, further significant restructuring was undertaken in response to the 2003 Kinnaird review. Accordingly, it is difficult to draw direct comparisons between the findings of ANAO audits pre-dating these restructures and the findings of more recent performance audits.

10 Legacy explosive ordnance is ordnance currently in service for which there is no clearly identifiable audit trail regarding its safety and suitability for service assessment (See footnote 114 for further explanation of this term).

11 This Army Minor project is for the acquisition of a new family of 155mm munitions to provide a significant increase in operational capability for combat force indirect firepower in terms of lethality, range and coverage. Introduction into service of this ammunition will enhance the in-service M198 155mm Howitzer capability. The project is linked to LAND 17 [major capital equipment project], which aims to enhance or replace the 155 mm platform [see footnote 69 for a description of the project]. The principal aim of the project is to ensure that munitions acquired will not be obsolescent, or technologically inferior, on introduction of any LAND 17 155mm Howitzers. Any integration and transition issues will be the responsibility of LAND 17. Subsequent to the Minor project, stock holdings of MARAP ammunition will be procured. Source: ANAO Audit Report No.3 2006–07, Management of Army Minor Capital Equipment Procurement Projects, p. 55.

12 As per the 2005–06 ANAO audit report of the procurement of explosive ordinance, the scope of this audit did not include a review of explosive ordnance distribution and warehousing processes and control arrangements which are managed by the Joint Logistics Command within Defence.

13 DMO's Explosive Ordnance Division also manages a range of other major capital acquisition projects involving the acquisition of guided munitions for the three Services, including but not limited to AIR 5409, JP 2070, AIR 5418, AIR 5349 Phase 2 and SEA 1390 Phase 4B. Given this audit's focus on the procurement of non-guided munitions for Army, these projects are not covered in this audit report. however, the ANAO currently has underway a performance audit of the acquisition of the replacement lightweight torpedo under JP 2070 which is expected to table later this financial year.

14 In the context of the ADF this process is referred to as ‘requirements determination'.

15 ANAO Audit Report No.40 2005–06, Procurement of Explosive Ordnance for the Australian Defence Force (Army).

16 Of the remaining 11 recommendations, one of the recommendations was substantially implemented, three of the recommendations were partially implemented, two demonstrated limited progress, and two were not implemented. One of the recommendations was overtaken by events as the recommendation was framed around processes that the DMO had in place to address serviceability issues at the end of the previous audit that are no longer ongoing. Two of the recommendations were unable to be assessed as Government decisions on the areas covered in these recommendations were still under consideration.

17 Other than ‘serviceable' includes explosive ordnance stock that is beyond repair or potentially serviceable. Potentially serviceable stock includes items identified as repairable, items that have a contingency certification and can be used in a limited fashion, items that are life expired, items that are pending inspection, or items that require Explosive Ordnance Division approval to sentence or the provision of technical data.

18 The Finance Circular No. 2004/14 Discounts for prepayment and early payment advises that to calculate the whole of government cost of the interest forgone in accepting the prepayment, agencies should use the Reserve Bank of Australia cash rate target. In addition, agencies need to take into account other costs and risks that may arise due to the prepayment.

19 Foreign Military Sales (FMS) is a government-to-government sales arrangement under which the United States (US) Defense Department negotiates and manages an FMS “case” for the acquisition of US technology on behalf of the Australian Government.

20 For example, DMO informed the ANAO that of the $97.6 million for Army operations explosive ordnance expenditure for 2008–09, $51.2 million represented prepayments made during 2008–09. This was comprised of $0.66 million in SAMS contracted milestone prepayments; $21 million in FMS prepayments and $29.18 million in prepayments for commercial purchases

21 See paragraph 6.20 for details of these processes.

22 DMO informed the ANAO that the remainder of the $29.2 million, some $0.6 million, represented a data mismatch due the receipting issues associated with COMSARM and ROMAN as outlined in paragraph 6.19.

23 Under the SAMS Agreement, Thales Australia is required to maintain a capability to manufacture certain types and quantities of explosive ordnance required by the ADF. This manufacturing capability is located at a munitions manufacturing facility near Benalla in Victoria. The Mulwala Agreement relates to a Defence owned, Thales Australia operated, propellant and high explosive production facility located at Mulwala in southern New South Wales. Under the terms of the Mulwala Agreement, Thales is required to supply propellant and high explosive to the Benalla munitions factory while the SAMS Agreement, or any contract for this, is in force.

24 At the time of the previous ANAO audit the SAMS and Mulwala agreements were between the Commonwealth and ADI Limited. At that time, ADI Limited was a joint venture between Transfield Holdings (an Australian company) and Thomson–CSF (a French company, partially owned by the French Government, which was renamed Thales in December 2000). In October 2006, the Australian Foreign Investment Review Board approved Thales' acquisition of the remaining 50 per cent stake in ADI Limited which was subsequently renamed Thales Australia.

25 The capability payment amount is indexed annually.

26 The DMO advised the ANAO that capability payments made by the DMO to Thales in respect of the Mulwala Facility totalled $27.2 million in 2007–08, $29.7 million in 2008–09 and the estimated commitment for capability payments for 2009–10 is $34.5 million.

27 The ANAO notes that there are a range of reforms occurring within Defence across the explosive ordnance domain. Given that this audit focuses on the procurement and through life support of explosive ordnance arrangements managed by the DMO, this audit comments on the reforms occurring within DMO and generally only comments on the reforms outside the DMO insofar as they directly impact on the activities of DMO.

28 Defence's Strategic Reform Program brings together the work of the Defence White Paper 2009 and other key reviews including the 2008 Audit of the Defence Budget, with the aim to ‘create the efficient and accountable Defence organisation required to deliver and sustain Force 2030 within the funding envelope agreed by Government'. Department of Defence, The Strategic Reform Program: Delivering Force 2030, p. 3, 2009. <http://www.defence.gov.au/publications/reformbooklet.pdf> [accessed 14 September 2009].

29 This program focuses on three related elements namely maintenance reform, inventory reform and non-equipment reforms related to explosive ordnance, clothing and fuel. Specific savings related to explosive ordnance under the Smart Sustainment Program have been identified in two of these areas: non-equipment procurement and inventory management.

30 The key reviews include the 2007 Review of Policy and Procedures in Explosive Ordnance, the 2008 Audit of the Defence Budget, and the explosive ordnance component of the Logistics Companion Review to the Defence White Paper 2009.

31 The Chiefs of Navy, Army and Air Force.

32 Raise, Train, Sustain requirements refers to the Services' resource needs, including explosive ordnance, to conduct training to support the ADF's capability.

33 MAAs cover DMO's acquisition services to Defence for both minor and major capital equipment projects.

34 Munitions Branch performs these responsibilities for non-guided explosive ordnance. Guided Weapons Branch in Explosive Ordnance Division performs these responsibilities for guided weapons, including the 155 mm Artillery and the Artillery Precision Guided Munitions (APGMs).

35 At the time of the previous ANAO audit the SAMS and Mulwala agreements were between the Commonwealth and ADI Limited. At that time, ADI Limited was a joint venture between Transfield Holdings (an Australian company) and Thomson–CSF (a French company, partially owned by the French Government, which was renamed Thales in December 2000). In October 2006, the Australian Foreign Investment Review Board approved Thales' acquisition of the remaining 50 per cent stake in ADI Limited which was subsequently renamed Thales Australia.

36 Primarily 5.56 mm, .50 cal, 20 mm and 25 mm ammunition natures, 105 mm artillery ammunition, 5"/54 naval gun ammunitions and Mk 82/Mk 84 bombs and the F1 grenade. Source: Department of Defence, explosive ordnance component of the ‘Logistics Companion Review' to the Defence White Paper 2009, p. 3.

37 Department of Defence, explosive ordnance component of the Logistics Companion Review to the Defence White Paper 2009, para. 13, p. 3.

38 ibid.

39 80 per cent of this capability payment is fixed and the remaining 20 per cent is incentive based.

40 Department of Defence, explosive ordnance component of the Logistics Companion Review to the Defence White Paper 2009, para. 16, p. 3.

41 Under the terms of the SAMS Agreement, the Commonwealth was obliged to notify Thales by 30 June 2008 of its intention to: (a) terminate the agreement; (b) extend the initial term (30 June 2015) of the agreement for a further 10 years; or (c) allow the agreement to expire at the end of the initial term (30 June 2015).

42 Under the terms of the Mulwala Agreement, the Agreement is subject to review by the Commonwealth at the same time and in conjunction with any review of the SAMS Agreement. At each such review, the Commonwealth may: (a) terminate the agreement (b) extend the initial term for a further period of 10 years; or (c) notify Thales that the agreement will expire at the end of the initial term (30 June 2015). According to external advice received by the DMO in March 2008, the Commonwealth is likely to be liable to pay Thales a number of expiry payments upon the expiry of the SAMS and Mulwala Agreement at 30 June 2015. The expiry payments could not be accurately identified and quantified at this time.

43 The origin of the decision to undertake this upgrade of the Mulwala facility was a Strategic Review into the modernisation of the Mulwala Facility undertaken in 1999. The 1999 Review was to consider the strategic requirements of Defence; identify improvements required to the Mulwala Facility to ensure compliance with applicable laws; and improvements necessary to ensure the supplier's ability to meet Defence requirements and generate additional commercial sales. The Review identified improvements required to modernise the facility and rectify significant occupational health and safety and environmental issues.

44 This $22 million was comprised of $0.66 million in SAMS contracted milestone payments and $21.37 million in FMS prepayments.

45 See paragraph 6.20 for details of these processes.

46 DMO informed the ANAO that the remainder of the $29.2 million, some $0.6 million, represented a data mismatch due the receipting issues associated with COMSARM and ROMAN as outlined in paragraph 6.19.

47 MUNITIONS/OUT/2009/829 – Munitions Branch Procurement Remediation Action Plan: Progress Report as at 31 August 2009.

48 Regulation 10 of the Financial Management and Accountability Regulations 1997 relates to the approval of future spending proposals and provides that, if any of the expenditure under a spending proposal is expenditure for which an appropriation of money is not authorised by the provisions of an existing law or a proposed law that is before the Parliament, an approver must not approve the proposal unless the Finance Minister (or delegate) has given written authorisation for the approval.