Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 9 of 2017–18

Management of the Pre-construction Phase of the Inland Rail Programme

Published

Wednesday 27 September 2017

Portfolio

Infrastructure and Regional Development

Entity

Australian Rail Track Corporation (ARTC); Department of Infrastructure and Regional Development; Department of Finance

Contact

Please direct enquiries relating to reports through our contact page.

Activity

Procurement

Sector

Infrastructure

Regional Development

Transport

The objective of this audit was to examine whether value for money is being delivered by the Australian Rail Track Corporation’s (ARTC’s) management of the Inland Rail pre‑construction program.

Summary and recommendations

Background

1. The Inland Rail programme is to construct an inland rail line from Melbourne to Brisbane, covering a total distance of approximately 1700 kilometres. In 2014, the Australian Government provided $300 million for pre-construction work on the proposed rail line, and in 2017 committed $8.4 billion to build it. The Australian Rail Track Corporation (a wholly government owned business enterprise) is undertaking the pre-construction work, and has been selected by government to deliver the full programme of works over the next seven years, 2017–18 to 2024–25.

2. The Australian Government's commitment to build the Inland Rail in its entirety, and confirmation that the Australian Rail Track Corporation was best placed to deliver it, were announced during the course of the pre-construction activities. The timing of these decisions created challenges for the Australian Rail Track Corporation in managing the pre-construction programme.

Audit objective and criteria

3. The audit objective was to assess whether value for money was being delivered by the Australian Rail Track Corporation's management of the pre-construction phase of the Inland Rail programme. To form a conclusion against the audit objective the Australian National Audit Office examined whether:

- governance arrangements were appropriate, and administration of grant funding was effective; and

- the Australian Rail Track Corporation's procurement activities provided value for money and were supported by Information and Communications Technology systems and appropriate policies and procedures.

Conclusion

4. In managing the pre-construction phase of the Inland Rail programme, the Australian Rail Track Corporation (ARTC) could have had a greater focus on achieving value for money in procurement activities. The ARTC identified the need to improve existing business functions and procurement practices throughout the pre-construction phase, and commenced initiatives to strengthen administration. These initiatives need to be fully implemented to support the ARTC in effectively managing the full Inland Rail programme in coming years and delivering value for money.

5. Governance arrangements for the pre-construction phase of the Inland Rail programme were appropriate, although there was not timely implementation of the Minister's decision that a funding agreement be developed between the Department of Infrastructure and Regional Development and the Australian Rail Track Corporation. The Australian Government's longer term intent with regard to the delivery and full construction of the Inland Rail was appropriately considered, including through the administration of grant funding. There could have been more emphasis on achieving value for money in procurement and contracting activities, including for the ARTC's contracting of staff for the programme, and improved planning for the leasing of property.

6. Testing of a sample of 54 procurements for the Inland Rail programme found a lack of consideration given to competition in the early phase of the programme, where a considerable proportion of procurements (17 per cent of the sample) were sole sourced. Procurement activities improved during the sampling period, as new systems, processes and practices were implemented. The ARTC's established Information and Communications Technology (ICT) systems and procurement and document management processes and practices were well short of the needs of the Inland Rail programme. The ARTC is further reviewing its procurement policies and procedures and supporting business functions for the full construction of Inland Rail.

Supporting findings

Governance and funding arrangements

7. Governance arrangements oversighting the pre-construction phase of the Inland Rail programme were appropriate, in so far as they adapted to the different stages of the implementation of the programme, and considered the Australian Government's interests with regard to longer term decisions about the delivery of the complete Inland Rail. There was no evidence however, that due consideration had been given to matters raised about the skills and status of committee members, specifically in relation to departmental representation. There could also have been more emphasis on achieving value for money in procurement and contracting activities. The ARTC's internal governance arrangements were appropriate, with a high level of engagement by the company's Board throughout the pre-construction phase. The ARTC is strengthening its processes to manage risk, and needs to implement a suitable system to support the management of risk in the Inland Rail programme.

8. Grant funding was appropriately managed for each of the four funding packages provided for the pre-construction phase of the Inland Rail programme. There was extensive engagement between the ARTC and the Department of Infrastructure and Regional Development (Infrastructure) in preparing the funding submissions, and Infrastructure appropriately assessed the submissions and approved milestone delivery payments. Protecting the Commonwealth's interests centred on how best to use the funds, given the status of the project over the longer term and the ARTC's role in delivering it. However, high-level deliverables, outcomes and reporting arrangements were not developed through the Minister's required funding agreement for the pre-construction phase, which could have supported greater emphasis on obtaining value for money in procurement activities associated with the milestone deliverables identified in the grant funding submissions.

9. The ARTC has maintained separate costs for the pre-construction phase of the Inland Rail programme, from commencement of the programme in 2014. These costs were more effectively administered some two years into the programme, with the implementation in August 2016 of upgrades to the company's financial management system that allowed more detailed allocation and monitoring of costs. The ARTC has secured additional office accommodation for staff in the Inland Rail programme, but in the absence of a property plan for the programme or for the ARTC's property needs more broadly, it cannot be assured that it is achieving value for money in leasing costs. Similarly, staffing requirements for the programme have been met through contracting arrangements for specialist staff, but with no forward plan as to the requirements of the programme. However, these arrangements have provided flexibility in recruitment, and will likely be a source of workforce skills in the longer term. The ARTC needs appropriate procurement processes in place to ensure transparency and value for money in securing contracted staff, as in all other contract arrangements.

Procurement

10. The ARTC did not have appropriate ICT systems to support procurement for the pre-construction phase of the Inland Rail programme. There was a heavy reliance on manual processes, paper-based approvals and non-standardised records management procedures. As at July 2017, specifically for the Inland Rail programme, the ARTC has upgraded the Contracts module and implemented a Tenders management module in the corporate Financials & Supply Chain system, and is at an early stage in deploying a system for records management. These improvements, if fully bedded down, with intended functionality being utilised and supported by updated procedural documentation, would strengthen the Inland Rail programme's procurement processes and records management, and could have application more broadly across the ARTC.

11. The ARTC did not have appropriate policies and procedures to support procurement for the pre-construction phase of the Inland Rail programme. Established procurement policies and procedures were not sufficiently robust for the administration of the Inland Rail programme. The Inland Rail team is subsequently developing a suite of procurement policies and procedures specifically for the programme, although many were still in draft form as at July 2017. If finalised and fully implemented, these documents should support a level of rigour in the programme's procurement practices not previously evidenced, and could also be applied more broadly across the company.

12. Testing of a sample of procurements undertaken between 29 April 2014 and October 2016 for the pre-construction phase of the Inland Rail programme found shortcomings in providing value for money. There could have been greater consideration of competition in the selection processes, although the use of non–competitive procurement methods was concentrated in those procurements undertaken prior to July 2015. In the sampled procurements conducted after that date, there were improvements in the levels of competitive procurements and documentation. Evidence of the importance of probity in procurement is shown through ARTC's contracting procedure, but testing identified insufficient documentation of the reasons for or against using a probity advisor. The testing also showed many variations to contract values that were not sufficiently explained, and work commencing prior to contract execution. These issues had been identified in ARTC internal audits. A review of the documentation for four later procurements showed improvement in the procurement process, consistent with the upgrade in the systems and newly developed policies and procedures supporting procurement for the Inland Rail programme.

Recommendations

Set out below are the ANAO's recommendations and the ARTC's response.

Recommendation no.1

Paragraph 2.32

To improve the management of risk, the Australian Rail Track Corporation accelerates the implementation of a fit-for-purpose risk management system for the Inland Rail programme.

Australian Rail Track Corporation response: Agreed in principle.

Recommendation no.2

Paragraph 3.14

To improve records management, the Australian Rail Track Corporation:

- revisits the scope and timeline of the Electronic Content Management review to incorporate the Inland Rail programme; and

- reviews and updates its records management policies and procedures.

Australian Rail Track Corporation response: Agreed in principle and underway.

Recommendation no.3

Paragraph 3.32

To support transparency and value for money in contracting arrangements for the construction of the Inland Rail, the Australian Rail Track Corporation:

- develops and implements policies and procedures that have suitable regard to Commonwealth procurement and contract management standards, recognising that the company is not bound by the Commonwealth Procurement Rules;

- implements full functionality and controls available in procurement and contract management systems modules; and

- monitors performance in procurement and contract management through increased internal audit activity and / or the implementation of a quality assurance process.

Australian Rail Track Corporation response: Agreed in principle with qualification.

Summary of entity responses

13. A summary of entity responses are below, with full responses provided at Appendix 1.

Department of Infrastructure and Regional Development

The Department supports the recommendations provided in the report. As the report notes as part of its delivery of Inland Rail, the ARTC has already commenced action that will improve ARTC's procurement practices and risk management processes. I expect the ARTC Board will have due regard to the report and will take action for the timely completion of the report's recommendations. Further to this, I expect the ARTC Board will provide regular advice to the Shareholders Ministers confirming how and when all of the recommendations will be implemented.

Department of Finance

Finance agrees with the ANAO's recommendations. The Government announced in the 2017–18 Budget that it will invest a further $8.4 billion in equity in the Australian Rail Track Corporation to deliver the Inland Rail project. The ANAO's findings will assist agencies and the ARTC, and will inform appropriate oversight and governance arrangements related to the delivery of the project. To this end, a Secretary-level Sponsors Group, including the Chairperson of the ARTC, has been established to closely monitor progress of the project.

Australian Rail Track Corporation

ARTC takes audit recommendations very seriously and has an ongoing commitment to continuous improvement. ARTC acknowledges your findings and your recognition in the body of the report that process improvements have already been made. At the same time, ARTC acknowledges the positive feedback on governance and the appropriate management of grant funding.

As a general observation, ARTC considers the findings do not adequately reflect the uncertainty and lack of clarity associated with the initial funding, longevity and responsibilities for the Programme during the period when decisions were being made as to the future of the Inland Rail project. Indeed, it was only in May 2016 that ARTC was confirmed as the delivery agency and in the May 2017 Budget that the funding commitment was confirmed. This imposed constraints on ARTC's approach to procurement, contract management and the project's risk management approach.

Notwithstanding this high level of uncertainty, 45 out of 54 tested procurements were competitively sourced through tenders, standing offers and quotes. Within this context, ARTC was also focussed on achieving value for money. Even though, as observed, ARTC is not obliged to follow the Commonwealth Government Procurement Guidelines, subsequently, ARTC has sharpened its approach to Inland Rail's procurement and contract management. In addition, monthly management reporting is being enhanced.

Finally, while the Ministers' funding agreement was not concluded, detailed scope of works and milestone deliverables were developed as part of each project proposal report (PPR).

Key learnings and opportunities for improvement for Australian Government entities

Below is a summary of key learnings identified in this audit report that may be considered by other government business enterprises when developing and implementing pre-construction programs.

Group title

Governance arrangements

Key learning reference

Group title

Procurement

Key learning reference

1. Background

Inland Rail programme

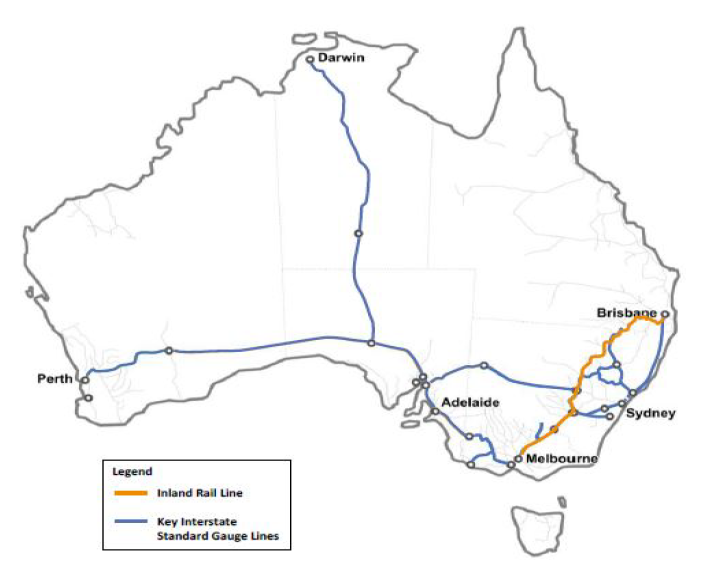

1.1 The Inland Rail programme is to construct an inland rail line from Melbourne to Brisbane, covering a total distance of approximately 1700 kilometres—constructing around 700 kilometres of new track, providing major upgrades to 300 kilometres of existing track and enhancement works on the remaining 700 kilometres. The Inland Rail programme is estimated to cost around $10 billion over ten years.1 Once complete, this will allow freight to be moved by rail between Melbourne and Brisbane in under 24 hours, and improve south-east Queensland’s rail link with Adelaide and Perth.

Figure 1.1: Australia’s existing rail network and planned Inland Rail connection

Source: Australian Rail Track Corporation 2015 Inland Rail Programme Business Case, p. 10.

Table 1.1: Inland Rail programme service offer

|

Inland Rail programme service offer |

|

|

Reliability |

98% reliability—equivalent to that of road. |

|

Price |

Reduced rail costs for non-bulk, intermodal freight travelling between Melbourne and Brisbane of $10 per tonne. |

|

Transit time |

|

|

Freight availability |

Freight departure and delivery when the market wants it. |

Source: Inland Rail Implementation Group Report to the Australian Government, 2015, p. viii.

1.2 The business case for the Inland Rail programme notes that ‘an inland railway between Melbourne and Brisbane has been considered for more than 100 years, first being formally considered in 1902’.2 More recent key studies underpinning the Inland Rail programme are shown in Table 1.2. The Inland Rail programme has also been included in Infrastructure Australia’s Infrastructure Priority List since May 2016.3

Table 1.2: Key studies for the Inland Rail programme

|

Studies, reports and funding commitments |

|

|

June 2006 |

North-South Rail Corridor Study June 2006. The study examined future transport demand along the Melbourne–Sydney–Brisbane corridor. The study was conducted by Ernst & Young, Hyder Consulting Pty. Ltd. and ACIL Tasman Pty. Ltd., at a cost of $4.3 million. The study identified a far western corridor through Parkes in western NSW as the preferred corridor for Inland Rail. |

|

July 2010 |

Melbourne-Brisbane Inland Rail Alignment Study, July 2010. The study determined the optimum alignment (within the preferred corridor identified in the June 2006 study) and likely economic and financial performance of the venture. The study was conducted by the Australian Rail Track Corporationa at a cost of $12.7 million. |

Note a: With consultants: ACIL Tasman; Aurecon; Halcrow; Parsons Brinckerhoff; and PricewaterhouseCoopers.

Source: ANAO from publicly available reports, media releases and Australian Government budget measures.

Pre-construction phase of the Inland Rail programme

1.3 In September 2013, the Australian Government announced a commitment of $300 million for the Melbourne to Brisbane inland railway, to fund activities required to get the Inland Rail programme ready to commence construction (at the completion of the activities or at a future point). Referred to as the pre-construction (or development) phase of the Inland Rail programme, it comprises detailed corridor planning, engineering design, environmental assessments and pre-construction activities, including land acquisition.

1.4 In November 2013, the Australian Government announced the establishment of the Inland Rail Implementation Group4, and that ‘the Australian Rail Track Corporation will, under the guidance of the Implementation Group, work with interested parties to construct the Inland Rail project through a staged 10-year schedule’.5

1.5 In the 2014 Federal Budget the Australian Government committed the (previously announced) $300 million in grant funding for the pre-construction phase of the Inland Rail programme over four years (2014–15 to 2017–18), with subsequent funding provisions in the:

- 2016 Federal Budget, up to $594 million in equity funding over three years (2017–18 to 2019–20) to progress the Inland Rail programme including land acquisition, the continuation of pre-construction, and due diligence activities6; and

- 2017 Federal Budget, $8.4 billion in equity funding over seven years (2017–18 to 2024–25) to deliver the programme in its entirety.

Inland Rail Implementation Group, Report to the Australian Government

1.6 In August 2015, the Inland Rail Implementation Group presented its Report to the Australian Government (the report).7 The group had been established to:

… lead the development of a 10-year delivery programme for the Inland Rail by the Australian Rail Track Corporation (ARTC) and prepare the business case. Responsibilities included settling the alignment, determining construction priorities, commencing pre-construction and monitoring development of the programme. The Deputy Prime Minister also requested that a dedicated freight route connecting the interstate line with the Port of Brisbane be examined.8

1.7 The report included that the ‘Implementation Group is satisfied that Inland Rail represents a necessary, cost-effective and industry-supported response to the challenge of the growing national freight task’, noting that ‘an Australian Government decision as to whether or not to proceed with Inland Rail represents a significant and complex challenge with respect to the scale, timing and financial implications of the project’.9

Context for the delivery of the pre-construction phase of the Inland Rail programme

1.8 Among other things, the Inland Rail Implementation Group was tasked with providing advice on options for the expenditure of the initial $300 million in grant funding—there were no defined objectives for the funds, other than to progress the inland rail. At finalisation of the group’s report (August 2015), $41.2 million of the initial $300 million had been allocated and largely spent, including on costs of developing a ten-year delivery schedule and finalising a business case.

1.9 The report provided three options for ‘how best to utilise the balance of the funds’, subject to the Australian Government deciding to: proceed to full construction in the immediate future; defer construction to a later date; or not progress the Inland Rail connection. Recommendations outlining possible alternatives for expenditure of the remainder of the $300 million would depend on which of the three options applied.10

1.10 The report also commented that ‘the delivery model has been developed with ARTC as the delivery agent at the request of Government, and while this is a viable option, it is not the only option’, suggesting a dedicated delivery authority as one alternative.11 However, on 3 May 2016 the Government announced the additional $594 million for Inland Rail, and that the project would be delivered through the ARTC in partnership with the private sector.12

1.11 In effect, the Government’s key decisions about the Inland Rail programme—would the ARTC continue to have carriage of the programme, and would the rail link be completed—were finalised in May 2016 and in the May 2017 Federal Budget respectively, and had to be factored into the timing of the payment of grant funds for the pre-construction phase of the programme and the ARTC’s management of pre-construction activities.

Australian Rail Track Corporation

1.12 The ARTC was established in 1998 as part of an Australian Government reform package for rail transport13, with agreements between the Commonwealth and state governments to form a ‘one stop shop’ for all train operators wanting to access a standardised national interstate rail network. Initially, the ARTC managed rail lines in Victoria and South Australia (including those between Albury and Melbourne, Broken Hill to Whyalla, Adelaide to Alice Springs and Port Augusta to Kalgoorlie) experiencing substantial growth in September 2004 when it entered into a 60 year lease with the New South Wales Government to operate and maintain sections of the state’s rail lines, including the Hunter Valley freight line.14

1.13 As at May 2017, the ARTC managed more than 8500 kilometres of standard gauge track in mainland Australia15 (selling access to train operators; developing new freight business; managing capital investment in the network; managing train operations; and maintaining the rail network). The ARTC describes its services as ‘facilitating the movement of a range of commodities including general freight, coal, iron ore, other bulk minerals and agricultural products. Our network is also important in providing access for interstate and inter-city passenger services’.16

Legislative and policy context

1.14 The ARTC is a Commonwealth company, established by the Commonwealth under the Corporations Act 2001 and is classified as a Government Business Enterprise (GBE).17 A GBE is legally separate from the Commonwealth, but is usually linked to implementing government policy, where intervention is deemed appropriate due to: high barriers to entry; market failure (or no market at all); infrastructure investments with lower rates of return; and / or other policy considerations of Government.18

1.15 The Australian Government’s relationship with GBEs is similar to the relationship between a holding company and its subsidiaries, features of which include:

- a strong interest in the performance and financial returns of the GBE;

- reporting and accountability arrangements that facilitate active oversight by the shareholder;

- action by the shareholder in relation to the strategic direction of its GBEs where it prefers a different direction from the one proposed;

- management autonomy balanced with regular reporting of performance to shareholders; and

- boards that are accountable to shareholders for GBE performance, and shareholders that are accountable to Parliament and the public.19

1.16 All ARTC company shares are owned by the Commonwealth of Australia, represented by the Minister for Finance and the Minister for Infrastructure and Transport. The Shareholder Ministers and their departments—Department of Finance and Department of Infrastructure and Regional Development respectively—have joint oversight responsibilities for the ARTC’s operations.20 The:

- Department of Finance’s primary tasks in relation to GBE’s includes to: provide sound strategic and analytical advice to the Minister for Finance, in particular by engaging with the GBEs, and ensure that there is a robust and sound governance framework in place by initiating change and contributing to policy development21; and

- Department of Infrastructure and Regional Development, as the Portfolio department in which the ARTC operates, has a more operational role in: ensuring that the ARTC meets the Government’s policy objectives effectively; builds shareholder value and ensures the ongoing sustainability of the business; and utilises resources in an efficient, effective, economical and ethical manner.22

1.17 The Corporations Act 2001 is the primary regulatory framework for Commonwealth companies. The Public Governance, Performance and Accountability Act 2013 (Chapter 3) sets out requirements that Commonwealth companies also have to comply with to meet appropriate standards of public sector accountability.23 The Department of Finance maintains a resource management guideline for GBEs on board and corporate governance, financial governance and planning and reporting: RMG-126 Commonwealth GBE governance and oversight guidelines.24

Administrative arrangements

1.18 Internal governance of the ARTC is provided through an eight-member Board of Directors25 that ‘provides stewardship, strategic leadership, governance and oversight of GBEs, while acting also as a bridge between Commonwealth policy making and operational implementation’.26

1.19 The operations of the company are managed through the ARTC’s Executive Committee that comprises the Chief Executive Officer (who is also a member of the ARTC Board) and other executive level managers. As at May 2017, the structure of the company reflected: legal services and corporate affairs reporting directly to the CEO; two business units, Hunter Valley and Interstate; and four support divisions providing a range of corporate services across the company. Going forward, from July 2017, the Inland Rail programme will be established as a third business unit within the ARTC, headed up by a Chief Executive Officer, reporting to the ARTC Chief Executive Officer / Managing Director and a Chief Financial Officer for the programme.

1.20 As at July 2017, the ARTC (including for the Inland Rail programme) had 1236 employees, and maintained premises in some 60 locations across Australia, including seven rest houses, 27 provisioning centres for staff working on rail maintenance, 16 sub-depots, three network control centres and six main offices.

Funding

1.21 The ARTC is funded through a combination of rail access fees charged to commercial train operators and coal producers, Australian Government equity contributions and/or direct grants related to specific capital projects, and other income (including interest revenue and insurance recoveries), shown in Table 1.3 for 2014–15 to 2016–17.

Table 1.3: ARTC income and equity funding 2014–15 to 2016–17

|

|

2014–15 $ million |

2015–16 $ million |

2016–17 $ milliona |

|

Rail access fees |

758.4 |

755.7 |

713.8 |

|

Government grants |

54.6 |

69.5 |

85.6 |

|

Other income |

45.2 |

30.1 |

26.8 |

|

Equity injections |

0.0 |

0.0 |

81.0 |

|

Total revenue and other income |

858.2 |

855.3 |

907.2 |

Note a: Draft end-of-year results, as at 2 August 2017.

Source: ANAO from the ARTC Annual Report 2015–16, Consolidated Income Statement, p. 51; and information provided by the ARTC for 2016–17.

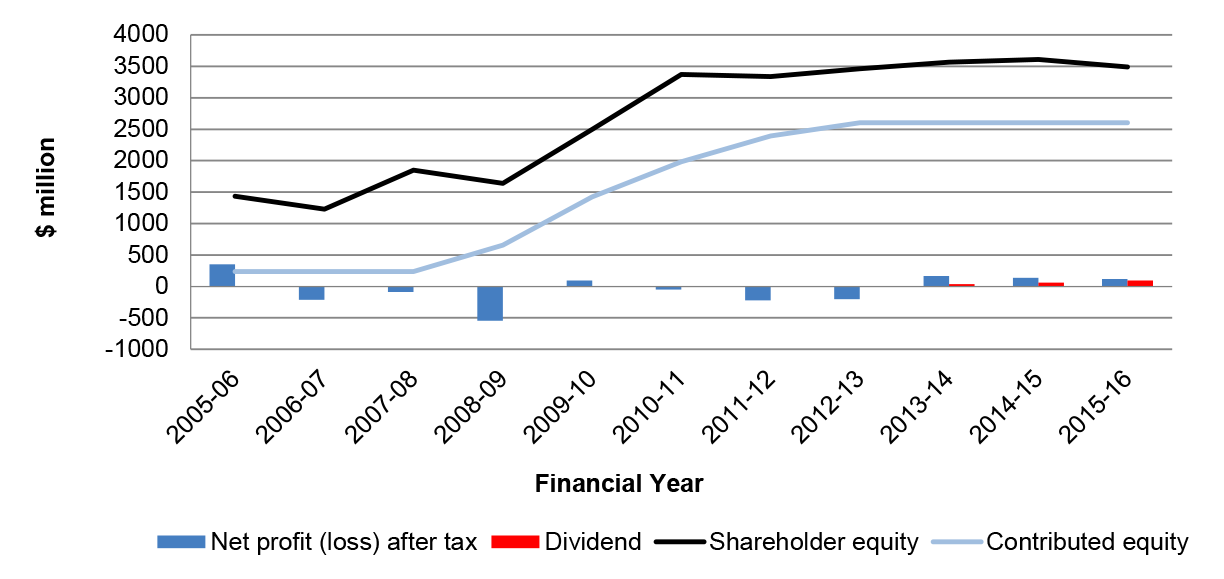

1.22 Through work funded from the ARTC’s own sources of revenue, grant funding from the Australian Government27, equity injections28 and an agreed nine year dividend ‘holiday’ prior to 2013–14, the ARTC has undertaken projects to upgrade freight lines. Major projects it has undertaken include the substantive completion, in 2013–14, of a $7 billion investment programme to repair, upgrade and expand capacity on the Hunter Valley and Interstate rail networks.29

1.23 The ARTC’s financial performance for 2005–06 to 2015–16, the value of the dividend paid to the Australian Government, and contributed and total shareholder equity over the same period is shown in Figure 1.2.

Figure 1.2: ARTC financial performance, 2005–06 to 2015–16

Source: ARTC Annual Reports, 2005–06 to 2015–16.

Funding for the pre-construction phase of the Inland Rail programme

1.24 The ARTC accesses grant funding for the pre-construction phase of the Inland Rail programme through submissions, referred to as Project Proposal Reports (that set out milestone deliverables), to the Department of Infrastructure and Regional Development. The department assesses the Project Proposal Reports and advises the Minister for Infrastructure and Transport, who then decides whether funding should be approved.

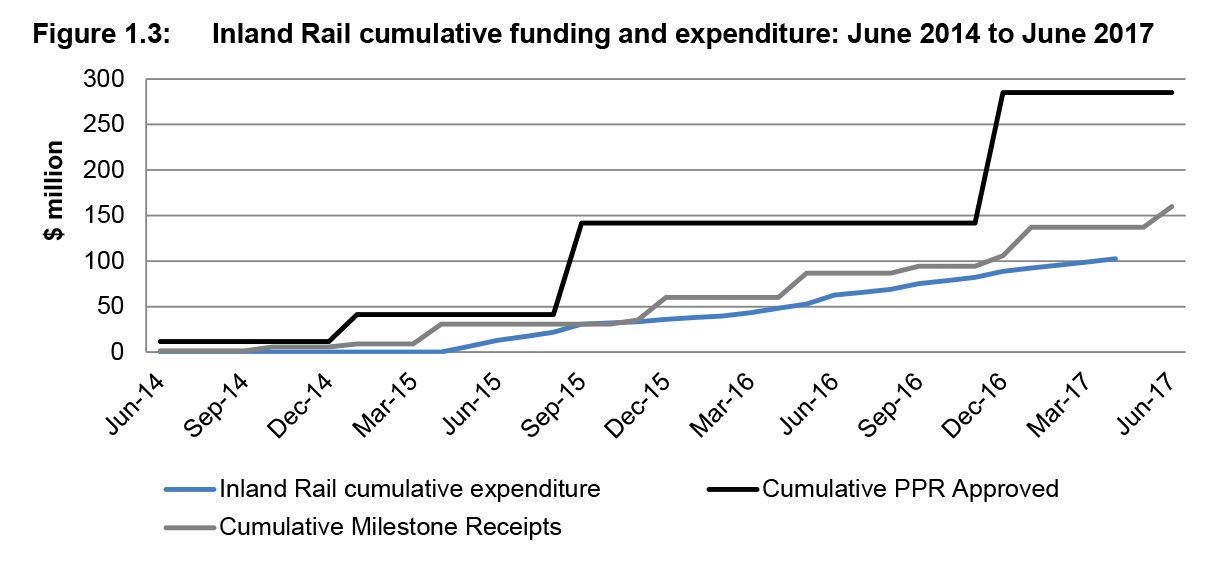

1.25 As at July 2017, the ARTC had submitted four Project Proposal Reports for the pre-construction phase of the programme of which, as at June 2017, $285 million had been approved by the Minister, and $160 million paid (against milestone deliverables) to the company (Figure 1.3).

Figure 1.3: Inland Rail cumulative funding and expenditure: June 2014 to June 2017

Source: ANAO, from information from the ARTC and the Department of Infrastructure and Regional Development.

1.26 The majority of pre-construction activities are being conducted through contracted services procured by the ARTC (including for engineering and design work), with an increase (as the pre-construction phase progressed) in contracting activity, governance and oversight arrangements, and ARTC personnel working on the programme. The Australian Government’s commitment in May 2017 to the full Inland Rail means the pre-construction phase of the programme will not have a discrete completion date, but will merge into construction mode during 2017–18.

1.27 Achieving value for money in the expenditure of public funds should be a key consideration in all aspects of the management of the programme, including procurement activity. Finance, on its website30, describes that to achieve a value for money outcome, procurements should: encourage competition and be non-discriminatory; use public resources in an efficient, effective, economical and ethical manner that is not inconsistent with the policies of the Commonwealth; facilitate accountable and transparent decision making; encourage appropriate engagement with risk; and be commensurate with the scale and scope of the business requirement.

Audit objective, criteria and approach

1.28 The audit objective was to assess whether value for money was being delivered by the ARTC’s management of the pre-construction phase of the Inland Rail programme. To form a conclusion against the audit objective the ANAO examined whether:

- governance arrangements were appropriate, and administration of grant funding was effective; and

- the ARTC’s procurement activities provided value for money and were supported by Information and Communications Technology systems and appropriate policies and procedures.

1.29 The audit focused on the: overarching governance arrangements for funding and delivering the pre-construction programme; and procurement activities, which have comprised the majority of the expenditure to date. The Australian Government’s policy decisions to: commit to, and to fund the construction of the full Inland Rail; and deliver the programme through the ARTC are not within the scope of this audit.

1.30 In conducting the audit, the ANAO: examined relevant documentation from the ARTC, Department of Infrastructure and Regional Development, and Department of Finance; interviewed ARTC staff based in Sydney, Newcastle, Brisbane and Adelaide; and interviewed officers from the Department of Finance and the Department of Infrastructure and Regional Development based in Canberra.

1.31 The audit was conducted in accordance with the ANAO’s Auditing Standards at a cost to the ANAO of approximately $580 000.

1.32 The team members for this audit were Michelle Mant, Alice Bloomfield, David Hokin, Judy Jensen and Andrew Morris.

2. Governance and funding arrangements

Areas examined

This chapter examines the governance arrangements supporting the pre-construction phase of the Inland Rail programme, processes for providing grants funding for the programme, and the management of costs, property and staffing requirements.

Conclusion

Governance arrangements for the pre-construction phase of the Inland Rail programme were appropriate, although there was not timely implementation of the Minister’s decision that a funding agreement be developed between the Department of Infrastructure and Regional Development and the Australian Rail Track Corporation. The Australian Government’s longer term intent with regard to the delivery and full construction of the Inland Rail was appropriately considered, including through the administration of grant funding. There could have been more emphasis on achieving value for money in procurement and contracting activities, including for the ARTC’s contracting of staff for the programme, and improved planning for the leasing of property.

Areas for improvement

The ANAO made one recommendation aimed at improving the management of risk for the Inland Rail construction programme (paragraph 2.32). The ANAO also suggested that, to support the full construction of the Inland Rail: the level of technical knowledge and expertise in the ARTC to manage the programme and that available to the government to oversight it, should be regularly reviewed (paragraph 2.18); the Department of Infrastructure and Regional Development should clarify the status of funding agreements (paragraph 2.43); and the ARTC should develop a property plan for the Inland Rail programme to ensure value for money in its office accommodation (paragraph 2.70).

Were there appropriate governance arrangements supporting the pre-construction phase of the Inland Rail programme?

Governance arrangements oversighting the pre-construction phase of the Inland Rail programme were appropriate, in so far as they adapted to the different stages of the implementation of the programme, and considered the Australian Government’s interests with regard to longer term decisions about the delivery of the complete Inland Rail. There was no evidence however, that due consideration had been given to matters raised about the skills and status of committee members, specifically in relation to departmental representation. There could also have been more emphasis on achieving value for money in procurement and contracting activities. The ARTC’s internal governance arrangements were appropriate, with a high level of engagement by the company’s Board throughout the pre-construction phase. The ARTC is strengthening its processes to manage risk, and needs to implement a suitable system to support the management of risk in the Inland Rail programme.

2.1 To assess whether there were appropriate governance arrangements supporting the pre-construction phase of the Inland Rail programme, the ANAO examined:

- governance arrangements within the ARTC (including reporting to the Board) and between the ARTC and Shareholder Ministers’ departments;

- the functioning of the ARTC’s Audit and Compliance Committee; and

- the ARTC’s management of risk.

Governance arrangements

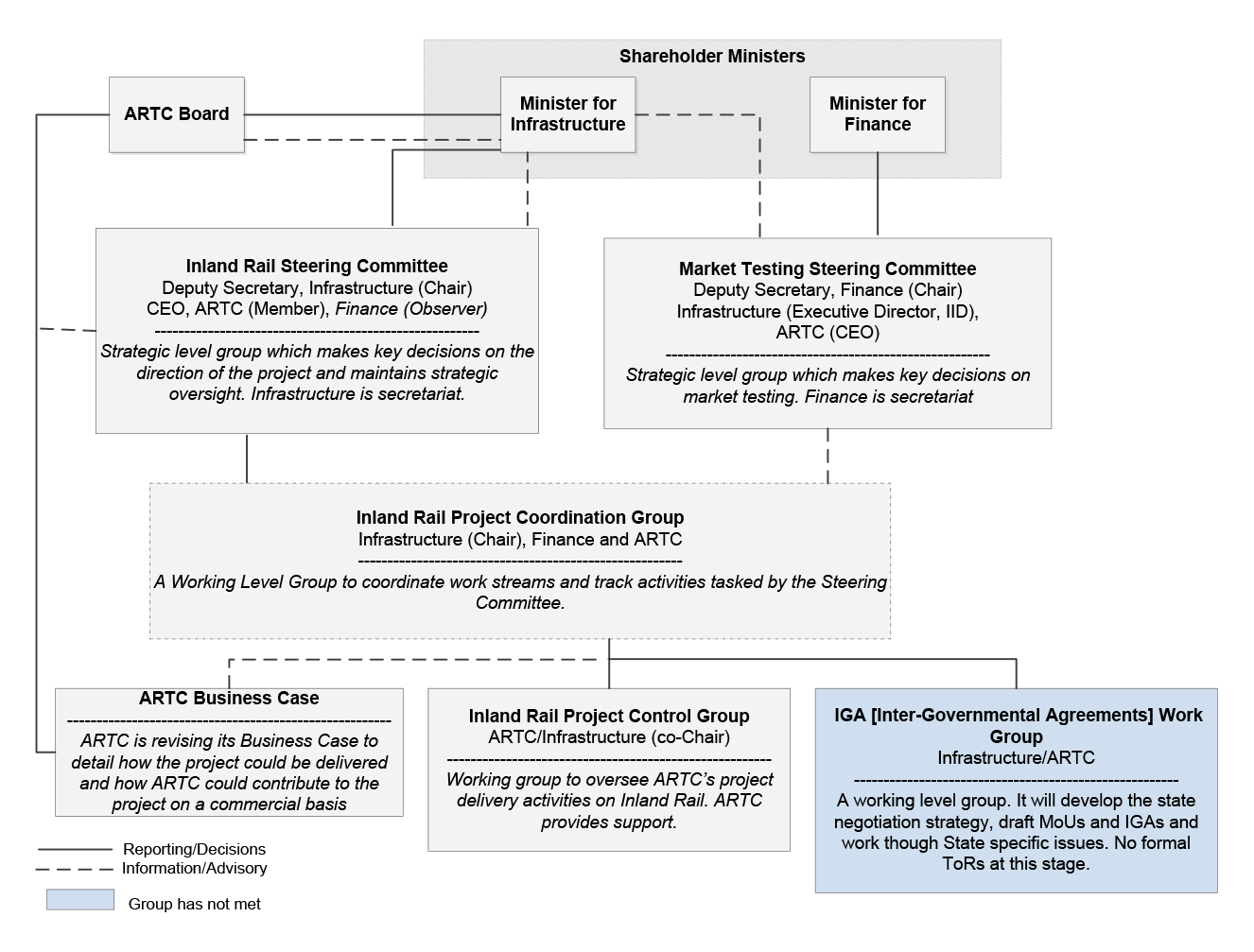

2.2 Governance of the pre-construction phase of the Inland Rail programme was provided through various groups and committees—internal to the ARTC, and jointly with the Department of Finance (Finance) and the Department of Infrastructure and Regional Development (Infrastructure). The groups and committees, and overall governance structure are illustrated in the:

- ARTC Governance Model, Presentation to the Australian National Audit Office, 3 May 2017, (updated 2 August 2017): governance arrangements over four phases of the Inland Rail programme (Figure 2.1); and

- Department of Infrastructure and Regional Development, Interagency Governance Structure (Figure 2.2).

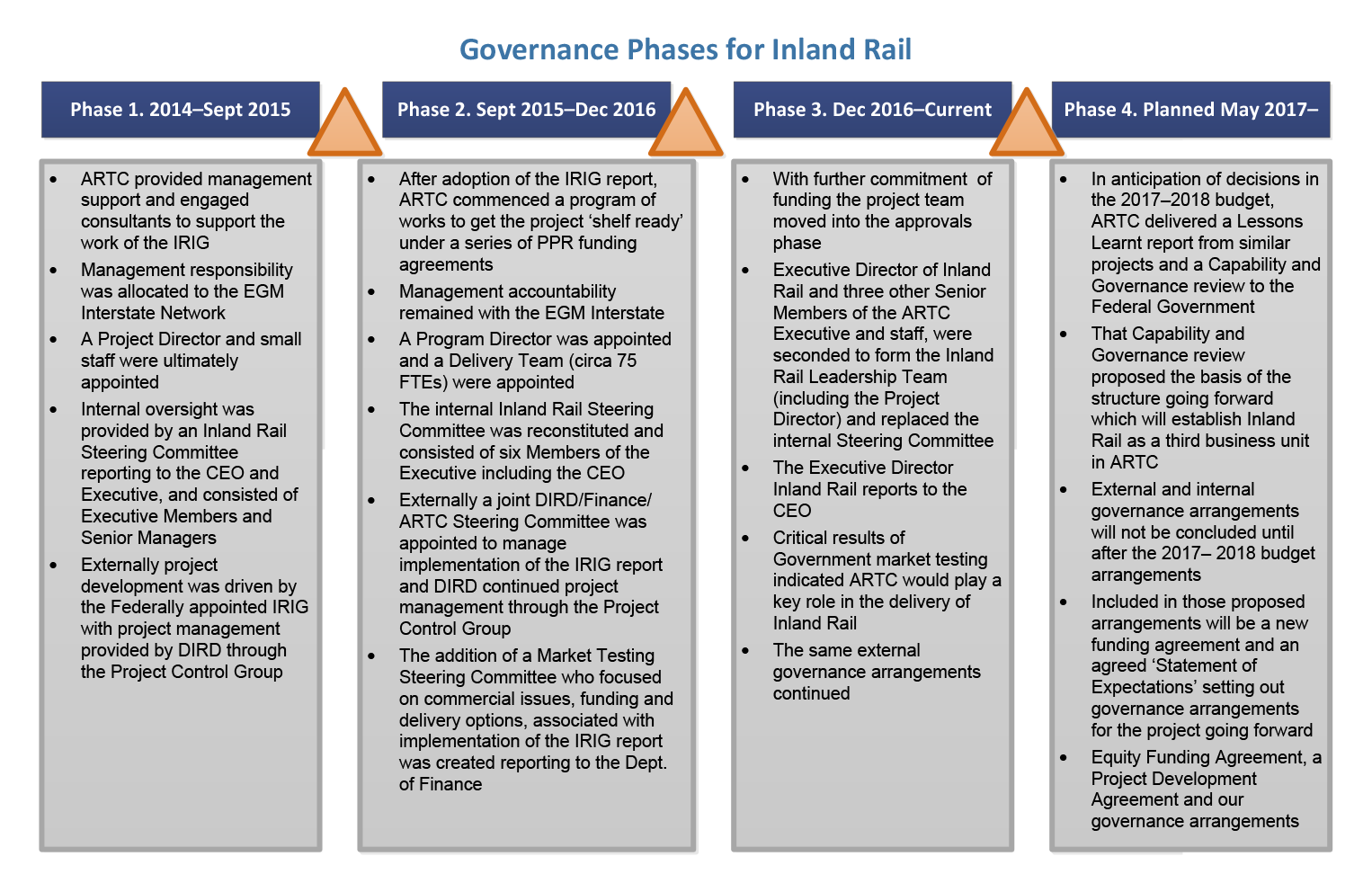

2.3 The two figures provide a different perspective of the governance arrangements, including that the ARTC presentation shows arrangements within the company, while the Infrastructure figure only shows the joint departmental / ARTC arrangements. Eight of the groups and committees identified in Figures 2.1 and 2.2 and the periods over which they functioned, are shown in Figure 2.3. Together, these figures show that there were a number of governance groups and committees for the pre-construction phase of the Inland Rail programme.

Figure 2.1: Governance Phases for the Inland Rail programme—2014 to August 2017

Note: ‘IRIG’: Inland Rail Implementation Group; ‘EGM Interstate Network’: Executive Group Manager of the Interstate Network Branch; ‘DIRD’: Department of Infrastructure and Regional Development (also referred to as Infrastructure).

Source: ARTC, ARTC Governance Model, Presentation to the Australian National Audit Office, 3 May 2017, updated 2 August 2017.

Figure 2.2: Inland Rail programme governance, May 2017

Note: As at August 2017, Infrastructure advised that the ARTC Business Case work stream was complete, and the Inter-Governmental Agreements working group commenced in late 2016.

Source: Department of Infrastructure and Regional Development.

Figure 2.3: Periods over which the governance groups and committees functioned

Note: DIRD, Department of Infrastructure and Regional Development (Infrastructure).

Source: ANAO analysis, from minutes of the meetings of each group.

2.4 The Terms of Reference for, or purpose of, each group or committee is at Table 2.1.

Table 2.1: Outline of governance groups for the Inland Rail pre-construction programme

|

Committee/Group |

Terms of reference / purpose |

|

Joint departmental / ARTC governance arrangements |

|

|

Inland Rail Implementation Group (10 meetings) |

Established by the Deputy Prime Minister to lead the development of a 10-year delivery programme for Inland Rail by the ARTC, and prepare the business case. |

|

Inland Rail Steering Committee (19 meetings) |

Established to provide strategic direction and oversight for the Melbourne to Brisbane Inland Rail programme. Specifically, the committee will oversee the delivery of a range of activities that the government announced in the 2016 Federal Budget to ensure that the government will be in a position to make decisions about the delivery, funding and financing of the project in the 2017 Budget. |

|

Market Testing Steering Committee (10 meetings) |

Established to provide strategic oversight and guidance to the market testing, funding review and capability review (the reviews) that are being undertaken as part of the Melbourne to Brisbane Inland Rail Project. |

|

Inland Rail Project Coordination Group (no minutes kept) |

Formed as a weekly working level group to coordinate work streams and track activities tasked by the Inland Rail Steering Committee. Maintains a register of actions for the group. |

|

Inland Rail Project (or Programme) Control Group (18 meetings) |

Facilitates the delivery and provides management oversight for all phases of the Melbourne to Brisbane Inland Rail programme. Reports to the Inland Rail Steering Committee, and provides the main point of governance and programme review between Infrastructure and the ARTC. |

|

DIRDa Inland Rail Internal Steering Committee (10 meetings) |

Formed to provide oversight and strategic governance for the Department’s role in Inland Rail, including to ensure that business objectives were adequately addressed and that the project remained appropriately resourced and on target. Meetings were suspended on 7 June 2016 with the comment that ‘members can provide feedback out of session’. |

|

ARTC internal governance arrangements |

|

|

ARTC Internal Steering Committee (35 meetings) |

To assist in arranging governance of the Inland Rail programme, particularly risk and value for money. |

|

Inland Rail Leadership Team (12 meetings) |

Team created as the first stage of a transition to creating Inland Rail as a business unit within the ARTC. Role of the team set out in a Decision Process Chart, which includes the team will act as the Project Steering Committee. Met weekly by phone and monthly face-to-face. |

Note a: DIRD, Department of Infrastructure and Regional Development (Infrastructure).

Source: ANAO, from documentation provided by the ARTC, Infrastructure and Finance.

Departmental oversight

2.5 The ANAO’s review of the terms of reference and meeting minutes of the joint groups and committees reflected a logical progression as the programme progressed. For example:

- the Inland Rail Implementation Group (group 131) ceased with the finalisation of the group’s report to the Australian Government; and

- the senior level Inland Rail Steering Committee (group 2) was established to provide oversight of the programme in February 2016, following a request of the Minister for Infrastructure and Regional Development in approving $100.6 million in grant funding for the ARTC.32

2.6 The ANAO review also identified references to the challenges involved in effectively overseeing the programme. For example, the report of the Inland Rail Implementation Group, August 2015, included that ‘Inland Rail is a complex project’ and that ‘effective governance will be critical to ensuring that it delivers the intended outcomes and is delivered cost effectively’. The report stated:

An important aspect is that there is an effective programme management office that has effective oversight with the necessary skills to take and be accountable for the many detailed decisions that will occur as the project is delivered. The Implementation Group recommends that the Government establish a programme delivery office for Inland Rail that has the necessary skills (including commercial, financial and technical), supported by a governance structure that is accountable for outcomes and delivery on-time and on-budget.

2.7 In a similar vein, the minutes of the last meeting of the DIRD Internal Steering Committee (11 May 2016) (group 6) record discussion about ongoing governance arrangements for Inland Rail and the need for independent expertise and advice. There was an action item ‘to review governance arrangements with the assistance of an independent strategic advisor and taking into account suggestions from members of the group’. Further discussion on governance arrangements included that: members of the committee (group 6) expressed concern that the ARTC had member status rather than observer status of the high-level Inland Steering Committee (group 2), and that an independent rail expert would enhance this committee. Minutes of the high-level Inland Rail Steering Committee (group 2):

- show that the committee had two members (the Secretary of Infrastructure and the Chief Executive Officer of the ARTC) with other attendees from Infrastructure and the ARTC as ‘participants’ and a representative from Finance with ‘observer’ status; and

- do not record any participation in the group by an independent rail expert.

2.8 The ANAO review also identified that departmental oversight of ARTC’s procurement and contract management could have been better. Terms of reference for the Inland Rail Project Control Group set out 11 ‘roles and responsibilities’, of which three relate to specific aspects of the management of procurement and contract variations.33 A review of the minutes of 16 meetings of the group showed that contract variations were discussed in eleven meetings. The discussions did not relate to individual contracts, rather to changes to Milestone Package deliverables. ANAO testing of 54 procurements (discussed in Chapter 3) found 24 of them were varied in excess of 50 per cent of the initial contract value, and no discussion of these variations is recorded in the minutes.

2.9 Overall, the joint governance arrangements for the pre-construction phase of the Inland Rail programme were appropriate, in so far as there was good representation of senior executive and operational staff to provide oversight and strategic direction for the programme. The groups and committees also adapted in response to the progression of the programme, and managed the Australian Government’s interests and longer term intent with regard to the delivery model and full construction of the Inland Rail.

2.10 There is no documented evidence, however, as to work undertaken to identify the ‘appropriate governance arrangements’ referred to by the Minister in 2016, or respond to the recommendation by the Inland Rail Implementation Group (group 1) to establish a programme delivery office with the ‘necessary skills’.34 There is also no record of consideration of securing the services of an independent rail expert, or of resolving whether the ARTC’s ‘membership’ status at the high-level Inland Steering Committee (group 2) was appropriate, with regard to responsibilities and accountabilities of Infrastructure to oversight the programme and the ARTC Board and senior executive to implement it.

2.11 There could also have been greater oversight of the ARTC’s procurement activities with respect to achieving value for money in contracting. Further, the development of a funding agreement between the Department and the ARTC (to agree project milestones and reporting arrangements) as requested by the Minister in June 2014 but not finalised until July 2017 (discussed later in this chapter), could have provided guidance on the outcomes associated with the $300 million grant funding (other than to progress the Inland Rail programme) and accordingly on key priorities for the pre-construction programme.

ARTC internal governance arrangements

2.12 In February 2017, the ARTC advised that the internal governance process for Inland Rail:

… mirrors that set by the parent ARTC body with modification only to meet any peculiarities that may arise due to the Programme Management / Programme Delivery and Procurement Delivery Strategies that are specifically involved with this Inland Rail Programme and its Projects. … Over the period under audit/review … higher-level Committee, Programme and Project organisational structures have changed several times to reflect the maturing nature of the Programme as it has progressed through the lifecycle phases of the ARTC Project Management Lifecycle. Therefore, and not surprisingly, committees at the governance, strategic management and management levels have changed their function and even reporting lines during the described maturation process; the latter specifically at the higher levels.

2.13 Consistent with this advice, the ARTC advised that the internal governance body for Inland Rail changed names several times. The ARTC Internal Steering Committee (group 7) met from 25 June 2014 to 4 May 2016, when it became the Inland Rail Executive Group, which met between 27 May 2016 and 5 December 2016. Changes within the ARTC in response to the needs of the programme then led to the creation of the Inland Rail Leadership Team (group 8), to transition to a new ARTC internal structure.

2.14 The ARTC provided over 300 documents related to these internal governance arrangements. The documentation provided records of meetings (including agenda items, action items, reports and minutes) from February 2014 to March 2017. A high-level review by the ANAO of the documentation noted discussion supporting the preparation and endorsement of the ARTC’s funding submissions (discussed later in this chapter).

2.15 The ARTC also provided an overview of the various means by which the company’s Board was kept informed of the progress of the Inland Rail programme and had input to decision making (Appendix 2). The ANAO reviewed 10 of the quarterly reports to the Board provided by the Interstate Network, from October 2014 to February 2017. All but one of the reports (February 2017) provided a summary of progress to date on the pre-construction phase of the Inland Rail programme: key achievements for the quarter; cumulative data on funds and expenditure; planned activities for the upcoming quarter; and risks associated with the programme.

Governance arrangements for the construction of Inland Rail

2.16 As at July 2017, the Australian Government and the ARTC are developing new governance arrangements to support the full construction of the Inland Rail programme, and the (almost) $9 billion in equity funding the Australian Government has committed to date. In response to the government’s announcement in May 2016 that it would deliver Inland Rail through the ARTC, Finance’s business advisor for the programme reviewed the outcomes of a capability and governance review35 undertaken by the ARTC Board to assess the ‘skills, corporate structure, shareholder arrangements, and capability and governance requirements in relation to the potential delivery models for Inland Rail’.

2.17 Key findings of the review, May 2017, included that: following recent recruitment to the ARTC Board, the Board has strong capabilities to provide strategic and governance oversight to the delivery of Inland Rail under delivery options outlined in the document; (for the options outlined) the ARTC executive management team will need to be augmented by the recruitment of a Chief Executive of the Inland Rail Business Unit that will report directly to the ARTC Group Chief Executive Officer and Managing Director; and ARTC is well positioned to recruit to address current gaps in existing capability, and is better positioned to do so than if a new government entity were to be set up for Inland Rail.36

2.18 The Inland Rail programme is a significant national infrastructure initiative, and governance arrangements going forward will need to ensure that: the level of technical knowledge and expertise in the ARTC to manage the programme and that available to the government to oversight it, should be regularly reviewed; and there is clarity about outcomes and deliverables throughout the full construction of the Inland Rail.

ARTC internal audit function

2.19 The ARTC advised that the company’s Audit and Compliance Committee was established in June 2000, and the audit charter reviewed in 2013 to comply with the Public Governance, Performance and Accountability Act 2013 (PGPA Act) and PGPA Rule, with the current Charter finalised in November 2016.37 The results of a review of the roles and responsibilities of the audit committee, as set out in the Charter, against requirements of an audit committee under the PGPA Act and associated rules, are set out in Table 2.2.

Table 2.2: ARTC Audit Committee Charter compliance with PGPA Act requirements

|

Section |

Requirement |

Compliance |

|

PGPA Act |

||

|

92(1) |

The directors of a wholly-owned Commonwealth company must ensure that the company has an audit committee. |

Yes |

|

92(2) |

The committee must be constituted, and perform functions, in accordance with any requirements prescribed by the rules. |

Yes |

|

PGPA Rule |

||

|

17(1) |

The accountable authority of a Commonwealth entity must, by written charter, determine the functions of the audit committee for the entity. |

Yes |

|

17(2) |

The functions must include reviewing the appropriateness of the accountable authority’s: financial reporting; performance reporting; system of risk oversight and management; and system of internal control. |

Yes |

|

17(3) |

The audit committee must consist of at least three persons who have appropriate qualifications, knowledge, skills or experience to assist the committee to perform its functions. |

Yesa |

|

17(4)(b) |

On and after 1 July 2015, the majority of the members of the audit committee must, for a corporate Commonwealth entity, be persons who are not employees of the entity. |

Yes |

|

17(5) |

The following persons must not be a member of the audit committee: the accountable authority or, if the accountable authority has more than one member, the head (however described) of the accountable authority; the Chief Financial Officer (however described) of the entity; the Chief Executive Officer (however described) of the entity. |

Yes |

Note a: Audit Committee members had backgrounds in the rail industry (domestic and foreign), law, accounting, engineering and government advisory.

Source: ANAO analysis.

2.20 The ARTC develops a rolling three-year plan (for safety and non-safety audits) for internal audit. The plan is delivered by ARTC internal audit staff, through outsourcing arrangements, and is also co-sourced (joint internal / outsourced resources).

Internal audit reports

2.21 Of 87 internal (non-safety) audits completed from 2014–15 to 2016–17, only one dealt specifically with the Inland Rail programme—AM14 Inland Rail Programme Governance Framework, March 2015. This audit, and other ARTC internal audits, raised several issues affecting the administration of the programme that have also been identified by the ANAO in this performance audit.

2.22 The AM14 Inland Rail Programme Governance Framework audit identified: instances of work on contracts having commenced prior to execution of the contract; and scope to improve the governance structure, which at that time involved ‘two separate governance bodies’ (the Inland Rail Implementation Group and the ARTC’s internal steering committee). Details at Appendix 3.

2.23 Other ARTC internal audit reports with findings and action items relevant to matters discussed in this ANAO performance audit (also shown in Appendix 3) are:

- IM18 Systems Developed Outside of IT, February 2015: focused on a review of the policies, processes, and controls implemented by ARTC to address information security. Key findings in the report included limited awareness across the ARTC of the company’s Information and Communications Technology policies and procedures;

- FIN2 Procurement and Contract Execution, February 2015: focused on compliance with procurement and contract procedures for the procurement of goods and services in 2014. Key findings in the report concerned the use of inappropriate types of contracts; and

- FIN01 Procure to Pay, 21 March 2017: assessed the adequacy and effectiveness of the controls in place to manage the risks associated with: procuring goods and services, including processes to select suppliers and the execution of contracts; and paying for goods and services. Key findings in the report included a lack of key control documentation during the tender process; a lack of justification for single source procurement; and forms signed without appropriate delegated authority.

2.24 The ARTC maintains an Audit Management System (in the form of an Access database) to record and track actions from audit findings from internal non-safety audit reports. As at July 2017, all actions from the reports listed above were recorded as ‘Closed Validated’ in the system.38

2.25 The only audit specifically for Inland Rail in the 2016–17 work programme is AM09 Inland Rail Project Governance Framework.39 The objective of this audit is to assess the adequacy of aspects of the Inland Rail programme’s control environment, with the internal audit notice noting that ‘the Inland Rail project was officially recognised as an ARTC project in April 2016, and as such the scope of the internal audit will only include the period from April 2016. As at 2 August 2017, the ARTC advised that fieldwork is being finalised for this internal audit.

ARTC risk management

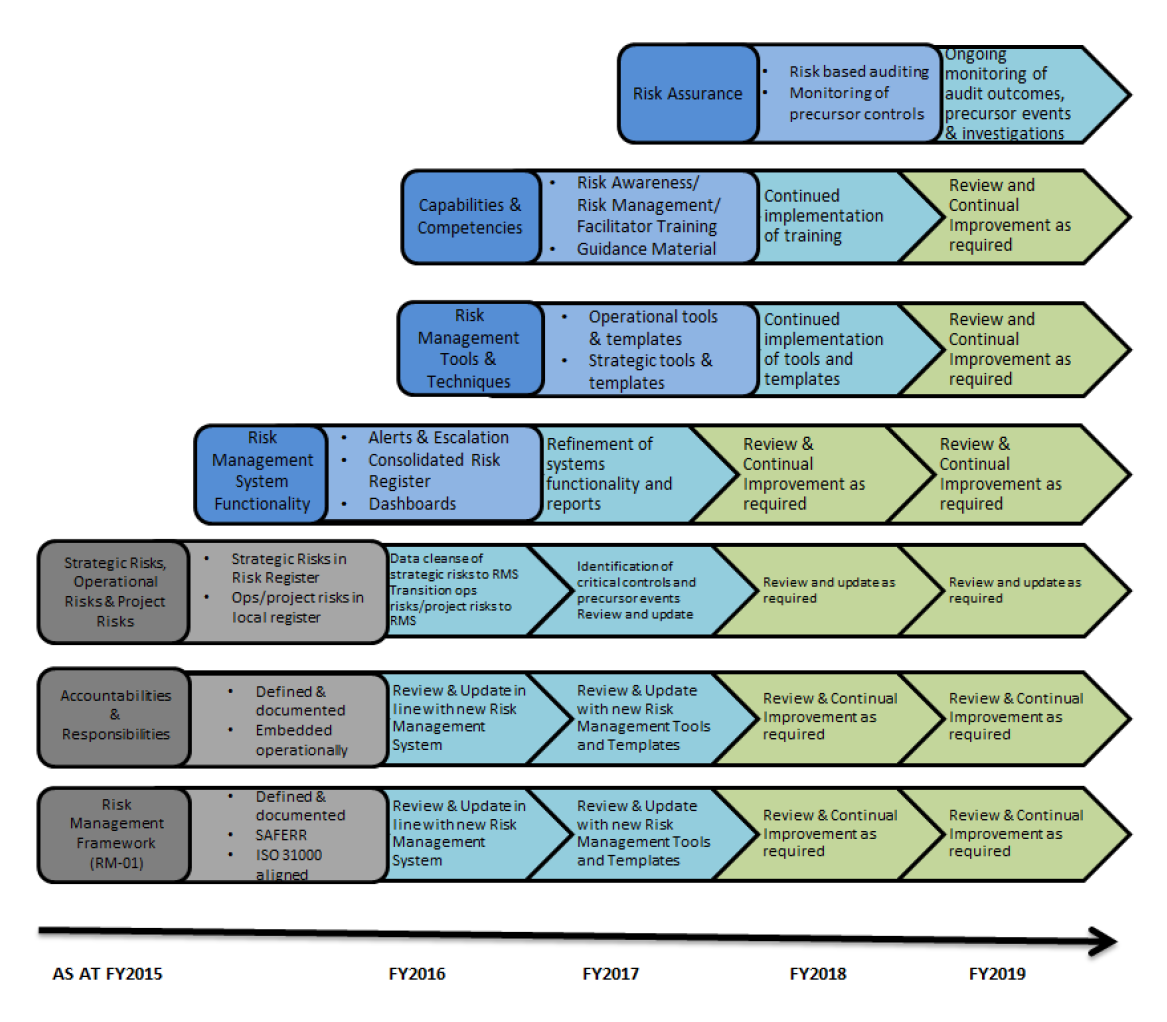

2.26 At the corporate level, the ARTC has developed a Risk Management Improvement Plan FY 2015/16 – FY 2019/20, (RSK-PL-001) dated 18 December 2015. The objective is to ensure that risks are managed ‘So Far As Is Reasonably Practicable’, with six key deliverables.40 The ARTC’s strategy to deliver the plan is at Appendix 4.41

2.27 Information on the ARTC’s management of risk is available on the company’s intranet, Connect. The ‘risk’ intranet page provides links to key documents, including the: Risk Management Framework, RSK-GP-004, 26 May 2016; Risk Management Improvement Plan; and a suite of new policies and procedures, replacing seven existing documents (that are still available on the site as at July 2017, for areas of the company that have not yet transitioned to the new Risk Management Framework).

2.28 Prior to the development and implementation of the risk management improvement plan, in 2015 the ARTC purchased an externally supplied risk management system, with up-front costs and annual fees payable each year over a five-year contract period (to 2020), as well as additional licence costs.42 The ARTC advised in July 2017 that: risks are being reviewed and updated as they are transitioned from the previous system43 to the current system; there have been delays in the roll out of the system; and business requirements have evolved since the initial requirements were identified in 2014.

2.29 For the management of risk in the Inland Rail programme, the ARTC has developed a programme specific Risk Management Plan (drafted early in 2015 and approved 5 April 2016) and does not use the current risk management system purchased in 2015. Instead, the ARTC maintains a risk register, in the form of a macro enabled Excel workbook, with the first entry recorded on 3 October 2014. The risk register is used in conjunction with the additional tools: Primavera Risk Analysis and @Risk for Monte Carlo simulations.44

2.30 As at 23 June 2017, over 1100 risks have been recorded in the register, of which less than 400 were still open. The ARTC advised in July 2017 that risks for the Inland Rail programme had been managed by a series of contracted risk managers, who brought their own approach and methodology to the task. As at July 2017, the current risk manager had been in the role for seven months, and had considerably enhanced the functionality and reporting capability of the register. To ensure the integrity of the register, the manager has sole edit rights to the register and has to manually manage all risk updates.

2.31 While the ARTC advised that the capability of the risk register is fit-for-purpose for the pre-construction phase of the Inland Rail programme, the company also advised that the register will not meet the needs of the full Inland Rail programme in the longer term, with greater demands placed on the risk system. The ARTC advised that discussions have begun on the way forward.

Recommendation no.1

2.32 To improve the management of risk, the Australian Rail Track Corporation accelerates the implementation of a fit-for-purpose risk management system for the Inland Rail programme.

Australian Rail Track Corporation response: Agreed in principle.

2.33 At the time of procurement of the new risk system, the Inland Rail programme was not confirmed as definitely proceeding and ARTC was not confirmed as the entity to deliver the programme.

2.34 Therefore specific requirements for functionality, analytic capabilities and system interoperability in relation to the management of the Inland Rail programme delivery risks were not considered. Additionally, management decisions were made to keep the Inland Rail risk register separate from the ARTC business units to readily facilitate handover to another entity, in the event ARTC was not selected to deliver the programme, as was requested by Government.

2.35 Risk continues to be managed effectively on the Inland Rail programme. However, with the programme now funded to proceed and ARTC confirmed to deliver the programme, ARTC is currently reviewing business needs for the ongoing management of the Inland Rail programme delivery risks and developing an appropriate risk management system for use going forward.

Were the grants for the pre-construction phase of the Inland Rail programme appropriately managed?

Grant funding was appropriately managed for each of the four funding packages provided for the pre-construction phase of the Inland Rail programme. There was extensive engagement between the ARTC and Infrastructure in preparing the funding submissions, and Infrastructure appropriately assessed the submissions and approved milestone delivery payments. Protecting the Commonwealth’s interests centred on how best to use the funds, given the status of the project over the longer term and the ARTC’s role in delivering it. However, high-level deliverables, outcomes and reporting arrangements were not developed through the Minister’s required funding agreement for the pre-construction phase, which could have supported greater emphasis on obtaining value for money in procurement activities associated with the milestone deliverables identified in the grant funding submissions.

Legislative and policy context

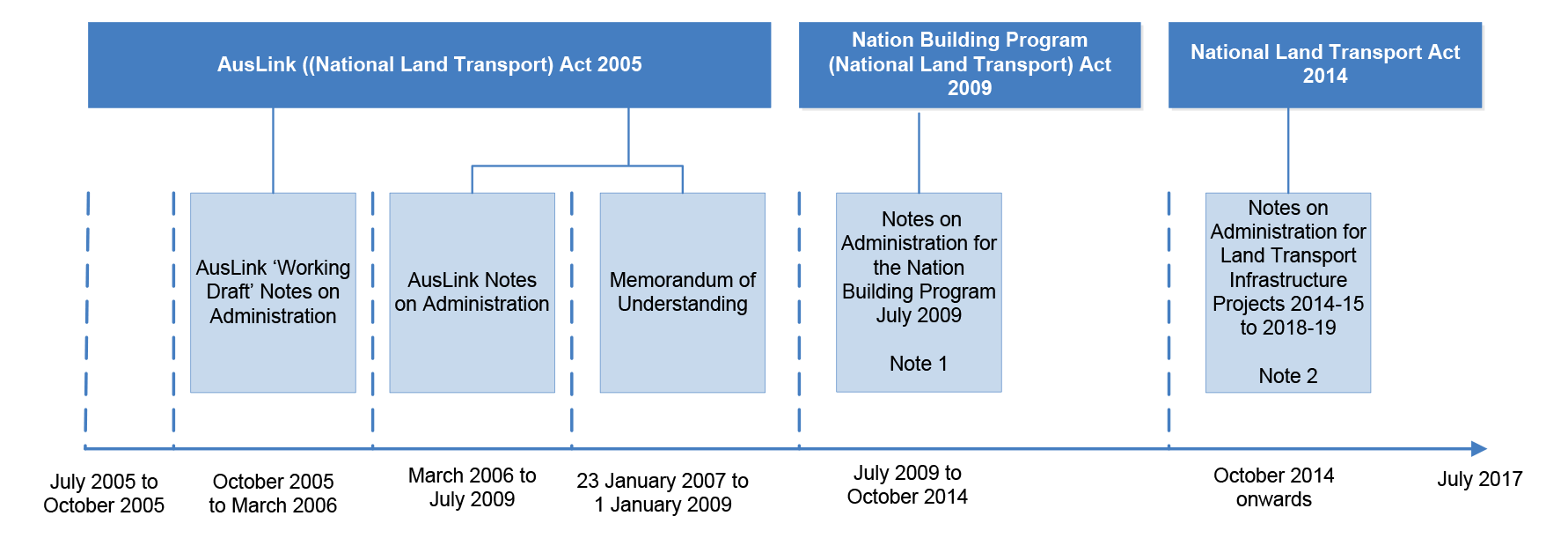

2.36 Legislative and administrative arrangements governing the provision of Australian Government grant funding for eligible infrastructure projects, including the pre-construction phase of the Inland Rail programme, are shown at Figure 2.4.

Figure 2.4: Legislative and administrative arrangements for the provision of Australian Government grant funding for eligible infrastructure projects

Note 1: For projects funded under Parts 3 and 6 of the Nation Building Program (National Land Transport) Act 2009 where payments are made directly to a State, an authority of a State, or any other body corporate.

Note 2: For projects funded, or proposed to be funded, under: Parts 3 or 7 of the National Land Transport Act 2014 (NLT Act); or Chapter 2 of the Nation-building Funds Act 2008. The Notes apply to all Proponents and Funding Recipients, where a Proponent may be a State, an authority of a State, a Local Government Authority; or any other body corporate that submits a proposal for Australian Government funding under the NLT Act. (The ARTC is a body corporate).

Source: ANAO analysis, updating information in ANAO Audit Report No.22 2007–08, Administration of Grants to the Australian Rail Track Corporation, p. 37, Figure 2.1.

2.37 The Notes on Administration for Land Transport Infrastructure Projects 2014–15 to 2018-19 (the Notes): are developed and maintained by Infrastructure; are publicly available on the Infrastructure website45; and provide guidance for funding applicants and the administrative processes that funding recipients must follow to claim payments, including to seek variations to project approvals. Specifically, Appendices C 1-4 of the Notes46 provide guidance on the level of detail and certainty required in a funding submission.

2.38 The Minister signed a Project Approval Instrument under Part 4 of the Nation Building Program (National Land Transport) Act 2009 to approve the project as a National Project and provide Commonwealth funding for the project to the ARTC as the funding recipient. Subsequent funds have been approved through variations to the project approval instrument.

Funding agreement

2.39 The funding arrangement for the pre-construction phase of the Inland Rail programme between Infrastructure and the ARTC was initially outlined in an exchange of letters between the ARTC and Infrastructure, in June 2014. In a letter of 13 June 2014 (approving funds for the programme), the Minister for Infrastructure and Regional Development stated that the ARTC ‘agree with my Department through a Memorandum of Understanding or a funding agreement the project milestones as well as the reporting arrangements’. On 29 January 2015, the Minister’s letter (approving further funding) notes that the Department ‘is still in discussion with the ARTC on a Memorandum of Understanding that covers reporting obligations of grant funding…I look forward to this Memorandum of Understanding being finalised’.

2.40 A paper prepared for the ARTC Internal Steering Committee, 15 April 2015, refers to the proposed funding Memorandum of Understanding (MoU) with the Australian Government, through Infrastructure:

While the Department’s focus is likely to be on the deliverables to be provided by ARTC, the MOU will also be the instrument to ensure that risk allocation and governance arrangements between ARTC and the Australian Government is properly addressed (in particular, that risks borne by ARTC are appropriately underwritten by the Australian Government).

2.41 A formal agreement between the ARTC and Infrastructure was finalised on 7 June 2017, some three years after the Minister’s first request to develop an agreement, and in the final year of the funding for the pre-construction phase. The agreement was in the form of a Deed of Agreement (the Deed) in relation to grant funding provided to the ARTC for projects approved under the National Land Transport Act 2014, valid until 30 June 2019.47 The Deed: does not provide details of project milestones and reporting arrangements (as per the Minister’s letters) referring to requirements set out in the NLT Act, the Notes and Instrument of Approval; and specifies (Clause 5.1.2) that there is no intent of retrospective application in relation to the existing projects ‘to the extent that funds have been approved in accordance with a Project Proposal Report prior to this Deed’.

2.42 Infrastructure advised on 7 July 2017, that:

There is no specific reason for the length of time the Deed took to negotiate. This funding arrangement is a binding agreement between the ARTC and the Commonwealth. It took some time to negotiate, longer than anticipated, in part due to both parties being aware of possible precedent for future construction funding.

The project (and risk) was being managed under the funding arrangements confirmed in an exchange of letters between the Department and the ARTC confirming the coverage of the funding through the Notes on Administration for the Infrastructure Investment Program.

The National Land Transport Act also provides the administrative requirements for associated projects, in particular sections in Parts 3 and 4 of the Act specify that conditions must be complied with including: reporting requirements; provision of information on request; and repayment of funds. The milestone approval arrangements required under the Notes on Administration also provided coverage from a number of perspectives including accountability and delivery of agreed outputs.

The Notes on Administration and Act manage risk and provide an accountability framework consistent with those in the Deed of Agreement.

2.43 In future, for similar grant funding arrangements, Infrastructure should more promptly comply with any request by the Minister to develop a Memorandum of Understanding or funding agreement.

Australian Government policies relating to Indigenous participation

2.44 The Deed includes that the recipient of funds (Clause 8.1) ‘must, unless otherwise agreed, develop and implement Indigenous workforce strategies as envisaged in the Council of Australian Governments Indigenous Reform Circular’. As at July 2017, there is no evidence of the ARTC having developed an Indigenous workforce strategy for the Inland Rail programme, noting however, that the requirement was only recently introduced through the Deed and is not retrospective.

2.45 The Australian Government’s Indigenous Procurement policy48 took effect from 1 July 2015. It requires Commonwealth entities to award a percentage of Commonwealth domestic contracts to Indigenous enterprises.49 As a GBE, the ARTC is not required to comply with this policy50, but is encouraged to do so. As at July 2017 the ARTC has the first draft of a policy, Inland Rail Programme Indigenous Procurement Policy, September 2016, with the purpose ‘to accompany Request for Tender Documents’. As at July 2017, the policy was still in draft form and there is no evidence in any of the 54 contracts reviewed by the ANAO (discussed in Chapter 3) of the consideration of Indigenous participation in procurement processes.

Process for grants funding of the pre-construction phase of the Inland Rail programme

2.46 To access grant funding for the pre-construction phase of the Inland Rail programme, the proponent (the ARTC) submits a project proposal report (PPR) to Infrastructure for a tranche of the total funds available ($300 million). The PPRs reflect specific bundles of work and set out milestone deliverables. Infrastructure assesses the PPRs and advises the Minister for Infrastructure and Transport who then decides whether funding should be approved. Infrastructure subsequently has responsibility for approving the milestone payments.

2.47 As at June 2017, the ARTC had submitted four PPRs (comprising 13 milestones) for the pre-construction phase of the Inland Rail programme. A review of the ARTC’s PPRs reflects that the company followed the relevant guidance for submissions under Part 3 of the NLT Act (although PPRs 1 and 2 were approved under Part 4 of the Act).

2.48 The PPRs and amounts approved and actually paid (as at July 2017), are set out in Table 2.3. The table shows minor adjustments for potential tax obligations and unspent risk contingency funding, and variations to the approved timeframe that resulted in differences between funds requested and approved. As at July 2017, the Minister has approved all the funds requested, and the ARTC has received some $160 million, or just over 53 per cent of the total amount of grant funding available.

Table 2.3: ARTC Project Proposal Reports and approved funding, as at July 2017

|

PPR submitted |

Requested ($million) |

Approved ($million) |

Approval legislation |

Cumulative approved ($million) |

Amount paid ($million) |

Payment date |

|

April 2014 PPR 1 (1–3) |

9.00 |

11.7a 12 June 2014 |

NLT Act Part 4, s.29 |

11.7 |

1.3 |

25 June 2014 |

|

4.4 |

27 Oct. 2014 |

|||||

|

3.3 |

22 Jan. 2015 |

|||||

|

24 Nov. 2014 Variation to PPR 1 |

3.2b |

3.2 29 Jan. 2015 |

NLT Act Part 4, s.29 |

12.2c |

|

|

|

11 Dec. 2014 PPR 2 ( 4–5) |

29.0 |

29.0 29 Jan. 2015 |

NLT Act Part 4, s.29 |

41.2 |

21.9 |

28 April 2015 |

|

4.4 |

22 Nov. 2015 |

|||||

|

21 Aug. 2015 PPR 3 (6–11) |

235.4 |

100.7 1 Oct. 2015 |

NLT Act Part 3, s.9 |

141.9 |

24.7 |

22 Dec. 2015 |

|

26.8 |

23 May 2016 |

|||||

|

7.3 |

28 Sep. 2016 |

|||||

|

11.8 |

22 Dec. 2016 |

|||||

|

31.1 |

23 Jan. 2017 |

|||||

|

18 Nov. 2016 PPR 4 (9–13) |

147.9d |

143.1e 20 Dec. 2016 |

NLT Act Part 3, s.9 |

285.0 |

22.9 |

22 June 2017 |

|

Total PPRs |

424.5f |

287.7 |

|

285.0g |

159.9 |

|

Note a: The Minister approved an additional $2.7 million for company tax obligations (taking the total to $11.7 million) to be released ‘only when ARTC demonstrates liability for tax associated with the Inland Rail project funding’.

Note b: The ARTC advised the Minister that the variation to PPR 1 was necessary to account for a number of under and overspends in relation to the original PPR 1 budget, as well as significant additional scope not envisaged at the time of the original submission.

Note c: The variation to the Project Instrument did not include the $2.7 million allowance for tax obligations approved as part of PPR1.

Note d: As the Minister approved the full scope of work proposed in PPR3 (for delivery by September 2017), but only sufficient funding for activities to 30 June 2016, the PPR 4 submission included a revised work programme for pre-construction activity to be delivered by November 2018 and an additional $12 million.

Note e: The PPR 4 submission included a total Risk Contingency of $10.1 million, which included $4.8 million brought forward from the unused PPR 3 Risk Contingency. The amount approved was adjusted accordingly.

Note f: Totals the amounts submitted by the ARTC, but does not allow for the partial funding of PPR3.

Note g: The discrepancy of $2.7m with the approved total is accounted for by the exclusion from subsequent variations to the Project Instrument of an allowance for tax obligations as detailed at Notes 1 and 3 above.

Source: ANAO from ARTC and Infrastructure documentation.

2.49 The document control sheets attached to each of the ARTC’s PPRs should set out the internal responsibilities for preparing, approving and endorsing the submissions. As shown in Table 2.4, the document control sheets did not provide full details in three of the four PPRs.

Table 2.4: Information provided on ARTC’s document control sheets for each PPR

|

PPR |

Prepared |

Approved |

Date approved |

Endorsed |

|

PPRs 1 and 2 |

No document control informationa |

|||

|

PPR3 |

Government Commercial Relations Manager – Inland Rail |

Executive General Manager, Interstate Network |

21 August 2015 |

Internal Inland Rail Steering Committeeb |

|

PPR4 |

Government Commercial Relations Manager – Inland Rail |

Inland Rail Programme Director |

blank |

blank |

Note a: The ARTC advised that PPRs 1 and 2 were approved by the ARTC Chief Executive Officer; and PPR 4 was considered by the ARTC’s Internal Steering Group on 27 October 2016 and approved on 18 November 2016.

Note b: Evidenced in the documentation provided by the ARTC (refer paragraph 2.14).

Source: ANAO, from the ARTC’s PPR submissions, and ARTC.

2.50 Guidance for Infrastructure’s assessment of the PPRs is provided in the department’s:

- Practice Direction, Milestones (November 2014): provides project officers with guidance on the establishment and management of Milestones; and

- Project Proposal Report Assessment Guide (developed December 2015, and implemented the following year for assessment of PPR 4): in the form of a template that provides a record of a project officer’s assessment, and follows Appendix C to the Notes. It provides a comprehensive checklist of the consideration of requirements for Land Transport Infrastructure projects.

Submission and assessment of the Project Proposal Reports

2.51 PPRs 1 and 2 are relatively simple submissions and assessments, relating to the development of discrete plans and strategies, and account for the $41.2 million referred to in the Inland Rail Implementation Group, Report to the Australian Government, 24 August 2015. Infrastructure assessed the PPRs under Part 451 of the Nation Building Program (National Land Transport) Act 2009 and the National Land Transport Act 2014 respectively, and (for PPR1) the Financial Management and Accountability Regulations 1997.

2.52 The assessment for PPR 1 includes that the Department ‘considers the proposed expenditure is in accordance with FMA Regulation 952 [and] that the PPR provides sufficient detail for the scope of works and that on the available evidence, the project provides value for money’. There is no reference to value for money in the PPR 2 assessment. The assessments by Infrastructure refer to supporting documentation provided by ARTC as part of the PPR submissions, but no analysis of these documents supporting Infrastructure’s assessment was referenced.

2.53 The ARTC’s PPR 3 is a more complex submission for a range of activities to be funded under the total remaining funds ($235 million to September 2017), recommending one of the four options set out in the submission that, in the ARTC’s view, represents the ‘best value for money’ as ‘multiple development activities can be procured and staged along the entire rail alignment’.

2.54 Infrastructure’s engagement with the ARTC in the preparation of PPR 3, formal assessment of the submission and advice to the Minister reflect two key considerations regarding the funding of the Inland Rail programme: would the government progress the full programme; and would the ARTC be the delivery body. The advice to the Minister includes: ‘The decision to fund this PPR should ideally be made after Government has made a decision to fully fund the programme over 10 years, and determined the delivery model’.