Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 28 of 2007–08

Defence's Compliance with the Public Works Committee Approval Processes

Published

Tuesday 22 April 2008

Portfolio

Defence

Entity

Department of Defence

Sector

Defence

The objective of the audit was to review selected Defence public works projects submitted in the three year period ending mid 2007 to assess whether they had been submitted in accordance with the Committee's prevailing requirements for notification and review prior to entering into financial commitments for public works. The audit also examined the procedures applied by Defence to refer public works projects to the Committee, and identified administrative practices that may improve adherence with relevant legislative and administrative referral requirements.

Summary

Introduction

Under the Public Works Committee Act (1969) (the Act), any public work1 estimated to cost $15 million or more must be referred to the Parliamentary Standing Committee on Public Works (the Committee).2 In early 2007, the Joint Committee of Public Accounts and Audit (JCPAA) advised the Australian National Audit Office (ANAO) that a priority3 of Parliament was for the ANAO to conduct a performance audit of the processes associated with the development of public works proposals by agencies that fall within the scope of the Committee. Against this background, the ANAO decided to undertake two related audits on this issue.

This first audit examines whether the Department of Defence's (Defence's) capital works projects have been submitted in accordance with the Committee's requirements for notification and review prior to entering into financial commitments for the works. A second audit, which is currently underway, will assess the planning and delivery of selected capital works projects, the extent to which these projects have delivered in accordance with expectations, and the extent to which relevant sponsoring agencies have complied with the requirements of the Act and approval procedures.

Administrative processes

The Department of Finance and Deregulation (Finance) administers the Act, and is responsible for working with agencies to ensure that any work estimated to cost $15 million or more is referred to the Committee. The Act provides the Committee with powers to examine and report on:

- the purpose and suitability of the work for the purpose;

- the need to carry out the work;

- cost effectiveness;

- the amount of revenue that may be expected4; and

- the present and prospective public value of the work.

Submissions to the Committee are prepared by the agency which is carrying out or contracting out the work. The submission includes information on why the work is necessary, other options that were considered, the estimated cost and any plans or drawings that will help the Committee understand the purpose and scope of the work. The Act provides that a public work, for which the estimated cost exceeds the threshold amount requiring referral to the Committee, may not be commenced unless either such a referral has occurred or certain specific conditions are met5.

Defence has a large ongoing investment program and so many of its projects are required under the Act to be referred to the Committee. The total value of projects referred to the Committee over the period from mid 2004 to mid 2007 was $5.29 billion. Defence was selected for audit because Defence projects comprised $4.30 billion, or 81 per cent of the total value of projects referred to the Committee over the period6.

Defence uses two methods for financing projects. Most commonly, direct procurement is used. This involves a standard set of contracts to pay for the required work at the time of construction. Less common are Public Private Partnerships (PPPs), whereby Defence enters into a long term agreement to pay an annual service payment, which covers the cost of construction work and whole of life maintenance and service provision.

The policy and processes Defence has in place to provide guidance to staff managing projects is quite different depending on which of these two financing methods is being used. There is much more support material available to staff managing projects using the direct procurement method, as this is the most common way of managing a public works project. The PPP method is still being developed, and, as a consequence, supporting material is also being developed7.

Audit objective and scope

The objective of the audit was to review selected Defence public works projects submitted in the three year period ending mid 2007 to assess whether they had been submitted in accordance with the Committee's prevailing requirements for notification and review prior to entering into financial commitments for public works. The audit also examined the procedures applied by Defence to refer public works projects to the Committee, and identified administrative practices that may improve adherence with relevant legislative and administrative referral requirements.

The scope of the audit did not include an examination of the extent to which the projects in the ANAO's sample have delivered in accordance with expectations. The ANAO currently has a second audit underway that will assess the planning and delivery of a sample of capital works projects (including two Defence projects), the extent to which the selected projects have met expectations, and the extent to which relevant sponsoring agencies have complied with the requirements of the Act and approval procedures.

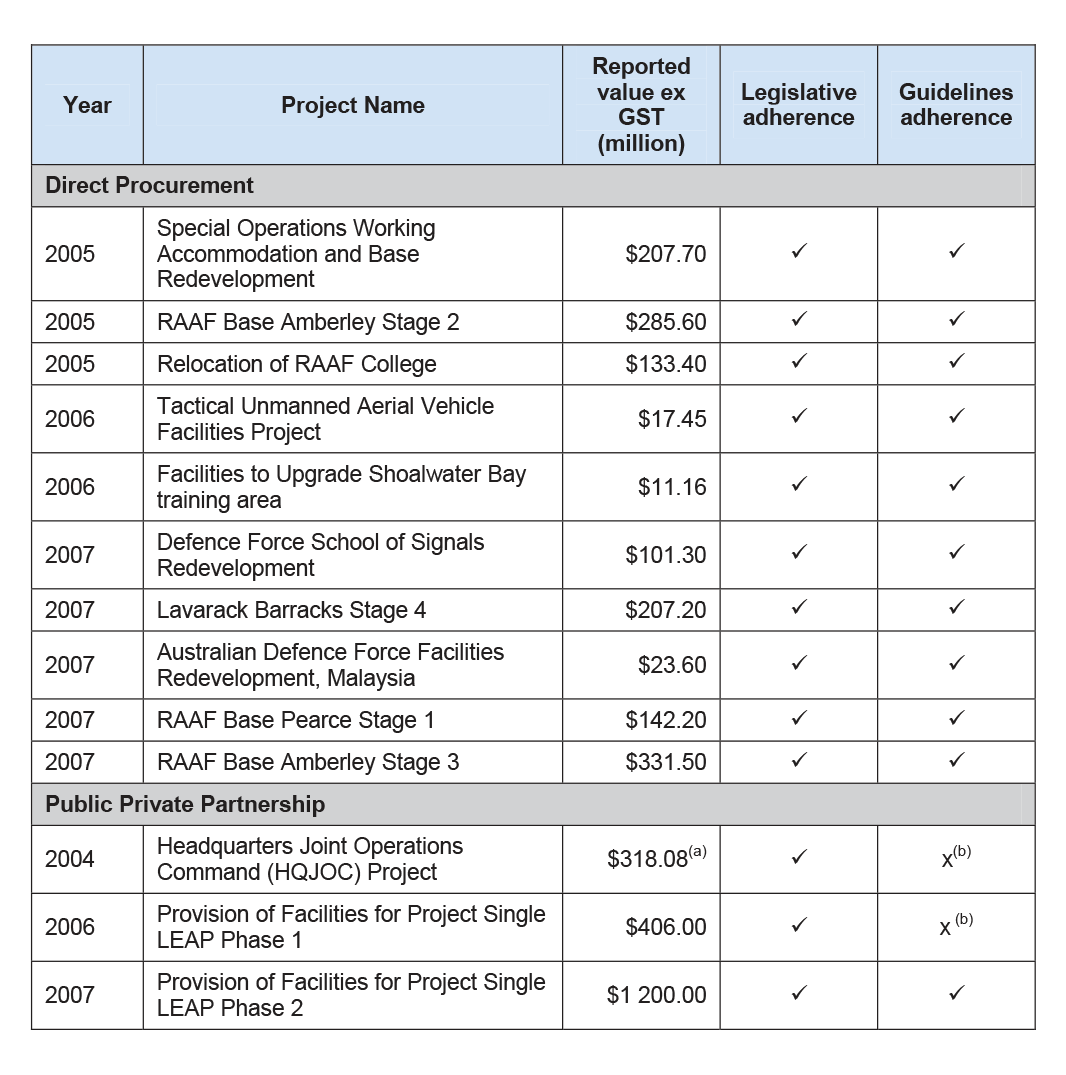

In order to assess Defence's adherence to the Committee's requirements, 13 projects were reviewed in detail during fieldwork, having regard to adherence to both the requirements of the Public Works Committee Act 1969 (the Act) and the Committee's Manual of Administrative Procedures (the Committee's Manual). The 13 projects selected represent 78 per cent of the total estimated cost of the 22 Defence projects referred to the Committee from mid 2004 to mid 2007. They are a cross section of projects, from the very large and complicated (for example, provision of facilities for the Single Living Environment and Accommodation Precinct (LEAP) Project), to the relatively straightforward (for example, the facilities upgrade to the Shoalwater Bay Training Area). The sample of projects include 10 that were financed through direct procurement, and three that are to be financed using Public Private Partnerships (PPPs).

Conclusion

Defence complies with the requirements of the Public Works Committee Act 1969, and largely complies with the requirements of the Committee's Manual, in referring projects to the Committee for notification and review prior to entering into financial commitments for the relevant public works. The ANAO found that Defence had referred all 13 of the building works projects examined in the audit to the Committee for Parliamentary approval before the department committed money to construction. In addition, all 13 projects demonstrated adherence to the legislative requirements, and 11 of the 13 selected projects demonstrated adherence to the Committee's administrative guidelines. The non-adherence to the guidelines for two projects relates to the requirement to advise the Committee of any significant changes to design, scope and related matters.

Defence's ability to manage building works projects successfully is influenced by relatively stable staffing, leading to corporate knowledge being retained, and a mechanism for maintaining in one easy to navigate system, key project management information. Defence has clear and accessible guidelines that reflect the Committee's requirements for the projects the department manages using direct procurement. However, Defence does not currently have available equally comprehensive policy and procedural information to guide project officers in developing and delivering PPP projects. The guidance Defence does have available to project officers undertaking PPPs is not maintained on the Infrastructure Management System and does not include information on the Public Works Committee processes, either before or after Parliamentary approval.

The ANAO considers there are opportunities for improvements to help Defence prepare for, and follow up on, Committee requirements. These include the use of standard templates when preparing documents for the Committee, more clearly specifying the costs of the project (particularly the inclusion or exclusion of Goods and Services Tax amounts) and in reporting back to the Committee on recommendations made in the Committee's reports.

Recommendation

The ANAO made one recommendation that Defence develop and document processes to report back to the Public Works Committee on recommendations made in the Committee's reports to Parliament where feedback has been requested.

Agency responses

Defence provided the following response to the audit:

The audit has confirmed that Defence complies with the requirements of the Public Works Act. To that end Defence notes that its two pass project development and approval processes, implemented in 2004, provide transparency, accountability and cost certainty for major capital facilities submissions to Government. This process also enables Defence to provide high quality information to the Public Works Committee during its enquiries.

Finance advised that the department supported the one recommendation made in the audit report.

Table 1 Project Legislative and guidelines adherence

Footnotes

1 A public work is defined as a work proposed to be done by the Commonwealth, or on behalf of the Commonwealth, and it includes construction, alteration, repair or destruction of buildings and other structures.

2 The Parliamentary Standing Committee on Public Works is also known as the Public Works Committee or the PWC.

3 Each year, the JCPAA consults with all other Committees of the Australian Parliament to identify the priorities of the Parliament for performance audits to be undertaken in the following financial year by the ANAO.

4 Revenue might be produced from building works like a toll bridge or a building that can be leased out to private companies.

5 Sub-section (8) of section 18 of the Act provides that:

A public work the estimated cost of which exceeds the threshold amount shall not be commenced unless:

(a) the work has been referred to the Committee in accordance with this section;

(b) the House of Representatives has resolved that, by reason of the urgent nature of the of the work, it is expedient that it be carried out without having been referred to the Committee;

(c) the Governor-General has, by order, declared that the work is for defence purposes and that the reference of the work to the Committee would be contrary to the public interest; or

(d) the work is a work that has been declared, by a notice under subsection (8A), to be a repetitive work for the purposes of this subsection.

6 Defence manages $11.9 billion of land and building assets and spent $578 million on capital projects in 2006–07.

7 The most comprehensive information available on PPPs at the Commonwealth level are the Department of Finance and Deregulation's Financial Management Guidance No.s 16 to 19, covering an introductory guide, business case development, risk management and contract management.