Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 4 of 2005–06

Post Sale Management of Privatised Rail Business Contractual Rights and Obligations

Published

Thursday 4 August 2005

Portfolio

Across Entities

Entity

Department of Transport and Regional Services; Department of Veterans’ Affairs; Department of Family and Community Services

Sector

Social Services

Transport

Veterans' Affairs

The objectives of the audit were to assess the Commonwealth's management of contractual rights and obligations under the Sale Agreements. In particular the audit sought to: assess the Commonwealth's management of contractual warranties and indemnities; assess DoTARS' management of each purchaser's compliance with contractual commitments to capital expenditure; and examine the effectiveness of the development and management of contractual arrangements for concessional rail passenger travel provided by the Commonwealth.

Summary

Introduction

The three rail businesses of the former Australian National Railways Commission were sold to separate purchasers in 1997. Two of these rail businesses (SA Rail Pty Limited and Tasrail Pty Limited) were intrastate freight operators. The other (Pax Rail Pty Limited) operated interstate passenger services on The Indian Pacific, The Ghan and The Overland. The sales raised aggregate proceeds of $95.4 million for the Commonwealth. In 1998, the Australian National Audit Office (ANAO) conducted a performance audit of the sale of the three rail businesses.

As well as providing for the sale of shares in the rail businesses, the Sale Agreements placed ongoing rights and obligations on the purchasers of the rail businesses, and the Commonwealth.

Each of the Sale Agreements contained a number of indemnities and warranties. Also common to each of the Agreements was a requirement for the purchaser to undertake a certain amount of capital expenditure. The Department of Transport and Regional Services (DoTARS) has had responsibility for administering these aspects of the Sale Agreements.

One of the major obligations placed on the purchaser of Pax Rail through the Pax Rail Sale Agreement related to the provision of concessions to certain passengers. Prior to the sale, a substantial proportion of passengers on The Indian Pacific, The Ghan and The Overland travelled on concession tickets. The Government decided that these concessions should continue post-sale. The original Sale Agreement, and subsequent contractual arrangements, required the Commonwealth to contribute to the cost of providing these concessions.

DoTARS was responsible for administering the delivery of rail concessions until 30 June 1998. From 1 July 1998, the Department of Family and Community Services (FaCS) assumed responsibility for the delivery and administration of the rail concession process for social welfare recipients and veterans.

Audit Objectives

The objectives of the audit were to assess the Commonwealth's management of contractual rights and obligations under the Sale Agreements. In particular the audit sought to:

- assess the Commonwealth's management of contractual warranties and indemnities;

- assess DoTARS' management of each purchaser's compliance with contractual commitments to capital expenditure; and

- examine the effectiveness of the development and management of contractual arrangements for concessional rail passenger travel provided by the Commonwealth.

Overall Audit Conclusions

In terms of the audit objectives, ANAO concluded as follows:

- to date, the Commonwealth's post sale exposures under the Sale Agreements' warranties and indemnities have not resulted in any financial cost to the Commonwealth;

- there is evidence that the purchasers' capital expenditure commitments have been met, although DoTARS could have better managed this aspect of the Sale Agreements; and

- concessional travel has continued to be provided under various contractual arrangements. However, FaCS' management of the passenger concession arrangements has not complied with the Commonwealth's financial framework, which has led to an increased risk that the Commonwealth is not obtaining value for money from the contractual arrangements.

Recommendations and Agency Responses

ANAO has made two recommendations to improve ongoing management of passenger concession arrangements. FaCS agreed with both recommendations. In addition, DoTARS, FaCS and the Department of Veterans' Affairs (DVA) provided summary comments on the report, as follows.

DoTARS

DoTARS considers that the outcomes of the sale of the three rail operating entities (SA Rail, Tasrail and Pax Rail) were successful. The sales fully met the Government's objectives including receipt of a good price for the assets and rail industry reform that would allow rail to compete with road transport, with the sales resulting in the introduction of strong and proven private sector companies that increased the competitiveness of rail on pricing and the quality of operations.

Since the sale of these rail assets, and in conjunction with other reforms, the rail industry has increased its share of the land transport freight market between the east coast and Perth from 69 per cent in 1997–98 to over 80 per cent currently.

In relation to the post sale obligations on the purchasers, the department notes that they have been fully complied with and the finding of the ANAO is that the Commonwealth's post sale exposures under the Sale Agreements' warranties and indemnities have not to date resulted in any financial cost to the Commonwealth.

The department also notes that the ANAO found evidence that the purchasers' capital expenditure commitments had been met in the case of each of the three sales. The value of capital expenditure required under the three sales agreements was $86.6 million. The actual investment undertaken by the three purchasers totalled $112.9 million, more than 30 per cent in excess of the investment the purchasers were required to undertake.

Nevertheless, the department acknowledges that there should have been tighter administration of processes including better procedures to ensure the timeliness of reporting by the purchasers. The ANAO report provides valuable lessons for the department in the future especially as to the importance of having appropriate follow up arrangements and clear, consistent and documented internal procedures in place for handling ongoing issues in a “post asset sale” environment.

FaCS

The audit investigations have assisted FaCS in ensuring it meets its obligations under the Commonwealth purchasing framework. Indeed many of the recommendations of the report have already been addressed or are being addressed in the process of renewing contractual arrangements. In this context FaCS broadly agrees with the recommendations of the report.

FaCS believes provision of further information regarding: reasons for the reimbursement method chosen; reasons for changes in the average cost per client; technical constraints with use of customer confirmation systems; and data sources underlying contract variations, would have assisted in contextualising a number of the issues raised.

DVA

The Department of Veterans' Affairs (DVA) notes the recommendations to improve ongoing management of passenger concession arrangements. The recommendations will not affect access to concessions by eligible veterans and their dependents. It is not expected that the recommendations will have any significant effect on DVA's procedures. However, to the extent necessary, DVA will provide what assistance it can to help the Department of Family and Community Services implement agreed recommendations.

Key Findings

Management of contractual exposures and purchaser commitments

Post sale monitoring of indemnities and warranties

Each of the Sale Agreements contains a number of indemnities. These are promises whereby a party undertakes to accept the risk of loss or damage another party may suffer. To date, no claims have been made against any of the Commonwealth indemnities.

A warranty is a promise whereby a vendor provides certain assurances to the purchaser. There were a number of warranties provided by both the purchasers and the Commonwealth in each of the Sale Agreements. There are no ongoing purchaser warranties to be monitored by the Commonwealth, and Commonwealth warranties made to the purchasers have not led to any additional cost to the Commonwealth.

Capital expenditure

Total capital expenditure required of purchasers under the Sale Agreements was $86.6 million. The importance of the capital expenditure commitments was evident from the conduct of the 1997 sales process. In particular, one of the main reasons the Commonwealth did not accept the highest bid for SA Rail Pty Ltd was the commitment made by the successful bidder to undertake $52.3 million of capital expenditure by 31 December 2002.

Capital expenditure was to be made in accordance with definitions specified in each Sale Agreement, and verified through periodic audits performed by the purchasing company's auditors. ANAO found that DoTARS did not develop and document any procedures for assessing the rail capital expenditure commitments. This adversely impacted upon:

- the timeliness with which audit certificates were obtained;

- the level of assurance obtained from the audit certificates;

- DoTARS' ability to assess whether reported expenditure was in accordance with the Sale Agreement requirements; and

- DoTARS' finalisation of the achievement, or otherwise, of the contractual commitments.

Nonetheless, from the available documentation, it appears that each purchaser met its capital expenditure commitment by the date specified in the respective Sale Agreement.

Concessional rail travel

The Commonwealth sold Pax Rail to Great Southern Railway Limited (GSR) in 1997 for $16 million. Since the execution of an amended Sale Agreement on 31 October 1997, at the time of audit fieldwork there had been three different contractual arrangements in relation to the provision of concessional rail travel by GSR. Each of these contractual arrangements has provided that GSR would offer certain concessions on its trains, with the Commonwealth contributing to the cost of providing these concessions.

ANAO found that FaCS was not sufficiently well informed in its contractual negotiations for concession arrangements to reliably conclude on the value for money of the agreed outcome. In particular, FaCS did not examine the reasons why costs were increasing whilst usage was falling.1 In this context, for the major contracts, FaCS agreed to make fixed payments based on forecast patronage without provision to adjust for the actual passenger journeys.

In response to concerns raised by ANAO, FaCS has suggested that reasons for the increased costs may include natural cost increases and an increase in the number of the concessional passengers travelling that are more expensive for the Commonwealth to purchase, such as Special Veterans and Commonwealth Seniors Health Card holders. However, ANAO considers it would have been sound administrative practice for such questions to have been addressed prior to the contracts being signed. 2

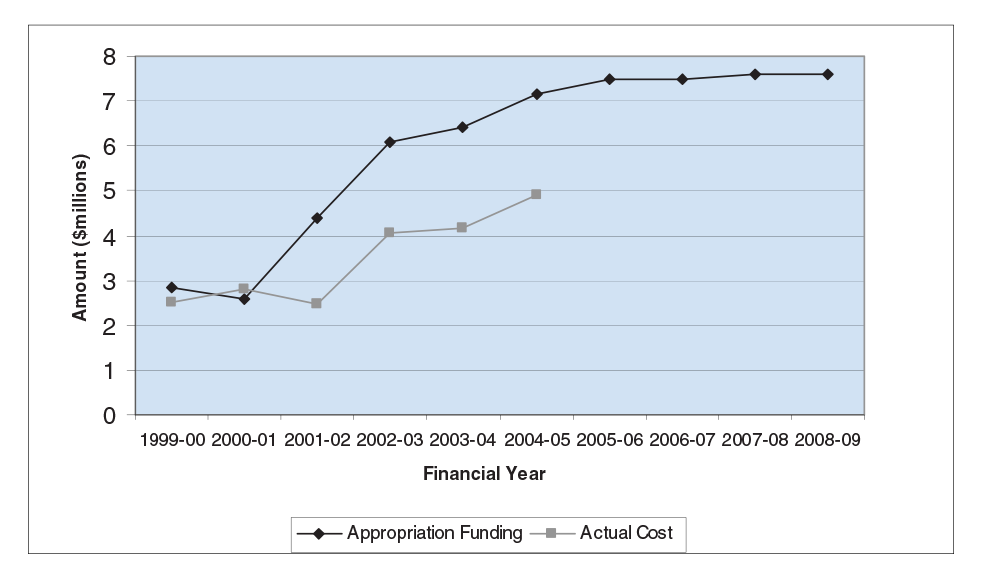

FaCS receives funding for payments to GSR as part of its administered annual appropriations. FaCS has consistently over-estimated the amount of funding it has required, even where contracts have provided a cap on total payments. In total, the amounts appropriated to FaCS in respect of GSR payments have, over six years, been $8.4 million (40 per cent) more than that required. Actual costs and amounts appropriated are illustrated in Figure 1.

Figure 1: Amount appropriated to FaCS for payments to GSR and actual cost

Source: ANAO analysis of FaCS financial data, 2004–05 deed of variation, FaCS Portfolio Budget Statements and 2005–06 Budget Papers.

Footnotes

1 Annual expenditure on passenger concessions rose from $2.7 million in 1998-99, to $4.9 million in 2004–05. Between 1999-00 and 2003-04, the number of trips taken by eligible clients fell from more than 90 000 to less than 72 000.

2 In this context, FMA Regulations 9 and 12, taken together, require a documented assessment, prior to contract signature, of whether the proposed expenditure represents an efficient and effective use of public money.