Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 30 of 2023–24

Corporate Planning in the Department of Climate Change, Energy, the Environment and Water

Published

Tuesday 28 May 2024

Portfolio

Climate Change, Energy, the Environment and Water

Entity

Department of Climate Change, Energy, the Environment and Water

Contact

Please direct enquiries through our contact page.

Activity

Governance

Sector

Environment

Audit snapshot

Why did we do this audit?

- The Public Governance, Performance and Accountability Act 2013 establishes a structure for entities to plan, measure, evaluate and report performance. This includes a uniform requirement for entities to prepare a corporate plan to promote rigorous and transparent resource management planning and improve performance across the Commonwealth.

- A Commonwealth entity’s corporate plan is its primary planning document. The corporate plan, Portfolio Budget Statements, and annual report should allow a clear line of sight between planned and actual performance.

Key facts

- In July 2022, the Department of Climate Change, Energy, the Environment and Water (DCCEEW) was established, combining functions previously held by four other entities.

- DCCEEW leads Australia’s response to climate change, sustainable energy use, and environmental protection.

- DCCEEW’s first corporate plan was an opportunity for the department to set out its purposes and key activities, the outcomes it hopes to achieve and how achievement against the purposes would be measured.

What did we find?

- DCCEEW has largely established its corporate plan as its primary planning document.

- DCCEEW has developed its corporate plan in line with the Commonwealth Performance Framework.

- DCCEEW is partly effective in implementing its corporate plan.

- DCCEEW has a largely effective assurance framework to support reporting against the corporate plan outcomes.

What did we recommend?

- There was one recommendation made to DCCEEW relating to management of enterprise risks.

- DCCEEW agreed to the recommendation.

8

key activities in DCCEEW’s 2023–24 Corporate Plan

21

performance measures in DCCEEW’s 2023–24 Corporate Plan

2

corporate plans since DCCEEW was established in July 2022

Summary and recommendations

Background

1. The Commonwealth Performance Framework is established under the Public Governance, Performance and Accountability Act 2013 (PGPA Act) to provide a line of sight between the use of public resources by Commonwealth entities and the outcomes achieved.1

2. Australian Government entities must meet high standards of governance, performance, and accountability. Under the Commonwealth Performance Framework, entities must prepare a corporate plan as the entity’s primary planning document. The corporate plan and the Portfolio Budget Statements describe the entity’s planned performance. The performance statements provide information on the entity’s actual performance in achieving its purposes in the reporting period. Performance statements are included in the entity’s annual report which is tabled in the Parliament. These three documents work together to provide a clear line of sight between planned and actual performance.2

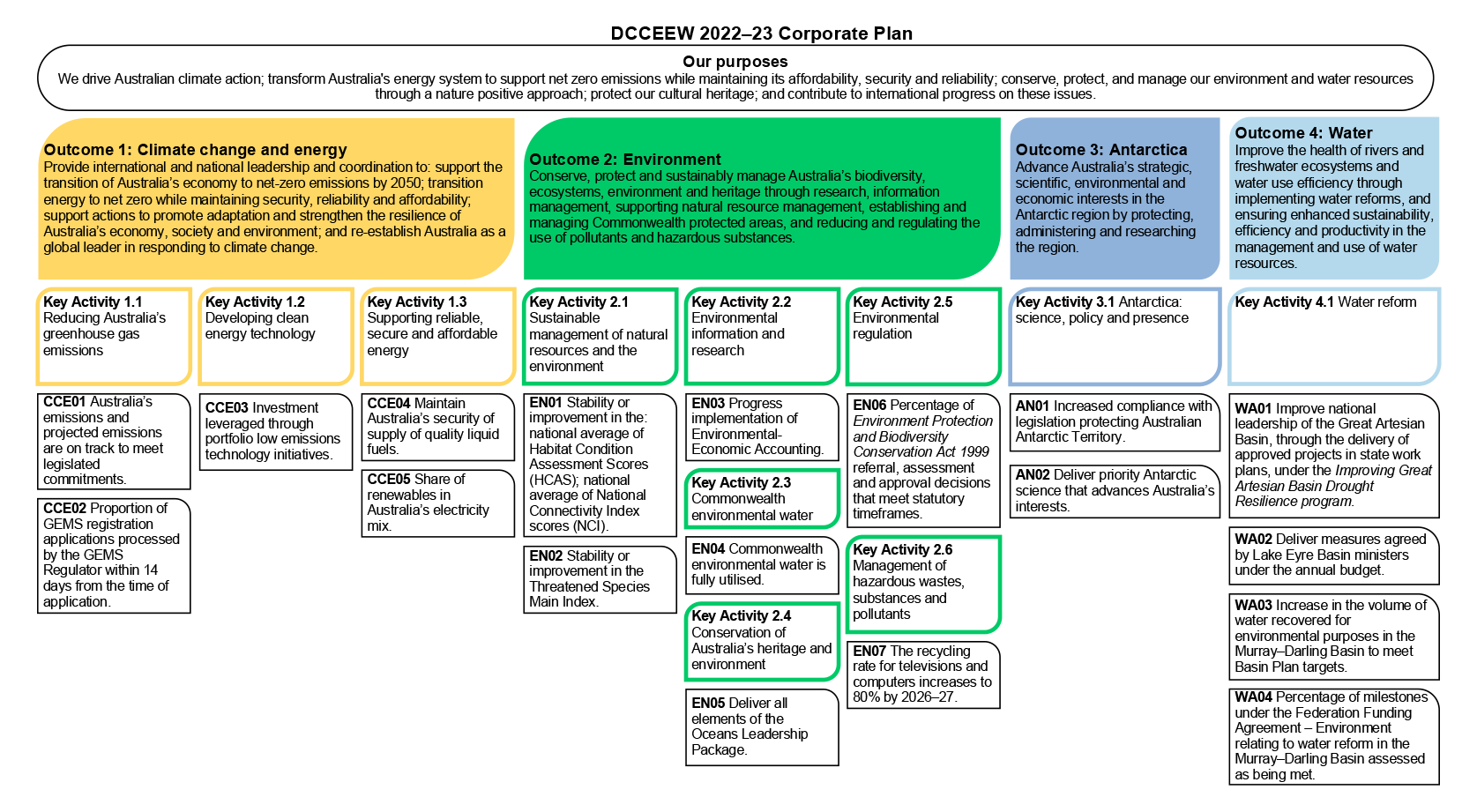

3. The Department of Climate Change, Energy, the Environment and Water (DCCEEW) was established on 1 July 2022, combining functions previously held by four different entities. DCCEEW published its first corporate plan — for 2022–23 — in March 2023. The 2023–24 corporate plan was published in August 2023.3

Rationale for undertaking the audit

4. The Commonwealth Performance Framework, established under the PGPA Act, requires Commonwealth entities to annually publish a corporate plan that details how they intend to achieve their purposes and how their performance will be measured and assessed. Commonwealth entities must report on their performance in annual performance statements tabled in the Parliament.

5. DCCEEW is a new entity combining functions from four different entities following a machinery of government change in July 2022. This audit will provide independent assurance to the Parliament that DCCEEW’s corporate planning meets the requirements and intent of the Commonwealth Performance Framework in operating as its primary planning document.

Audit objective and criteria

6. The objective of this audit was to assess the effectiveness of DCCEEW’s corporate plan as its primary planning document in accordance with the PGPA Act. To form a conclusion against the objective, the following criteria were adopted.

- Has DCCEEW developed its corporate plan in line with the Commonwealth Performance Framework?

- Is DCCEEW effectively implementing its corporate plan?

- Does DCCEEW have an effective assurance framework to support reporting against the corporate plan outcomes?

Conclusion

7. DCCEEW has largely established the corporate plan as its primary planning document in accordance with the Public Governance, Performance and Accountability Act 2013. The corporate plan meets legislative requirements. Priorities identified in the corporate plan are not yet reflected through a mature divisional planning process. The management of enterprise risks can be strengthened by assessing the risks against departmental risk appetite and tolerances. DCCEEW developed an enterprise performance framework to support the continual improvement of performance information.

8. DCCEEW has developed its corporate plan in line with the Commonwealth Performance Framework. The department established governance arrangements that supported the development and implementation of the 2022–23 and 2023–24 corporate plans. The corporate plans meet the mandatory requirements of the Public Governance, Performance and Accountability Act 2013 as both corporate plans were published in accordance with publication requirements and include mandatory content. DCCEEW has presented information clearly to provide a line of sight within the performance cycle and across performance cycles.

9. DCCEEW is partly effective in implementing its corporate plan. The corporate plan has not yet been fully integrated into the department’s planning and reporting frameworks. DCCEEW has established appropriate governance structures to provide oversight over corporate plan implementation. In March 2023, DCCEEW developed an Enterprise Risk Management Framework (ERMF) and identified eight enterprise risks. Committees are not providing effective oversight over all enterprise risks and the enterprise risks are not being managed in accordance with the ERMF. The nature of committee reporting to the Executive Board limits the Board’s ability to have assurance over enterprise risk management. DCCEEW developed an Enterprise Performance Framework to support regular reporting against the performance measures listed in the corporate plan.

10. DCCEEW has a largely effective assurance framework to support reporting. Processes to support reporting include the development and certification of measure profiles for each performance measure, and certification of the accuracy of performance information by measure owners and deputy secretaries. The detail within the measure profiles regarding the responsibility for collating performance information differs. DCCEEW developed an Enterprise Performance Framework intended to provide annual risk-based reviews of performance measures.

Supporting findings

Development

11. DCCEEW established governance arrangements and processes to support the development of both the 2022–23 and 2023–24 corporate plans. Implementation plans were used to support the drafting and approval processes for both corporate plans. To support performance measurement and reporting, the department developed ‘profiles’ of each measure, with certification by division heads and deputy secretaries that the measures complied with the PGPA Act. (See paragraphs 2.3 to 2.29)

12. The 2022–23 and 2023–24 corporate plans were provided to relevant ministers and published in accordance with required timeframes. The corporate plans meet the mandatory content requirements of the Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) and place DCCEEW in a good position to provide meaningful and accurate performance information to the Parliament. DCCEEW has identified a mix of quantitative, qualitative, output and effectiveness measures across all outcomes. DCCEEW has not identified efficiency measures. (See paragraphs 2.30 to 2.49)

13. DCCEEW has provided a clear read across relevant Portfolio Budget Statements (PBS) and corporate plans from 2022–23 to 2023–24. Changes in performance information have been communicated to allow users and the Parliament to track the changes between the documents and across performance cycles. (See paragraphs 2.50 to 2.64)

Implementation

14. DCCEEW used the 2022–23 Corporate Plan to develop and embed purposes for the new department. The 2022–23 Corporate Plan published in March 2023 was intended to inform DCCEEW’s business and divisional planning. The first stage of this divisional planning occurred in October 2023. The corporate plan identified nine areas of capability development to support DCCEEW’s delivery of key activities. Five are being implemented. The priority focus areas for information technology (IT) that were identified in both corporate plans have not been reflected in enterprise-wide IT and digital transformation strategies and plans. (See paragraphs 3.3 to 3.20)

15. DCCEEW established five committees with roles related to the enterprise-wide monitoring of programs and performance. Each committee has a forward workplan that includes monitoring of plans and strategies in the corporate plan. In November 2023, DCCEEW commenced the development of an approach to regular reporting against performance measures through the Enterprise Performance Framework. (See paragraphs 3.21 to 3.30)

16. The 2022–23 and 2023–24 corporate plans identify eight enterprise risks and provide a narrative of how each risk will be managed. In February 2023, DCCEEW assigned governance committees with responsibility for the management of specific enterprise risks. The enterprise risks have not been assessed against departmental risk tolerances and the effectiveness of controls in managing the risks have not been assessed, in accordance with the ERMF. Committees discussed and considered control actions for four of the eight enterprise risks. The nature of committee reporting to the Executive Board limits the ability of the Board to have effective oversight of enterprise risk management. (See paragraphs 3.31 to 3.49)

Assurance

17. DCCEEW drafted an implementation plan for the development of the 2022–23 Annual Report, including a governance structure for the clearance of information in the report and a risk assessment. DCCEEW developed measure profiles to document the data and reporting arrangements for the performance measures. The measure profiles also document roles and responsibilities, data limitations and data validation. There is a risk the measure profiles do not provide the accountable authority with a consistent level of assurance that the performance information will be complete and accurate. (See paragraphs 4.2 to 4.19)

18. Division heads and deputy secretaries are required to provide assurance over reporting information against the performance measures. DCCEEW developed templates to guide certification of performance information for the 2022–23 Performance Statements and all certifications were provided. DCCEEW has recognised the need to continue to improve the performance measures through an Enterprise Performance Framework supported by the internal audit program. (See paragraphs 4.20 to 4.37)

Recommendations

Recommendation no. 1

Paragraph 3.47

The Department of Climate Change, Energy, the Environment and Water manage enterprise risks in accordance with the department’s Enterprise Risk Management Framework, including assessing enterprise risks against departmental risk appetite and tolerances, and assessing the effectiveness of controls.

Department of Climate Change, Energy, the Environment and Water response: Agreed.

Summary of entity response

The Department of Climate Change, Energy, the Environment and Water (the department) is committed to the establishment of compliant, sound, and best practice governance arrangements to support delivery of its large and complex agenda. The department agrees to the one recommendation regarding improvements to the management and oversight of enterprise risks in the context of implementation of our Corporate Plan.

Following its establishment in July 2022, the department published its first corporate plan in March 2023, following extensive consultation with all staff to establish our Vision and Purposes supported by our Key Activities. Our next Corporate Plan, published in August 2023, further matured our performance information.

In March 2023, the department implemented an Enterprise Risk Management Framework to support a fit-for-purpose approach to the identification and management of risks suited to its diverse operating context. We continue to mature our positive risk culture through our governance arrangements and supporting resources.

The department welcomes the ANAO’s recommendation and observations to support our improvement of corporate planning practices ahead of our next Corporate Plan in August 2024.

Key messages from this audit for all Australian Government entities

19. Below is a summary of key messages, including instances of good practice, which have been identified in this audit and may be relevant for the operations of other Australian Government entities.

Group title

Governance and risk management

Key learning reference

1. Background

Commonwealth Performance Framework

1.1 The Public Governance, Performance and Accountability Act 2013 (PGPA Act) establishes a performance framework across Australian Government entities and requires Australian Government entities to meet high standards of governance, performance and accountability.4 The Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) establishes requirements to give effect to matters covered by the Act.5

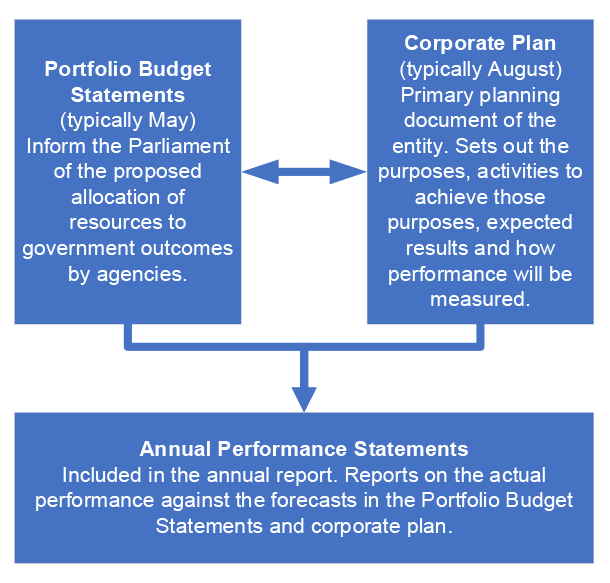

1.2 The Department of Finance defines how components of the PGPA Act and PGPA Rule combine in the Commonwealth Performance Framework to allow a clear line of sight between planned and actual performance.6 The Commonwealth Performance Framework consists of an entity’s Portfolio Budget Statements, corporate plan, and annual performance statements7 as illustrated in Figure 1.1.

Figure 1.1: Commonwealth Performance Framework

Source: Department of Finance, Corporate Plans for Commonwealth Entities (Resource Management Guide 132), ‘What is a corporate plan?’, available from https://www.finance.gov.au/government/managing-commonwealth-resources/corporate-plans-commonwealth-entities-rmg-132/what-corporate-plan [accessed 10 May 2024].

1.3 The Commonwealth Performance Framework establishes an entity’s corporate plan as its primary planning document including by requiring:

- performance planning and reporting to draw clear links between the entity’s key activities and the results achieved; and

- performance reporting to provide meaningful performance information.8

Department of Climate Change, Energy, the Environment and Water

1.4 The Department of Climate Change, Energy, the Environment and Water (DCCEEW) was established on 1 July 2022. DCCEEW is responsible for:

- climate change and energy functions previously held by the Department of Industry, Science, Energy and Resources;

- environment and water functions previously held by the Department of Agriculture, Water and the Environment;

- international climate change functions previously held by the Department of Foreign Affairs and Trade; and

- water infrastructure functions and the National Water Grid Authority previously held by the Department of Infrastructure, Transport, Regional Development and Communications.

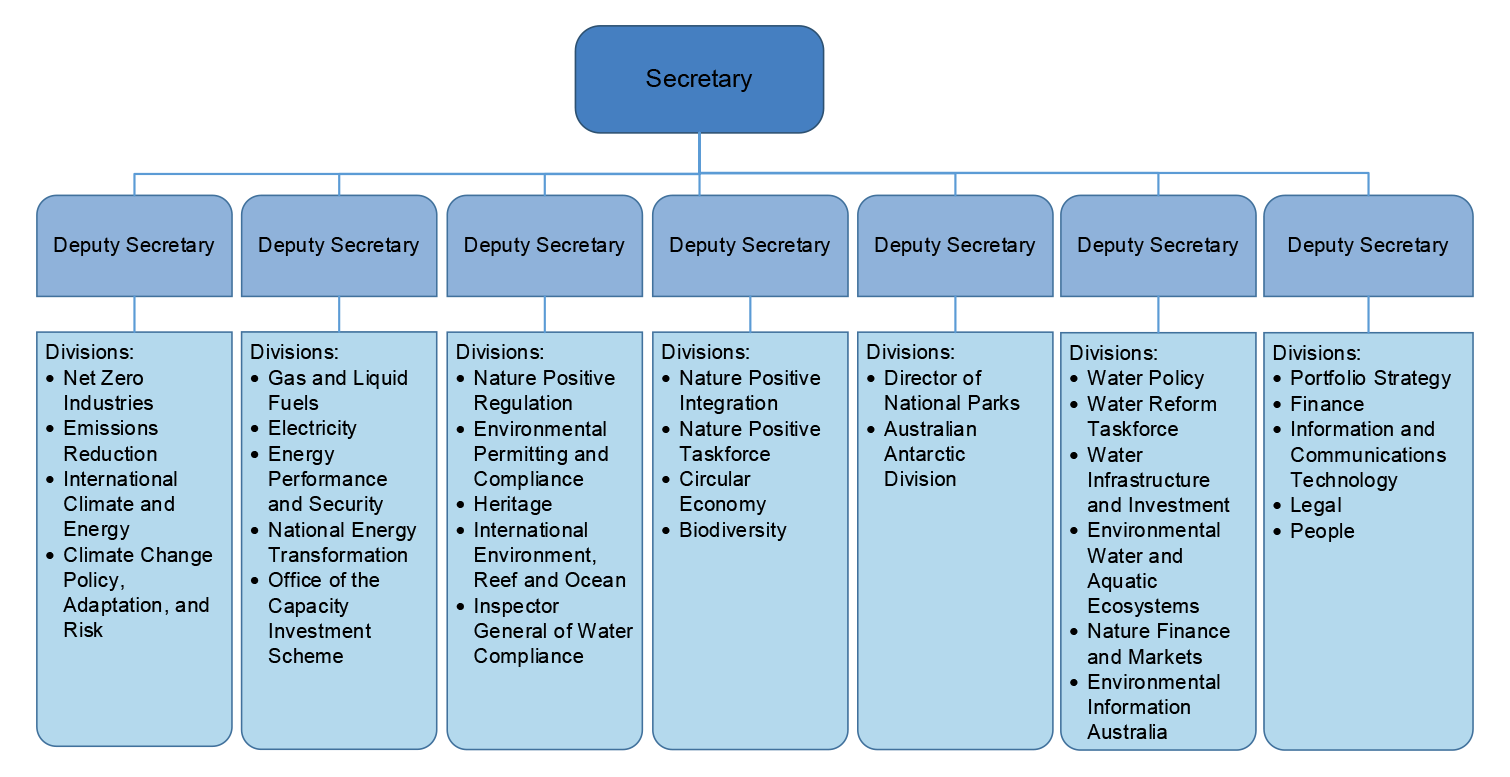

1.5 DCCEEW comprises seven groups, each led by a deputy secretary. The structure of DCCEEW as of March 2024 is depicted in Figure 1.2.

Figure 1.2: Structure of DCCEEW

Source: DCCEEW organisational chart March 2024.

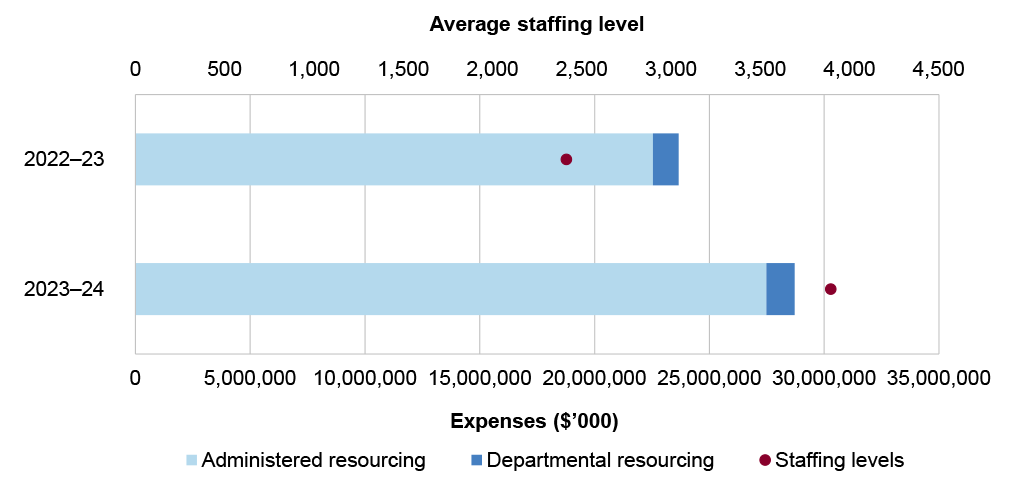

1.6 As illustrated in Figure 1.3, DCCEEW’s staffing level rose by 61 per cent from 2,414 staff in 2022–23 to 3,895 in 2023–24. DCCEEW’s budgeted resourcing grew by 21 per cent from 2022–23 to 2023–24. DCCEEW’s total estimated budget in 2023–24 was $28.7 billion.

Figure 1.3: DCCEEW resourcing and staffing level

Source: DCCEEW, Annual Report 2022–23, Commonwealth of Australia, Canberra, 2023, available from https://www.dcceew.gov.au/about/reporting/annual-report [accessed 27 March 2024].

Australian Government, Portfolio Budget Statements 2023–24, Budget Related Paper No. 1.3. Climate Change, Energy, the Environment and Water Portfolio, Commonwealth of Australia, Canberra, 2023, available from https://www.dcceew.gov.au/sites/default/files/documents/dcceew-2023-24-pbs.pdf [accessed 14 February 2024].

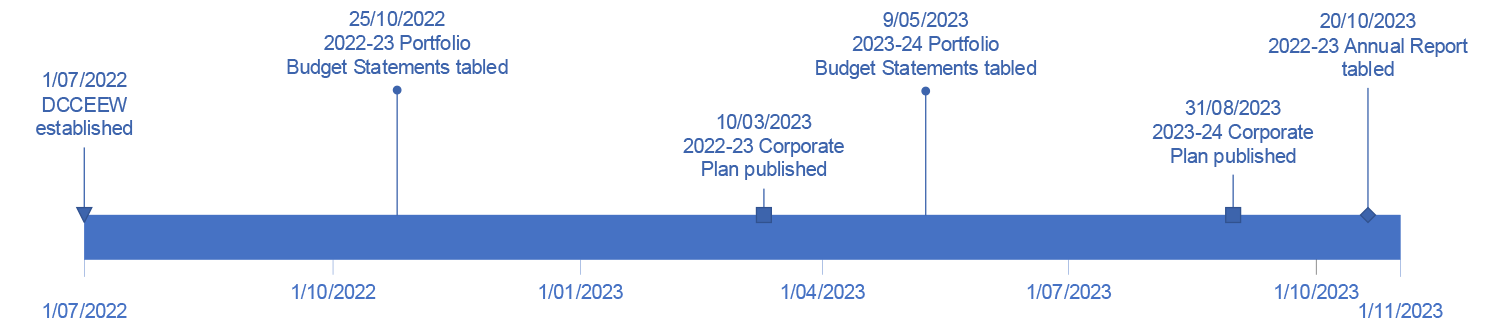

1.7 DCCEEW published its first corporate plan — for 2022–23 — in March 2023. The 2023–24 Corporate Plan was published in August 2023.9 Figure 1.4 illustrates the release of the two corporate plans and other performance framework documents since the establishment of the entity. DCCEEW’s first annual report was tabled in the Parliament on 20 October 2023.10

Figure 1.4: DCCEEW’s performance framework documents

Source: ANAO analysis of departmental documentation.

Rationale for undertaking the audit

1.8 The Commonwealth Performance Framework, established by the PGPA Act, requires Commonwealth entities to annually publish a corporate plan that sets out how they intend to achieve their purposes, and how their performance will be measured and assessed. Commonwealth entities must report on their performance in annual performance statements that are included in an entity’s annual report that is tabled in the Parliament.

1.9 DCCEEW is a new entity combining functions from four different entities following a machinery of government change in July 2022. This audit will provide independent assurance to the Parliament that DCCEEW’s corporate planning meets the requirements and intent of the Commonwealth Performance Framework in operating as its primary planning document.

Audit approach

Audit objective, criteria and scope

1.10 The objective of this audit was to assess the effectiveness of DCCEEW’s corporate plan as its primary planning document in accordance with the PGPA Act.

1.11 To form a conclusion against the objective, the following criteria were adopted.

- Has DCCEEW developed its corporate plan in line with the Commonwealth Performance Framework?

- Is DCCEEW effectively implementing its corporate plan?

- Does DCCEEW have an effective assurance framework to support reporting against the corporate plan outcomes?

Audit methodology

1.12 The audit methodology involved examining departmental documentation, including meeting papers of governance groups, and meeting with relevant departmental staff.

1.13 The ANAO also received one submission from the public via the citizen contribution facility on the ANAO website.

1.14 The audit was conducted in accordance with ANAO Auditing Standards at a cost to the ANAO of approximately $364,785.

1.15 The team members for this audit were Johanna Bradley, Emma Hussey, Mary Potter, Ashlee Johnson, and Corinne Horton.

2. Development

Areas examined

This chapter examines whether the Department of Climate Change, Energy, the Environment and Water (DCCEEW) developed its corporate plan in line with the Commonwealth Performance Framework.

Conclusion

DCCEEW has developed its corporate plan in line with the Commonwealth Performance Framework. The department established governance arrangements that supported the development and implementation of the 2022–23 and 2023–24 corporate plans. The corporate plans meet the mandatory requirements of the Public Governance, Performance and Accountability Act 2013 as both corporate plans were published in accordance with publication requirements and include mandatory content. DCCEEW has presented information clearly to provide a line of sight within the performance cycle and across performance cycles.

2.1 The Public Governance, Performance and Accountability Act 2013 (PGPA Act) and Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) establishes an entity’s corporate plan as its primary planning document and determines mandatory corporate plan content. The Commonwealth Performance Framework promotes a high standard of planning, measuring, evaluating and reporting on Commonwealth entity performance and provides for consistency across planning and reporting on performance.11 The accountable authority is responsible for preparing a corporate plan and measuring and assessing the performance of the entity in achieving its purposes, in accordance with the PGPA Act.12

2.2 Strategic and concerted leadership over the performance cycle within an entity is essential to good management and the effective stewardship of public resources.13 Effective governance will support the accountable authority to ensure the corporate plan is the primary planning document and guide the achievement of the entity’s objectives and key priorities.14 It will also ensure compliance with the requirements of the PGPA Act and position the accountable authority to be able to accurately report its progress.15

Was the development of DCCEEW’s corporate plan supported by appropriate governance arrangements?

DCCEEW established governance arrangements and processes to support the development of both the 2022–23 and 2023–24 corporate plans. Implementation plans were used to support the drafting and approval processes for both corporate plans. To support performance measurement and reporting, the department developed ‘profiles’ of each measure, with certification by division heads and deputy secretaries that the measures complied with the PGPA Act.

Departmental governance and oversight structures

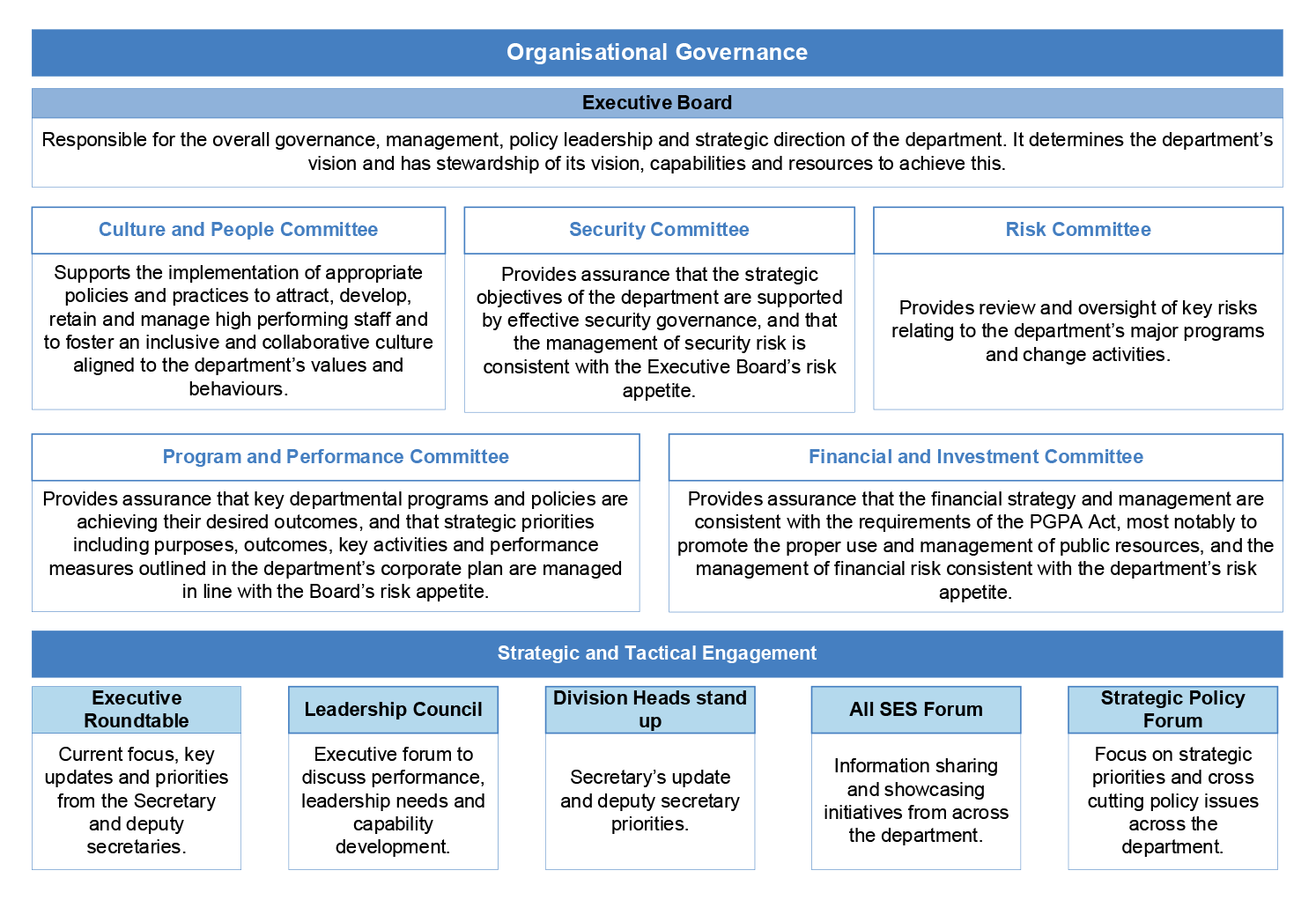

2.3 DCCEEW was established on 1 July 2022 and the Executive Board met for the first time on 15 July 2022. The Executive Board Charter (approved by the Executive Board in December 2023) states that the Executive Board is responsible for the overall governance and strategic direction of the department. This includes oversight of the development, implementation, and review of the corporate plan.

2.4 The Executive Board consists of the Secretary and deputy secretaries and meets fortnightly. On 10 August 2022, the Executive Board agreed to a structure for DCCEEW’s governance committees and forums, establishing two categories of governance groups (depicted in Figure 2.1).

- Organisational Governance groups provide the key decision-making and governance mechanisms and are supported by formal secretariat arrangements. Board committees were established with decision-making authority through terms of reference.

- Strategic and Tactical Engagement groups provide forums for updates from the Secretary and deputy secretaries on current focus areas and provide opportunities for information sharing and showcasing activities. Actions are tracked by operational areas.

2.5 The Executive Board endorsed terms of reference for each committee. The terms of reference require the chair of each committee to report to the Executive Board after each meeting. The committees first met in November and December 2022, and the first reports were provided to the Executive Board on 14 December 2022.

2.6 The Performance and Audit Team within the Portfolio Strategy Division is responsible for preparing the corporate plans, drafting the non-financial aspects of the Portfolio Budget Statements (PBS), preparing drafts of the annual report, supporting the department’s approach to performance reporting, and managing the department’s internal audit function.

Figure 2.1: DCCEEW governance committees and forums

Note: The Executive Board established a Work Health and Safety Committee in August 2022, which was subsequently merged into the Culture and People Committee in April 2023.

The Risk Committee was established in December 2023.

Source: DCCEEW intranet and internal documentation.

Development of the 2022–23 Corporate Plan

2.7 On 24 August 2022, the Executive Board discussed a one-page ‘Corporate Roadmap’ that outlined proposed approaches to developing ‘key corporate artefacts’ for the newly established department, including a new corporate plan. The Executive Board agreed:

- to publish the inaugural corporate plan ‘by January/February 2023’;

- that an Executive Board strategy session would be held in October 2022 ‘to provide a top-down perspective on a vision, purpose and brand identity to frame and guide staff consultations’;

- to discuss the principles and interim purpose statement with the SES, including at a full day SES forum in November 202216;

- to include broader consultation with staff;

- that the development of the interim purpose statement and principles would be discussed at the Strategic Policy Committee17; and

- to procure an external consultant to assist with the ‘establishment of corporate planning’ and other communication activities.

2.8 In November 2022, DCCEEW developed a plan to guide the preparation of the 2022–23 Corporate Plan. The plan included timeframes, key deliverables and consultation arrangements and aligned with the original consultation approach agreed by the Executive Board in August 2022. Twelve deliverables were to be completed over five months from October 2022 to February 2023. Figure 2.2 provides the deliverables and timeframes as agreed by the Executive Board in November 2022. All 12 deliverables were completed in accordance with the plan.

Figure 2.2: 2022–23 Corporate Plan development plan

Source: DCCEEW internal documentation.

Consultation

2.9 DCCEEW planned to consult with the Australian Public Service Commission, the Department of the Prime Minister and Cabinet, and the National Indigenous Australians Agency on the draft vision and purposes. Consultation occurred with the Australian Public Service Commission, the Department of the Prime Minister and Cabinet, and the Department of Finance. Consultation did not occur with the National Indigenous Australians Agency.

2.10 The 2022–23 Corporate Plan lists external organisations and bodies that will make a significant contribution towards achieving the entity’s purposes. On 8 March 2024, DCCEEW advised the ANAO that it relies on operational areas of the department to engage with partners and stakeholders and to take this into consideration when providing input into the corporate plan.

Publication

2.11 In August 2022, the Executive Board agreed the 2022–23 Corporate Plan would be published by ‘January/February 2023’ (see paragraph 2.7). In January 2023, the Executive Board was provided with a revised publication date of ‘late February/early March 2023’.

2.12 The deliverables and timeframes agreed by the Executive Board on 28 November 2022 stated that the design phase for the 2022–23 Corporate Plan would start in October 2022 (see paragraph 2.8). These actions occurred over November and December 2022. DCCEEW published its first corporate plan for 2022–23 in March 2023.

Development of performance measures

2.13 The 2022–23 Corporate Plan contained 19 performance measures against which performance of DCCEEW’s purposes would be measured. DCCEEW developed a measure profile to support each of these measures during the development of the 2022–23 Corporate Plan.

2.14 The measure profiles contained:

- the relevant PBS outcome and program;

- the data source and methodology for selecting, analysing and validating the data;

- an assessment of compliance with the PGPA Rule; and

- the previous department from which the measure had come, if applicable.

2.15 Each measure profile required certification by the relevant division head (the ‘measure owner’), including sign-off of the assessment of the measure against section 16EA of the PGPA Rule.

2.16 Profiles for 11 measures were incomplete. Ten profiles did not provide information on relevant departmental or public outputs relating to the measure. Four measure profiles did not provide the date of certification by the measure owner. DCCEEW was unable to provide evidence of certification by measure owners for the measure profiles.

Consideration of risks to the development of the 2022–23 Corporate Plan

2.17 DCCEEW established its Enterprise Risk Management Framework in March 2023. Before March 2023, DCCEEW staff were instructed to operate under the risk management framework from the previous Department of Agriculture, Water and the Environment and Department of Industry Science, Energy and Resources.

2.18 During the development of the 2022–23 Corporate Plan, the Executive Board considered the risk of not setting a clear purpose for the department; the risk of not complying with legislative requirements; the risk of poor staff engagement; and the risk of not delivering within a tight timeframe. Controls were identified and implemented for three of the four risks. A control was not identified for the risk of not delivering within the timeframe.

Development of the 2023–24 Corporate Plan

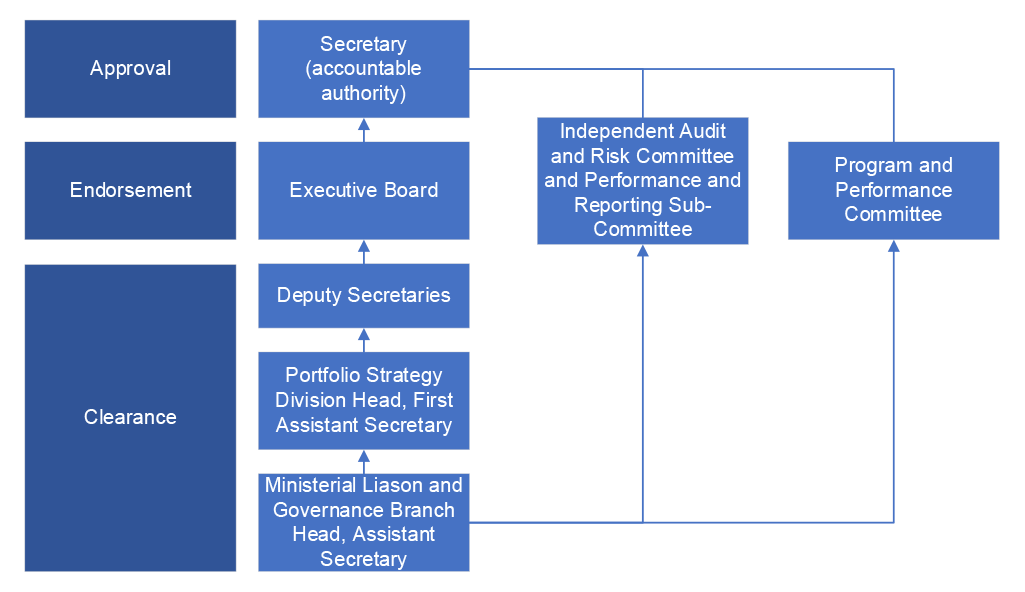

2.19 DCCEEW drafted an implementation plan to guide the development of the 2023–24 Corporate Plan. The 2023–24 Corporate Plan Implementation Plan included a timeline, roles and responsibilities, requirements regarding record keeping, and a governance structure. The 2023–24 Corporate Plan Implementation Plan was not required to be approved by a governance committee, and was not approved by the division responsible for corporate plan development.

2.20 Figure 2.3 provides the governance structure for the development of the 2023–24 Corporate Plan as presented in the Corporate Plan Implementation Plan.

Figure 2.3: Governance over 2023–24 Corporate Plan development

Note: Section 17 of the PGPA Rule requires the audit committee of a Commonwealth entity to provide independent advice and assurance to the entity’s accountable authority.

The Program and Performance Committee was established by the Executive Board to support the Executive Board (see Figure 2.1).

Source: DCCEEW 2023–24 Corporate Plan Implementation Plan.

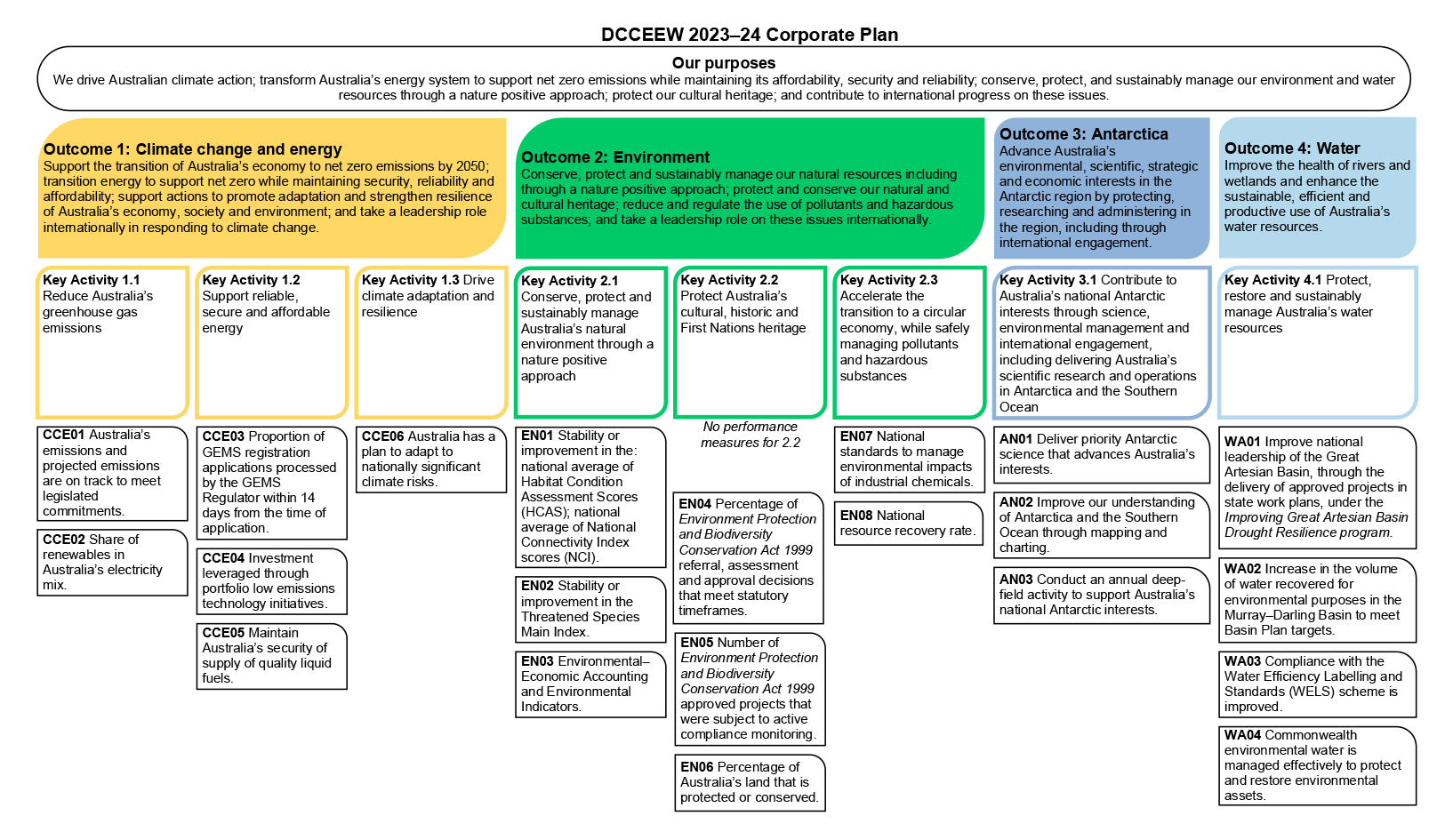

2.21 The 2023–24 Corporate Plan was published five months after the 2022–23 Corporate Plan was published. The changes that were made in the 2023–24 Corporate Plan largely related to continuing to develop performance measures.

2.22 The 2023–24 Corporate Plan Implementation Plan outlines milestones that were to be completed over three months from May to August 2023. Of 12 key milestones in the 2023–24 Corporate Plan Implementation Plan, 11 were achieved as planned. The 2023–24 Corporate Plan Implementation Plan intended that the draft 2023–24 Corporate Plan would be provided to the Secretary twice. The Secretary was provided with the draft 2023–24 Corporate Plan once, after it was reviewed by the Executive Board and the Program and Performance Committee.

2.23 The Program and Reporting Sub-Committee (a sub-committee of the Audit Committee) provided assurance over the 2023–24 Corporate Plan and performance measures, discussing some of the measure profiles in detail. The Executive Board and the Program and Performance Committee both endorsed the draft 2023–24 Corporate Plan.

Consultation

2.24 The Corporate Plan Implementation Plan did not include consultation with external entities involved in contributing to meeting DCCEEW’s outcomes. DCCEEW engaged with the Department of Finance in the development stages of the corporate plan, on alignment with section 16EA of the PGPA Rule.18

Measure profiles

2.25 The 2023–24 Corporate Plan Implementation Plan included a template for measure profiles as was used to support performance measures included in the 2022–23 Corporate Plan (see paragraph 2.14). The template included an assessment of compliance with section 16EA of the PGPA Rule. In July 2023, measure profiles were prepared for all 21 measures using the template.

2.26 The Implementation Plan included templates for measure owners (division heads) and deputy secretaries to certify that ‘the information contained in the 2023–24 Corporate Plan relating to [the performance measure] complies with section 16EA of the PGPA Rule 2014’. Certification was acquired through email. The emails requesting certification did not include the measure profile being certified for six of the 13 measure owners. Of 21 performance measures in the 2023–24 Corporate Plan, 20 were certified by the relevant measure owner, and all were certified by the relevant deputy secretary.19

2.27 The ANAO met with measure owners in January 2024 to discuss their role in certifying the performance measures. Measure owners reported being confident they understood their role and were sufficiently supported by the Portfolio Strategy Division, which was coordinating the measure profile completion and certifications.

2.28 The 2023–24 Corporate Plan Implementation Plan notes that particular attention would be paid to whether the measures were reliable, verifiable, and free from bias.20 DCCEEW advised the ANAO on 1 March 2024 that this occurred through the self-assessment against section 16EA of the PGPA Rule in the development of the measure profiles.

Consideration of risks to the development of the 2023–24 Corporate Plan

2.29 DCCEEW’s Enterprise Risk Management Framework released in March 2023 requires risk management to be integrated into planning and decision-making. No formal risk assessments were undertaken for the development of the 2023–24 Corporate Plan. No risks to the development of the 2023–24 Corporate Plan were considered by the Executive Board.

Does the corporate plan meet the mandatory requirements of the PGPA Act and PGPA Rule?

The 2022–23 and 2023–24 corporate plans were provided to relevant ministers and published in accordance with required timeframes. The corporate plans meet the mandatory content requirements of the Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) and place DCCEEW in a good position to provide meaningful and accurate performance information to the Parliament. DCCEEW has identified a mix of quantitative, qualitative, output and effectiveness measures across all outcomes. DCCEEW has not identified efficiency measures.

Minimum publishing and content requirements

2.30 The accountable authority of a Commonwealth entity must prepare and publish a corporate plan each year in accordance with any requirements prescribed by the PGPA Rule.21 Section 16E of the PGPA Rule outlines the content and publishing requirements for these corporate plans.

Publishing requirements

2.31 Both corporate plans were provided to the Minister for the Environment and Water, the Minister for Climate Change and Energy, and the Minister for Finance prior to publishing them on the department’s website, as required by the PGPA Rule.22

2.32 Corporate plans must be published ‘by the last day of the second month of the reporting period for which the plan is prepared’.23 The PGPA Rule makes a provision for new entities to publish the first corporate plan ‘as soon as practicable after the plan is prepared.24

2.33 The 2022–23 Corporate Plan was published on 10 March 2023. The 2023–24 Corporate Plan was published by the required date of 31 August 2023. DCCEEW met the minimum requirements for the publication of its 2022–23 and 2023–24 corporate plans.

Content requirements

2.34 The PGPA Rule requires that specific matters be included in entity corporate plans.25 Resource Management Guide (RMG) 132 provides guidance on how to fulfil the requirements of the PGPA Rule.26 Table 2.1 provides an assessment of the content of the 2022–23 and 2023–24 corporate plans against the requirements of the PGPA Rule, as per the guidance in RMG 132.

Table 2.1: Minimum corporate plan content requirements for 2022–23 and 2023–24

|

PGPA Rule requirements |

ANAO assessment |

|

|

Subsection 16E(1) Introduction Statement of preparation Reporting period planned Reporting period covered |

● |

A statement of preparation is included; the reporting period for which the plan is prepared is included; the reporting periods covered by the plan is included. |

|

Subsection 16E(2) Purposesa |

● |

The purposes statement is in line with RMG guidance. |

|

Subsection 16E(3) Key activities |

● |

The 2022–23 Corporate Plan contains 11 key activities and the 2023–24 Corporate Plan contains 8 key activities that will assist DCCEEW in achieving its purposes. Each key activity relates to a different program area. |

|

Subsection 16E(4) Operating context Environment |

● |

Most of the discussion relates to issues beyond the control of DCCEEW but states the main program that will influence DCCEEW’s response. |

|

Subsection 16E(4) Operating context Capability |

● |

Both corporate plans include strategies to improve DCCEEW’s capabilities or outline process, systems and committees in place to support the capabilities. |

|

Subsection 16E(4) Operating context Risks |

● |

Provides description of risk management systems, enterprise risks and risk governance. |

|

Subsection 16E(4) Operating context Cooperation |

◕ |

More information and a greater level of detail was included in the 2023–24 Corporate Plan. Specific examples of programs are listed that are influenced by the cooperative relationships. Not all entities that are identified in the PBS as contributing to multiple shared objectives are included. |

|

Subsection 16E(4) Operating context Subsidiaries |

N/A |

DCCEEW does not have subsidiaries. |

|

Subsection 16E(5) Performance Performance measures Targets |

◕ |

15 of the 19 performance measures in the 2022–23 Corporate Plan and 18 of the 21 performance measures in the 2023–24 Corporate Plan provide a good basis for measuring performance (see paragraphs 2.39 to 2.49). |

Key: ○ Requirement has not been met ◔ Requirement has been partially met ◑ Requirement has been half met ◕ Requirement has been largely met ● Requirement has been met.

Note a: DCCEEW’s corporate plan also contains a vision. A vision statement is not a requirement under the PGPA Act and the ANAO has not audited DCCEEW’s vision.

Source: ANAO analysis of DCCEEW’s 2022–23 and 2023–24 corporate plans.

2.35 As demonstrated in Table 2.1, DCCEEW met the mandatory requirements of section 16E of the PGPA Rule.

2.36 Subsection 16E(2) of the PGPA Rule requires the corporate plan to include ‘details of any organisation or body that will make a significant contribution towards achieving the entity’s purpose through cooperation with the entity, including how that cooperation will achieve those purposes’.27 RMG 132 highlights that this requirement ‘aligns with the requirement for entities who produce Portfolio Budget Statements to report links to the programs of other entities which assist them achieve their Outcomes’.28

2.37 The 2023–24 PBS lists 30 Australian Government entities who deliver programs that contribute to achieving DCCEEW’s outcomes.29 Five of those 30 entities contribute to three or four of DCCEEW’s outcomes (see Table 2.2).

Table 2.2: Entities in DCCEEW’s PBS that contribute to three or four of DCCEEW’s outcomes

|

Australian government entity listed in the DCCEEW PBS that contributes to three or four outcomes |

DCCEEW’s outcomes the entity contributes to as listed in the PBSa |

ANAO analysis — Is the entity listed in DCCEEW’s corporate plan? |

|

Bureau of Meteorology |

1, 2, 3, 4 |

✔ |

|

Commonwealth Scientific and Industrial Research Organisation |

1, 2, 3 |

✔ |

|

Department of Foreign Affairs |

1, 2, 3 |

✔ |

|

Department of Industry, Science and Resources |

1, 2, 3 |

✘ |

|

Department of the Treasury |

1, 2, 4 |

✘ |

Note a: DCCEEW has four outcomes. The outcomes relate to: 1 — Climate change and energy; 2 — Environment; 3 — Antarctica; 4 — Water. See Appendix 3 for the full outcome statements.

Source: 2023–24 Budget Paper 1.3. Climate Change, Energy, the Environment and Water Portfolio and DCCEEW 2023–24 Corporate Plan.

2.38 The 2023–24 Corporate Plan does not include the Department of Industry, Science and Resources, or the Department of the Treasury, although both departments contribute to achieving three of DCCEEW’s four outcomes. On 15 December 2023, DCCEEW advised the ANAO that organisations and bodies in the 2023–24 Corporate Plan were ‘initially identified as part of the (Machinery of Government) arrangements, then tested with the Executive Board as part of the consultation process’.

Performance measures

2.39 Australian Government entities are required to include performance measures in their corporate plan to measure and assess their performance in the reporting period. The performance measure results are included in the entity’s annual performance statements in the annual report, which is tabled in the Parliament at the end of the reporting period. To meet the requirements of the PGPA Rule, each performance measure must:

- relate directly to one or more purposes or key activities;

- use information sources and methodologies that are reliable and verifiable;

- provide an unbiased basis for measurement/assessment; and

- provide a basis for assessment of entity’s performance over time.30

2.40 Collectively the measures must, where reasonably practicable, comprise a mix of quantitative and qualitative measures and include measures of an entity’s output, efficiency, and effectiveness if these are appropriate.31

2.41 The ANAO was funded as part of the 2021–22 Budget to implement the ongoing program of performance statements audits. This funding established assurance of non-financial reporting as a core component of assurance to the Parliament. Conducting annual audits of performance statements ensures that the Parliament receives the same level of assurance on performance statements as it does for financial statements.32 On 16 January 2023, in response to correspondence from the Auditor-General, the Minister for Finance requested, under section 40 of the PGPA Act, that the Auditor-General undertake assurance audits of the Department of Industry, Science and Resources and the Department of Infrastructure, Transport, Regional Development, Communications and the Arts instead of the Department of Employment and Workplace Relations33 and DCCEEW as part of the 2022–23 audit program.34

Measures in the 2022–23 Corporate Plan

2.42 The 2022–23 Corporate Plan contained 19 performance measures. Appendix 3 contains a list of DCCEEW’s purpose, outcomes, key activities, and performance measures in the 2022–23 Corporate Plan. Each measure included targets and was supported by a rationale, methodology and data sources that will be used, and outputs. The corporate plan identified the type of each performance measure such as effectiveness or output as well as if it was a quantitative or qualitative measure. The corporate plan also identified regulatory measures.35

2.43 Of the 19 measures, the ANAO assessed that 15 provided a good basis for measuring performance and complied with the requirements of section 16EA of the PGPA Rule. Section 16EA of the PGPA Rule requires that performance measures must provide an unbiased basis for measurement or assessment. The ANAO assessed that three of the 2022–23 performance measures had a risk that the measurement or assessment of the results in the annual performance statements could be biased. Each of these three measures had targets without clearly pre-defined tolerances and reporting against the target in the annual performance statements could be biased towards being achieved or partly achieved.

2.44 Collectively, the 2022–23 performance measures comprised effectiveness, outputs, and qualitative and quantitative measures. DCCEEW identified one performance measure (EN06) as an efficiency measure, however the ANAO assessed this measure as not meeting the definition of an efficiency measure as it does not assess cost or the ratio of input to outputs.36 DCCEEW did not consider this measure an efficiency measure in 2023–24.

Measures in the 2023–24 Corporate Plan

2.45 DCCEEW revised its performance measures for its 2023–24 Corporate Plan by:

- adding seven new measures;

- removing five measures; and

- amending nine measures, including by adding an additional target to one measure.37

2.46 Three of the 21 measures in the 2023–24 Corporate Plan may not meet all PGPA Rule requirements as they are either at risk of bias or may not provide a measure of performance over time. This may limit DCCEEW’s ability to accurately measure these activities and demonstrate performance against its key activities over time.

2.47 The 2023–24 Corporate Plan included more qualitative measures than in the previous year. DCCEEW had not identified any performance measures as efficiency measures for 2023–24.

2.48 On 8 March 2024, DCCEEW advised the ANAO that the Executive Board would consider proxy measures for efficiency for inclusion in the 2024–25 Corporate Plan. Further information relating to improvements made by DCCEEW are outlined in paragraphs 4.30 to 4.34 and Appendix 2.

2.49 Compliance with the performance framework, including the development of appropriate performance measures, is positioning DCCEEW to be able to accurately report its performance against its key activities to the Parliament. DCCEEW needs to continue to refine its performance measures to ensure they provide an unbiased basis for measurement and provide a basis for assessment of performance over time.

Has DCCEEW appropriately applied the clear read principle?

DCCEEW has provided a clear read across relevant Portfolio Budget Statements (PBS) and corporate plans from 2022–23 to 2023–24. Changes in performance information have been communicated to allow users and the Parliament to track the changes between the documents and across performance cycles.

2.50 The Commonwealth Performance Framework provides that entities draw a clear line of sight between planned and actual performance.38 Performance measures in the corporate plan and PBS (and any other budget statements) are reconciled in the annual performance statements at the end of each reporting period, which are included in the entity annual report that is tabled in the Parliament. As such, ‘it is important that the performance measures in both planning documents are consistent and work together to enable a coherent set of performance results to be included in the annual performance statements. This provides a clear read between these documents.’39

Alignment in the 2022–23 performance cycle

2.51 There was alignment across the outcomes, programs, key activities and performance information presented in in the 2022–23 PBS and the 2022–23 Corporate Plan. Outcomes in the 2022–23 PBS were reflected in the 2022–23 Corporate Plan. There was alignment between the programs in the 2022–23 PBS and key activities in the 2022–23 Corporate Plan. The key activities in the 2022–23 Corporate Plan were aligned to relevant outcomes.

2.52 The 2022–23 PBS contained one performance measure per program. The corporate plan contained ten additional measures across five programs and key activities. There were minor changes to some measures and targets.

2.53 There were minor changes between the performance measures in the 2022–23 PBS and the 2022–23 Corporate Plan. DCCEEW’s 2022–23 PBS noted that ‘[a]s per Department of Finance direction, one measure has been applied per program’.40 Two performance measures in the 2022–23 Corporate Plan replaced measures in corporate plans from the departments that were previously responsible for those functions, prior to DCCEEW’s establishment.41

2.54 DCCEEW’s 2022–23 PBS was released on 25 October 2022 — just under four months after DCCEEW was established on 1 July 2022 — and its first corporate plan was released in March 2023. On 9 February 2024, DCCEEW advised the ANAO that the 2022–23 PBS did not contain a full suite of performance measures because the department was reviewing its measures for the 2022–23 Corporate Plan.

2.55 Appendix 1 in the 2022–23 Corporate Plan contains an explanation of the changes to performance measures designed by the previous function holders — the Department of Industry, Science, Energy and Resources, and the Department of Agriculture, Water and Environment — as well as changes since the 2022–23 PBS.

Alignment in the 2023–24 performance cycle

2.56 The 2023–24 PBS was tabled in May 2023 and the 2023–24 Corporate Plan was published in August 2023 (see Figure 1.4). Clear read across the performance cycles is examined further below.

2.57 DCCEEW reviewed its performance measures in line with revised outcomes and key activities in 2023–24. The 2023–24 PBS and 2023–24 Corporate Plan maintained clear connections between each element, with key activities and performance measures in the 2023–24 Corporate Plan aligned to each PBS outcome, which led up to the department’s overarching purposes.

2.58 The 2023–24 Corporate Plan included a new key activity with a new performance measure under Outcome 1, following additional funding in the 2023–24 budget.42 It is good practice for entities to consider the key activities and performance measures that should be included in their corporate plan on the basis of program appropriations. Where there are large appropriations for specific policies, activities or projects, entities should consider including a measure or measures to promote accountability and transparency and enable parliamentary and government scrutiny of whether these policies, activities or projects are delivering their intended return on investment and meeting the expectations of government.43

2.59 In total, there were 12 performance measures included in the 2023–24 Corporate Plan that were not in the PBS.

- Four were performance measures that were included in the previous year’s corporate plan that had been carried across.

- Eight performance measures across five key activities were newly introduced in the 2023–24 Corporate Plan.

2.60 One key activity under Outcome 2 did not have any performance measures in the corporate plan.44 The heritage performance measure included in the PBS was not in the corporate plan. The corporate plan noted that a number of reforms are progressing in the heritage space and stated that ‘[t]he development of future performance measures are currently under review and will be influenced by progress on these reforms’.45

Line of sight across performance cycles

2.61 Demonstrating how reporting on performance information changes over time allows entities to demonstrate how priorities change and enables the Parliament to monitor the delivery of parliamentary priorities. Providing a clear line of sight in planning documents across years (from 2022–23 to 2023–24) enables comparison across performance cycles. This line of sight is provided if performance information that has been added to, amended, or removed between performance cycles is clearly explained to the reader.46

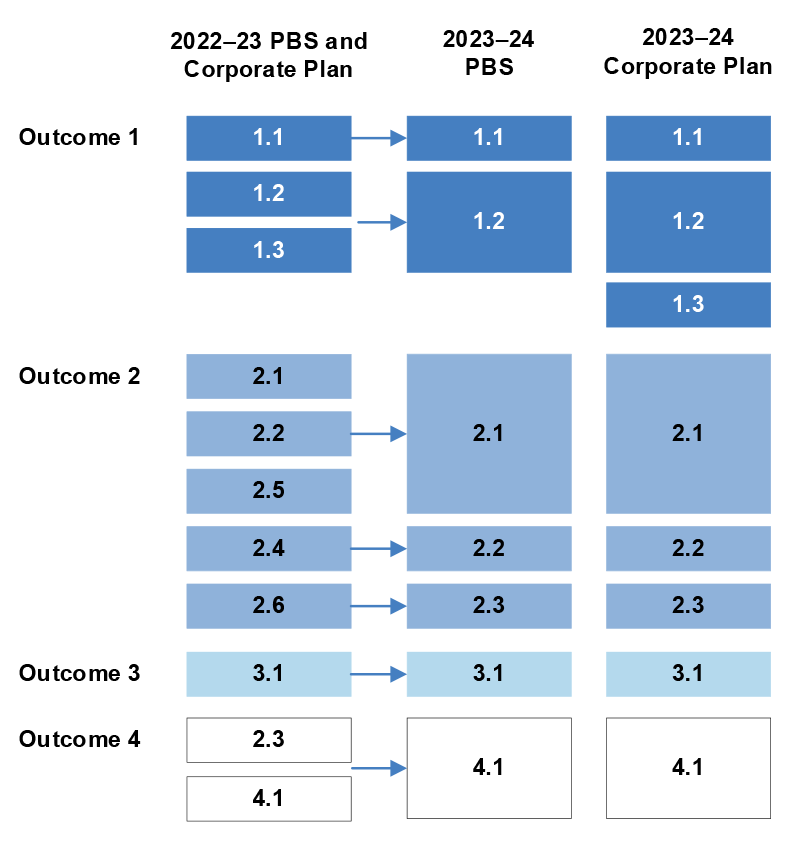

2.62 The programs and key activities outlined in the 2022–23 performance documents were revised for the 2023–24 PBS. As noted at paragraph 2.58, a new key activity (1.3) was introduced under Outcome 1 in the 2023–24 Corporate Plan. Figure 2.4 illustrates the changes in program structure between the documents.

Figure 2.4: Comparison of 2022–23 and 2023–24 programs and key activities

Source: ANAO summary of departmental information.

2.63 Consistent with guidance from Department of Finance, these changes were outlined in DCCEEW’s 2023–24 PBS.47 The PBS noted that ‘[t]he department is currently reviewing its performance information in the context of new government and departmental responsibilities and initiatives’, with further refinements to be reflected in the 2023–24 Corporate Plan. The 2023–24 Corporate Plan stated that the department had revised its outcomes and programs in the 2023–24 PBS ‘to better reflect our core work’. This approach provided users with context for the changes and a basis for comparison with previous year’s performance information.

2.64 As outlined in paragraph 2.45, across DCCEEW’s 2022–23 and 2023–24 corporate plans, seven new measures were added, five measures were removed, and nine measures were revised. A detailed explanation for these changes was provided in Appendix 1 of the 2023–24 Corporate Plan. Readers were alerted that performance measures had been revised ‘in line with the revised outcomes and key activities’ before the performance information was presented in the corporate plan, and were directed to Appendix 1 for a summary of the changes. This approach assists the reader to identify differences in an entity’s performance compared to the previous year, and understand why they occurred, facilitating clear read.

3. Implementation

Areas examined

This chapter examines whether the Department of Climate Change, Energy, the Environment and Water (DCCEEW) is effectively implementing its corporate plan.

Conclusion

DCCEEW is partly effective in implementing its corporate plan. The corporate plan has not yet been fully integrated into the department’s planning and reporting frameworks. DCCEEW has established appropriate governance structures to provide oversight over corporate plan implementation. In March 2023, DCCEEW developed an Enterprise Risk Management Framework (ERMF) and identified eight enterprise risks. Committees are not providing effective oversight over all enterprise risks and the enterprise risks are not being managed in accordance with the ERMF. The nature of committee reporting to the Executive Board limits the Board’s ability to have assurance over enterprise risk management. DCCEEW developed an Enterprise Performance Framework to support regular reporting against the performance measures listed in the corporate plan.

Areas for improvement

The ANAO made one recommendation around the management of enterprise risks. The ANAO identified two opportunities for improvement to ensure corporate plan information technology priority and focus areas are achieved, and ensure decision-making is supported by regular reporting.

3.1 Under the Commonwealth Performance Framework, the corporate plan is intended to be an entity’s primary planning document. Strategic priorities identified in the corporate plan should be actively used by the entity to support decision making and manage the business, and senior management should have oversight over the implementation of these strategic priorities.

3.2 In addition to identifying key activities the entity will undertake to achieve its purposes, a corporate plan includes strategies and plans the entity will implement to have the capability it needs, and a summary of the risk oversight and management systems of the entity including key risks the entity will manage.48

Has corporate planning effectively informed business planning?

DCCEEW used the 2022–23 Corporate Plan to develop and embed purposes for the new department. The 2022–23 Corporate Plan published in March 2023 was intended to inform DCCEEW’s business and divisional planning. The first stage of this divisional planning occurred in October 2023. The corporate plan identified nine areas of capability development to support DCCEEW’s delivery of key activities. Five are being implemented. The priority focus areas for information technology (IT) that were identified in both corporate plans have not been reflected in enterprise-wide IT and digital transformation strategies and plans.

Strategies to support the implementation of the corporate plan

3.3 DCCEEW used the development of the purposes and vision in the 2022–23 Corporate Plan to set the strategic direction for the new department and discuss tensions inherent in the department’s climate change, energy and environmental activities.

3.4 When it endorsed the 2022–23 Corporate Plan, the Executive Board agreed to a range of proposed activities to embed the vision and purposes throughout the department. The activities DCCEEW implemented included publishing the corporate plan on the DCCEEW intranet, an internal video message from the Secretary and deputy secretaries, an all Senior Executive Services briefing on 10 March 2023 to launch the corporate plan, and the creation of a visual identity incorporating First Nations themes.49 A corporate plan intranet page and a process to help staff undertake divisional planning under the corporate plan were delivered following the release of the 2023–24 Corporate Plan in August 2023.

Divisional planning

3.5 The 2022–23 Corporate Plan was intended to inform DCCEEW’s divisional plans; staff development plans; and monitoring and reporting, insights and analytics. Following the release of the 2022–23 Corporate Plan, the Portfolio Strategy Division advised the Executive Board it would ‘work with divisions to prepare business plans that define the key activities under each program’. The Executive Board agreed to having ‘mature business plans complete at the divisional level prior to the new financial year in 2023–24’.

3.6 The Executive Board agreed to a divisional planning process in July 2023. The process comprised documenting the priorities of each division under key activities, identifying activities that cut across the department, and the main risks to being able to deliver key priorities. This process was ‘to align with the release of the 2023–24 Corporate Plan’.50

3.7 The first stage of the process commenced in October 2023 when the Portfolio Strategy Division provided divisional planning information to divisions. The Portfolio Strategy Division prepared information to support divisional planning to ‘create a line of sight from the vision, purposes, outcomes and key activities to the work of the division’.

- Four ‘corporate cascades’ were prepared — one for each of the four outcomes — to guide the divisional consideration of strategic priorities.

- The cascades provide ‘high-level mapping of legislation, Portfolio Budget Statement budget measures, ministerial priorities, and major departmental programs/projects/initiatives’.

- The cascades were provided to deputy secretaries and heads of divisions with a request to identify divisional priorities and activities that cut across divisions and were uploaded to DCCEEW’s intranet.

- A divisional business plan template was uploaded to DCCEEW’s intranet. It included a section to identify alignment with the outcomes and key activities supported by the divisional activities.

3.8 Divisional plans prepared through this process demonstrate that divisions have considered to which key activities and outcomes their work contributes, and their priorities under the key activities. The divisional plans do not provide information on available resourcing or capabilities to deliver these strategic priorities and key activities.

3.9 On 8 January 2024, DCCEEW advised the ANAO that it was collating the divisional risk registers as part of the divisional planning process.

3.10 On 7 May 2024, DCCEEW advised the ANAO that the second stage of the divisional planning process involved targeted workshops with each division to identify out of tolerance risks. DCCEEW plans to ‘embed risk monitoring and review into a division level planning cycle to maintain focus on these risks by relevant risk owners’.

Enterprise Performance Framework

3.11 In November 2023, the Executive Board agreed to a ‘performance framework and measures uplift’ through the development of:

an enterprise performance framework to provide a logical, consistent and transparent process for planning, monitoring and reporting (including key activities and performance measures) across the department.

3.12 The Executive Board was provided with a roadmap for the development of the Enterprise Performance Framework, with final approval and project closure scheduled for late February 2024. Table 3.1 lists the steps provided in the roadmap.

Table 3.1: Enterprise Performance Framework Roadmap

|

Date |

Action |

|

Oct – Nov 2023 |

|

|

Early Dec 2023 |

|

|

Mid Dec 2023 |

|

|

Jan 2024 |

|

|

Early Feb 2024 |

|

|

Mid Feb 2024 |

|

|

Late Feb 2024 |

|

Source: ANAO analysis of departmental documentation.

3.13 DCCEEW engaged Nous Group from November 2023 until February 2024 to provide the following two services.51

- Design new approach; including draft enterprise-level guidance on reviewing, developing and updating key activities and measures, and proposed updates to the key activities and measures.

- Delivery of final, endorsed enterprise performance framework, including finalised enterprise-level guidance and confirmed performance measure updates and final, endorsed measure documentation, including data dossiers, performance assessment tools, and third-party verifications.

3.14 The Enterprise Performance Framework was agreed by the Secretary in May 2024 following review by the Program and Performance Committee, Audit Committee and Performance Reporting Sub-Committee.

Developing capabilities

3.15 Subsection 16E(2) of the Public Governance and Performance Accountability Rule 2014 (PGPA Rule) requires entities to include ‘strategies and plans the entity will implement to have the capability it needs to undertake its key activities and achieve its purposes’. The 2022–23 and 2023–24 corporate plans outline nine strategies and plans to improve DCCEEW’s capabilities and deliver on its outcomes.52 By January 2024, five of the strategies and plans had been established and reflect the priorities identified in the 2023–24 Corporate Plan, as presented in Table 3.2.

Table 3.2: Delivering in capability development areas

|

Detail in the corporate plana |

ANAO assessment — Is the plan or strategy being implemented as planned? |

|

APS Reform agenda

|

◆ |

|

People Strategy

|

◆ |

|

Divisional workforce plans/ operational workforce planning

|

▲ |

|

Employee experience and culture program

|

▲ |

|

Place/properties

|

◆ |

|

Security

|

◆ |

|

ICT

|

▲ |

|

Digital services and transformation

|

▲ |

|

Regulator performanceb

|

◆ |

Key: ◆ Being implemented in accordance with the corporate plan ▲ Elements of the implementation are in accordance with the corporate plan ■ Not being implemented in accordance with the corporate plan.

Note a: The wording in the table is from the 2023–24 Corporate Plan.

Note b: The 2022–23 Corporate Plan does not contain this information on how DCCEEW will address regulator performance.

Source: ANAO analysis of departmental documentation.

3.16 Workforce plans analyse the current workforce, determine future workforce needs, identify the gap between the present and the future, and implement solutions to deliver on organisational goals.53 In March 2023, the 2022–23 Corporate Plan noted that DCCEEW was ‘working on operational workforce planning’. DCCEEW commenced the Operational Workforce Planning Initiative, ‘aimed at developing targeted operational workforce plans for each division’ in September 2023. Workforce plans were not in place during 2023. On 7 May 2024, DCCEEW advised the ANAO that ‘this work is now complete.’

3.17 The corporate plans describe an Employee Experience Program that is being developed to ‘enhance our culture and support our mission to be a model employer’. This program is to be supported by research and ‘map the employee life cycle … and build an understanding of individual staff experiences at important touchpoints over the course of their career’.54 On 16 November 2023, DCCEEW advised the ANAO that elements of the planned program are being implemented, such as an employee exit survey, action plans following the APS census, and employee pulse surveys.

3.18 DCCEEW is transitioning away from an ICT shared services arrangement with the Department of Agriculture, Fisheries and Forestry ‘to establish our own DCCEEW-managed ICT arrangement’.55 On 31 May 2023 the Executive Board considered a business case to guide this transition. This business case did not reflect the six IT priorities and focus areas provided in both corporate plans. On 6 March 2024, DCCEEW advised the ANAO that the procurement and build of ICT capabilities was re-scoped in December 2023 to allow it to occur in parallel with a May 2024 deadline.

3.19 The 2022–23 Corporate Plan provides that the department ‘will continue to review, refresh and increase its ICT capability to reduce dependency on outdated legacy systems … A new ICT Strategy will be developed, aligning with the broader directions of the department and the whole-of-government context’.56 On 4 October 2023 the Executive Board decided the transition from a shared services ICT arrangement would take primacy over transformation in the short-term. On 31 October 2023 DCCEEW proposed an approach to the development of a Business Technology Strategy to ‘provide strategic guidance for any area of DCCEEW that consumes or delivers technology’.

|

Opportunity for improvement |

|

3.20 DCCEEW align its enterprise-wide IT strategies and business cases with priorities identified in the corporate plan. |

Does DCCEEW have arrangements to monitor implementation of the corporate plan?

DCCEEW established five committees with roles related to the enterprise-wide monitoring of programs and performance. Each committee has a forward workplan that includes monitoring of plans and strategies in the corporate plan. In November 2023, DCCEEW commenced the development of an approach to regular reporting against performance measures through the Enterprise Performance Framework.

3.21 From the publication of the 2022–23 Corporate Plan in March 2023 until the end of December 2023, the Executive Board held 21 meetings. In these meetings, the Executive Board considered the strategies and plans listed in Table 3.2. The Executive Board’s 2023 forward workplan included regular updates on corporate plan strategies: quarterly updates on the People Strategy, including information on capability; and monthly updates in financial and property dashboards, including the average staffing level and property risks. The forward workplan included quarterly reporting on cyber security.

3.22 As outlined in paragraphs 2.4 and 2.5, the Executive Board established committees to assist its governance of DCCEEW. Each of these committees was established with terms of reference providing the committee with decision-making authority in its area of responsibility. Committee membership comprises between seven and 14 SES staff. The chair and deputy chair of each committee are to be held by staff at the deputy secretary level, with the exception of the Risk Committee, which is to be chaired by the Secretary.

3.23 The Culture and People Committee, Security Committee, Finance and Investment Committee, and Program and Performance Committee each had their inaugural meeting in November or December 2022, and all met five times during 2023. The Risk Committee was established in December 2023 and held its inaugural meeting in March 2024. According to its terms of reference it will ordinarily meet monthly.

3.24 Each committee has a role in enterprise-wide monitoring. Their monitoring role is provided in Table 3.3.

Table 3.3: Monitoring by Board committees

|

Committee |

Monitoring role as described in the committee’s terms of reference |

Number of times the committee has discussed a strategy or plan in the corporate plana |

|

Culture and People Committee |

Responsible for monitoring the implementation of key people related strategies, policies and plans. |

The People Strategy was discussed twice. |

|

Finance and Investment Committee |

Monitoring of divisional and departmental financial performance. |

The costs associated with the transition to DCCEEW-managed ICT services was discussed regularly. |

|

Program and Performance Committee |

Monitoring the manner of delivery and performance of DCCEEW programs in achieving objectives and desired outcomes. |

Regulatory functions were discussed 3 times. |

|

Security Committee |

Monitoring the effectiveness and progress of a security policy framework. |

The Agency Security Plan was discussed once. |

|

Risk Committee |

Reviewing and oversight of the department’s major programs and change activities. |

N/Ab |

Note a: This assesses the number of times a strategy or plan has been discussed since the release of the 2022–23 Corporate Plan in March 2023 until the end of December 2023.

Note b: The Risk Committee’s inaugural meeting was March 2024.

Source: ANAO analysis of departmental documentation.

3.25 All committees had forward workplans for 2023 and have developed forward workplans for 2024.57

Regular reporting against performance measures

3.26 In May 2023, DCCEEW informed the Audit Committee’s Performance Reporting Sub-Committee that quarterly reporting would ‘commence next financial year against the 2023–24 Corporate Plan’, incorporating ‘updated outcomes, key activities and performance measures’.

3.27 As discussed in paragraphs 3.11 to 3.14, DCCEEW commenced the development of an Enterprise Performance Framework in October 2023, and finalised the framework in May 2024. The framework provides four pillars, including: a ‘performance measurement culture’ where ‘we use data driven performance information in our daily behaviours to create insights that can inform decision-making’; and ‘performance measure practices’ including monitoring, reporting, and reviewing performance information. The framework notes the intention of the department to conduct ‘formal monitoring of measures quarterly’.

3.28 DCCEEW has not established systems or processes to support regular monitoring or reporting against the performance measures in the 2023–24 Corporate Plan, outside the preparation of the annual performance statements (see paragraphs 4.10 to 4.18). On 1 March 2024, DCCEEW advised the ANAO that:

A quarterly performance reporting process has been proposed, integrated into Division level business planning. We are looking to implement this approach following the release of the 2024-25 Corporate Plan in August 2024.

3.29 Non-financial performance information should be an integral part of strategic and operational planning, budgeting, reporting and reviewing processes. Regular monitoring and evaluation of performance information should provide a basis for informed and evidence-based decision-making and accountability. By way of comparison, it is unlikely that there would be confidence in an entity that did not use its financial information for management and business improvement purposes.58

|

Opportunity for improvement |

|

3.30 DCCEEW implement regular monitoring and reporting of its performance measures to support evidence-based decision-making and effective management and stewardship of public resources. |

Is DCCEEW managing the risks to achieving the outcomes in its corporate plan?

The 2022–23 and 2023–24 corporate plans identify eight enterprise risks and provide a narrative of how each risk will be managed. In February 2023, DCCEEW assigned governance committees with responsibility for the management of specific enterprise risks. The enterprise risks have not been assessed against departmental risk tolerances and the effectiveness of controls in managing the risks have not been assessed, in accordance with the ERMF. Committees discussed and considered control actions for four of the eight enterprise risks. The nature of committee reporting to the Executive Board limits the ability of the Board to have effective oversight of enterprise risk management.

Oversight of enterprise risks

3.31 The Executive Board is responsible for setting DCCEEW’s risk appetite and treating strategic risks. The Board’s forward workplan lists ‘setting and annual review of enterprise risks’ in March each year. The 2022–23 and 2023–24 corporate plans identify eight enterprise risks and provide a narrative of how each risk will be managed.

3.32 On 25 January 2023, the Executive Board considered enterprise risks and a risk appetite statement proposed to be included in the 2022–23 Corporate Plan. The proposed risks were identified as ‘the overarching risks that may impact delivery of our purpose and were identified by divisions as part of recent updates to Divisional Risk Registers’. The enterprise risks were approved by the Executive Board on 25 January 2023 and subsequently included in the 2022–23 Corporate Plan.

3.33 At the time of approving the enterprise risks, the Executive Board was not presented with an assessment of enterprise risks including whether risks were within tolerances.

3.34 DCCEEW released its Enterprise Risk Management Framework (ERMF) in March 2023. The ERMF was updated in September 2023 with minor edits. The ERMF seeks to embed a positive risk culture in the department and outlines the approach for ‘embedding risk management into our culture, work practices and decision making’. It is underpinned by the principles of a positive risk culture; embedding a risk strategy; appropriate risk governance; and processes and procedures to deliver risk management practices. The ERMF aligns with all nine elements of the Commonwealth Risk Management Policy.59

3.35 The Executive Board did not review or discuss enterprise risks during the development of the 2023–24 Corporate Plan and the enterprise risks did not change from the 2022–23 Corporate Plan.60

Board committee review and oversight of enterprise risks

3.36 The Executive Board agreed in February 2023 that the ‘Chair of each governance committee will be assigned accountability for the management of the relevant enterprise risks on behalf of the Secretary’. The 2022–23 and 2023–24 corporate plans specify which Executive Board committee is responsible for overseeing the enterprise risks. Each committee includes its role with regard to enterprise risks in its terms of reference. Table 3.4 identifies the committee responsible for each enterprise risk and describes how each committee exercised its oversight of enterprise risks during 2023.

Table 3.4: Enterprise risk oversight by Executive Board committees

|

Executive Board committee |

Enterprise risk/s the committee is responsible for |

ANAO analysis of committee oversight |

|

Program and Performance Committee (PPC) |

1. We are unable to deliver or implement effective regulatory practice, or influential, integrated and innovative policy. |

During 2023 the PPC considered the regulatory functions of DCCEEW in June, October and December, and effective delivery of policies and programs in June and October. |

|

2. We do not develop effective relationships with stakeholders. |

The PPC has not considered stakeholder relations or the impact of DCCEEW’s operations on the environment, during 2023. |

|

|

5. We do not prevent or limit negative impacts on the natural environment in the delivery of our operations. |

||

|

7. We are unable to ensure the integrity and availability of data and deliver secure, integrated and reliable information systems.a |

The PPC considered data governance, and the development of a data governance strategy in August, October and December 2023. |

|

|

Finance and Investment Committee (FIC) |

6. We do not appropriately manage our financial processes, assets, projects, budgets and investments. |

Discussed in March 2023. Draft risk profile discussed April 2023. |

|

8. We do not have effective, efficient and fit for purpose systems and processes to meet operational needs. |

Recognised oversight of this risk in April 2023 during discussion of draft risk profile. |

|

|

Culture and People Committee (CPC) |

3. We are unable to attract, develop and retain the people and integrity capabilities required. |

In February 2023 the CPC noted its responsibility for the enterprise risk 3. The CPC discussed updated Terms of Reference in July, including the addition of enterprise risk 4. |

|

4. We do not protect the health, safety and wellbeing of our people and other persons under our care.b |

||

|

Security Committee |

7. We are unable to ensure the integrity and availability of data and deliver secure, integrated and reliable information systems.a |

Discussed in March and May 2023. |

Note a: The responsibility for enterprise risk seven is shared between the PPC and Security Committee. This risk is not listed in the PPC’s terms of reference. This risk was not included in the version of the risk profile snapshot provided to the Audit Committee in June (see paragraph 3.40). It was included in the September snapshot and mis-assigned to the FIC.

Note b: The CPC was given responsibility for enterprise risk four in July 2023, following the merging of the Work Health and Safety Committee into the CPC in April 2023.

Source: ANAO analysis of departmental documentation.

3.37 In February 2023, DCCEEW proposed to develop a risk profile for each enterprise risk. The profiles would ‘complement existing reporting to governance committees to support the oversight and management of the risks’.