This chapter examines the reported use of confidentiality provisions in Australian Government contracts over time, and the appropriateness of the use and reporting of specific confidentiality provisions in a sample of contracts.

Background

3.1 The Senate Order is underpinned by the principle that the Parliament and the public should not be prevented from accessing contract information unless there is a sound reason to do so. Once a contract has been awarded, the terms of the contract including parts of the contract drawn from the supplier’s submission are not confidential unless the entity has determined and identified in the contract that specific information is to be kept confidential. The need for confidentiality in contracts should be assessed on a case-by-case basis and balanced against public accountability requirements. An entity’s assessment of a supplier’s claims against the Confidentiality Test and the reasons for agreeing to the inclusion of confidentiality provisions should be documented.

3.2 To determine whether confidentiality provisions in contracts had been used appropriately and reported correctly, the ANAO examined:

- the reported use of confidentiality provisions in contracts over time based on each entity’s Senate Order listings; and

- the use of confidentiality provisions in a sample of the audited entities’ contracts.

The inclusion of parliamentary disclosure and ANAO access clauses in the sample of contracts were also examined.

The reported use of confidentiality provisions in Australian Government contracts over time

3.3 The unjustified use or incorrect reporting of confidentiality provisions in government contracts can reduce transparency through: preventing the release of contract information; and potentially misinforming the Parliament and the public about government contract information that they can access. A summary of the number and value of contracts and the reported use of confidentiality provisions in entities’ contract listings for the 2011–14 calendar years are provided at Table 3.1.

Table 3.1: Number and value of contracts, and the reported use of confidentiality provisions, as published in entity contract listings 2011–14

|

Number of FMA Act/PGPA Act entities that published a contract listing or advice no relevant contracts had been entered in to(a)

|

93

|

98

|

101

|

92

|

|

Total number of contracts listed

|

39 223

|

42 536

|

30 696

|

41 469

|

|

Total value of contracts listed (billion)

|

$156.5

|

$199.7

|

$189.2

|

$216.3

|

|

Total number of contracts identified as containing confidentiality provisions

|

2 391

|

1 703

|

1 369

|

1 855

|

|

Total value of contracts with identified confidentiality provisions (billion)

|

$21.90

|

$21.87

|

$16.90

|

$30.86

|

|

Percentage of contracts with identified confidentiality provisions

|

6.1

|

4.0

|

4.5

|

4.5

|

Source: ANAO analysis.

Note (a): Number of agencies/entities that had published contract listings for the: 2011 calendar year reporting period as at 30 April 2012; for the 2012 calendar year reporting period as at 1 June 2013; for the 2013 calendar year reporting period as at 14 March 2014; and for 2014 calendar year reporting period as at 27 May 2015.

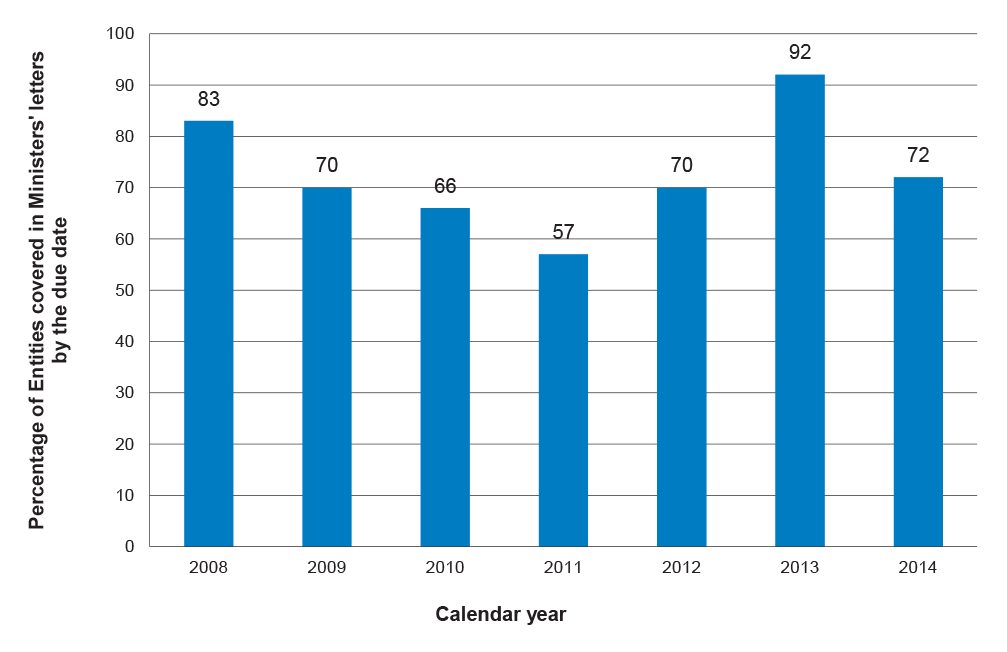

3.4 Across all entities’ contract listings, the proportion of contracts reported to contain confidentiality provisions for the 2014 calendar year has remained low at 4.5 per cent. This is in keeping with the 2013 calendar year reporting period and the broader downward trend since the commencement of the Senate Order, as shown in Figure 3.1. The low level of reported use of confidentiality provisions indicates that scrutiny and accountability of government expenditure is less likely to be impeded by assertions of commercial sensitivity or confidentiality than when the Order was first introduced.

Figure 3.1: Proportion of contracts reported as containing confidentiality provisions: calendar years 2002–14

Source: ANAO analysis of agencies’/entities’ Senate Order contract listings.

Use of confidentiality provisions by audited entities

Types of confidentiality provisions

3.5 There are two types of confidentiality provisions:

- those that make specific information contained in the contract confidential (referred to in the Order as ‘provisions requiring the parties to maintain confidentiality of any of its provisions’; and

- those that protect the confidential information of the parties that may be obtained or generated in carrying out the contract but cannot be specifically identified when the contract is entered into (referred to in the Order as ‘other requirements of confidentiality’).

3.6 Most government contracts contain general confidentiality provisions and entities publish an overarching statement with their Senate Order listing advising of the existence of, and reasons for, the inclusion of such provisions. General confidentiality provisions are not required to be reported where an overarching statement is supplied. Table 3.2 provides examples of the differences between specific and general confidential information.

Table 3.2: Examples of specific and general confidential requirements in contracts

- Price discount information

- Specific contract information, related to statutory secrecy provisions

- Entity security arrangements, including floor plans

- The contractor’s tools, proprietary methodologies and processes

|

- All information and Commonwealth material

- All the entity’s policies, instructions or business strategies

- All pre-existing intellectual property of the contract

- Information or documents that are marked confidential or are by their nature confidential

|

Source: ANAO from audited entities’ contracts.

The appropriate use of confidentiality provisions in a sample of contracts

3.7 To assess the appropriateness of the use of confidentiality provisions for the purposes of this audit the ANAO reviewed a sample of contracts identified as containing confidentiality provisions. In order to undertake this assessment, the ANAO had regard to Finance’s current guidance, Buying for the Australian Government, Confidentiality throughout the Procurement Cycle (the Guidance). The Confidentiality Test outlined in the Guidance establishes four criteria (as shown in Table 3.3), all of which must be met for a supplier’s information to be considered confidential.

Table 3.3: The Confidentiality Test

|

Criterion 1: The information to be protected must be specifically identified

|

|

A request for inclusion of a provision in a contract that states that all information is confidential does not pass this test. Individual items of information, for example pricing, must be separately considered. However, where an entity contract may be used for future cooperative procurements entities generally should not include provisions that would prevent other Commonwealth entities from accessing the terms and conditions, including pricing of the contract.

|

|

Criterion 2: The information must be commercially ‘sensitive’

|

|

The information should not generally be known or ascertainable. The specific information must be commercially ‘sensitive’ and it must not already be in the public domain. A request by a potential supplier to maintain the confidentiality of commercial information would need to show that there is an objective basis for the request and demonstrate that the information is sensitive.

|

|

Criterion 3: Disclosure would cause unreasonable detriment to the owner of the information or another party

|

|

A potential supplier seeking to maintain confidentiality would normally need to identify a real risk of damage to commercial interests flowing from disclosure which would cause unreasonable detriment. For example, disclosure of internet price lists would not harm the owner, but disclosure of pricing information that reveals a potential supplier’s profit margins may be detrimental.

|

|

Criterion 4: The information was provided under an understanding that it would remain confidential

|

|

This requires consideration of the circumstances in which the information was provided and a determination of whether there was a mutual, express or implied understanding that confidentiality would be maintained. The terms included in request documentation and in draft contracts will impact on this. For example, a request for tender and draft contract which included specific confidentiality provisions would support an assertion by a potential supplier that the entity has agreed to accept information on the understanding that it would remain confidential.

|

Source: Finance.

Appropriateness of the use and reporting of confidentiality provisions

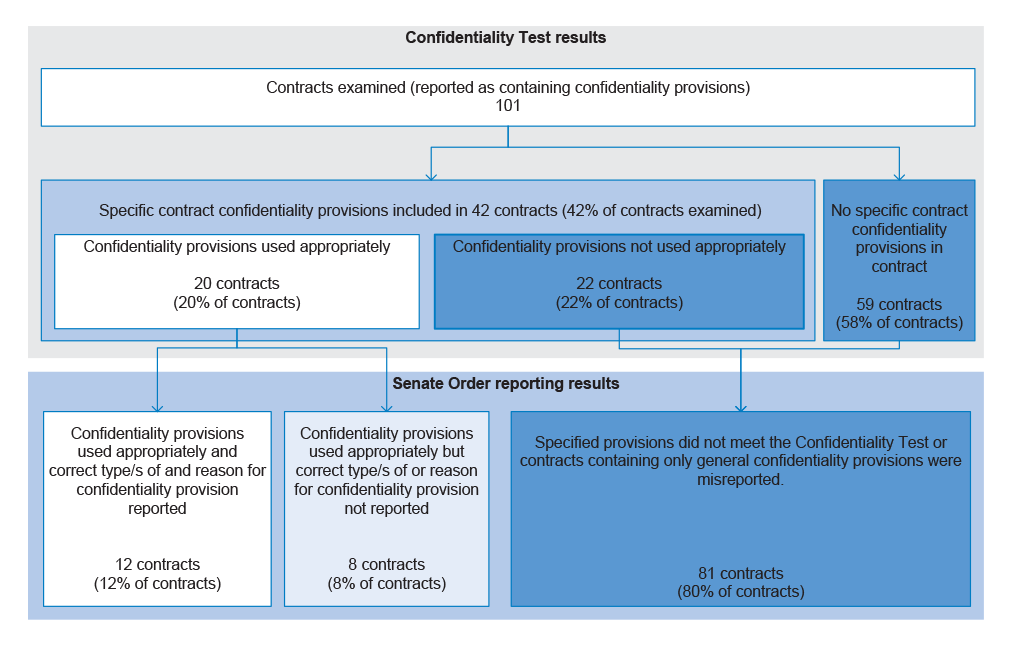

3.8 The ANAO selected a sample of 101 contracts that had been reported by the four audited entities in their contract listings or on AusTender as containing confidentiality provisions. The results of the ANAO’s analysis, based on the application of the Confidentiality Test to the reported confidentiality provisions, are shown in Figure 3.2 and discussed in the following sections of this chapter. Of the 101 contracts examined, 20 per cent used confidentiality provisions appropriately.

Figure 3.2: Contract analysis result: appropriateness of the use and reporting of confidentiality provisions

Source: ANAO analysis. Areas of incorrect reporting and/or use of confidentiality provisions are shown with dark blue shading.

Note: Percentages are rounded.

Confidential information in the contract is specifically identified (Criterion 1 and Criterion 4 of the Confidentiality Test)

3.9 For a contract to be assessed as meeting Criterion 1 of the Test, at least one contract provision must specifically identify the information that is to be protected. However, as shown in Figure 3.2 above, only 42 of the 101 contracts examined contained provisions that specifically identified the information that was to be protected. The remaining 59 contracts were found on ANAO’s examination to have no specific confidentiality provisions that identified information within the contract which was required to remain confidential. Most of the contracts examined were prepared using templates that contained a section to separately list the confidentiality requirements of the contract. Despite the confidentiality requirements section stating ‘nil’, ‘not applicable’ or ‘none specified’, 29 of these 59 contracts had still been reported as containing confidentiality provisions. The remaining 30 contracts either contained only general confidentiality provisions or confidentiality provisions relating to information which was to be obtained or generated as part of the delivery of the contract.

Information is commercially sensitive and would cause detriment if made public (Criterion 2 and Criterion 3 of the Confidentiality Test)

3.10 The Confidentiality Test states that for information to be considered confidential it must be commercially sensitive and the disclosure of the information would cause detriment to the owner of the information or another party. This type of information would not normally be in the public domain. Examples of information that may be included in contracts requiring protection through the use of confidentiality provisions include:

- pricing information that would reveal a supplier’s cost or profit margins;

- unique industrial processes, formulae, product mixes, customer lists, engineering and design drawings and diagrams, and accounting techniques;

- personal information requiring protection under the Privacy Act 1988; and

- information of a nature that should be protected on the basis of public interest or under statutory secrecy provisions.

3.11 The ANAO assessed the 42 contracts (from the sample of 101) which had specifically identified the information to be protected through the use of confidentiality provisions against Criteria 2 and 3 of the Confidentiality Test. Of these 42 contracts, 20 were assessed as meeting Criteria 2 and 3 of the Confidentiality Test. The 22 contracts assessed as not meeting these criteria displayed the following characteristics:

- 14 contracts claimed protection of supplier internal costing/profit information, but the contracts did not contain pricing information which revealed the suppliers’ internal costs or profit margins;

- five contracts claimed protection of intellectual property but did not contain information on particular technical or business solutions that would be considered to constitute intellectual property; and

- three contracts claimed confidentiality under the Privacy Act 1988, but did not contain information of a personal nature as described by the Act.

3.12 The Guidance advises that the entity’s assessment of the supplier’s claims and the reasons for agreeing to the inclusion of confidentiality provisions should be documented. The audited entities were not able to provide documentation supporting their assessment of suppliers’ claims against the Confidentiality Test, and reasons for agreeing for the information to remain confidential. However, in two cases, some discussion of the request from the supplier was captured in tender assessment documents, but did not extend to consideration of the Confidentiality Test, nor was the delegate required to make a decision regarding the inclusion of confidentiality provisions in the contract. In one further case, a procurement advisor provided clear advice about the Confidentiality Test and the need to document the assessment. This advice was provided after the contract was executed and was sought in relation to reporting the contract on AusTender.

Other issues noted with the use of confidentiality provisions

3.13 Nearly half the contracts (48 per cent) in the sample from the four entities stipulated the period of confidentiality as ‘perpetual’, ‘ongoing’, ‘unlimited’, or ‘indefinite’ for either or both contract and contract-related information. According to the Guidance, information should generally not be kept confidential for an unlimited period. At most, the time period should be in line with entities’ records authorities or the general records authorities under the Archives Act 1983.

The role of Department of Finance

3.14 The results of this audit indicate that the guidance on the Confidentiality Test is deficient or its application by individuals undertaking procurement is deficient—confidentiality provisions in 80 per cent of contracts in the sample were inappropriately used or misreported. As noted in paragraph 1.7, entities’ primary reference for confidentiality is the Guidance, however, when undertaking procurement an entity’s first port of call is the Commonwealth Procurement Rules (CPRs). While there are references to the treatment of confidential information within the CPRs, these references are not prominent and could be easily overlooked. Furthermore, there is no direct reference to the Confidentiality Test within the CPRs. Greater prominence needs to be given to the Confidentiality Test in the Commonwealth Procurement Rules and Department of Finance should amend the CPRs to include the Confidentiality Test or refer more directly to the requirement for its use.

3.15 The results also highlight that the audited entities in 2014 had little or no assurance processes to oversight the use of confidentiality provisions. Department of Finance could do more in its role as the procurement policy owner to strengthen current guidance to include examples of entity assurance mechanisms including better practice approaches.

Recommendation No.1

3.16 To improve the appropriate use and reporting of confidentiality provisions in contracts by entities, the ANAO recommends the Department of Finance revises guidance for confidentiality in procurement by including:

- reference to the Confidentiality Test in the Commonwealth Procurement Rules; and

- strengthening current guidance to include examples of entity assurance mechanisms.

Department of Finance response:

3.17 Agreed. As part of the next review of the Commonwealth Procurement Rules, Finance will expand on the reference to the guidance Confidentiality Throughout the Procurement Cycle to note it includes a ‘Confidentiality Test’ and will continue to encourage entities to implement appropriate quality assurance processes when uploading data to AusTender.

Trends in the use of confidentiality provisions

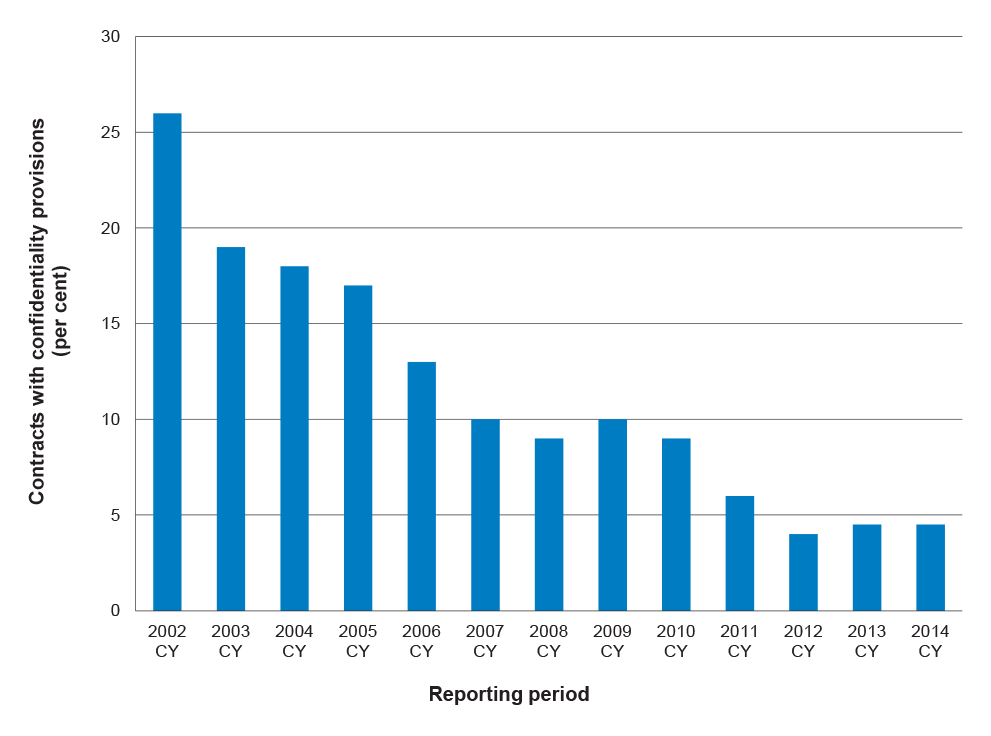

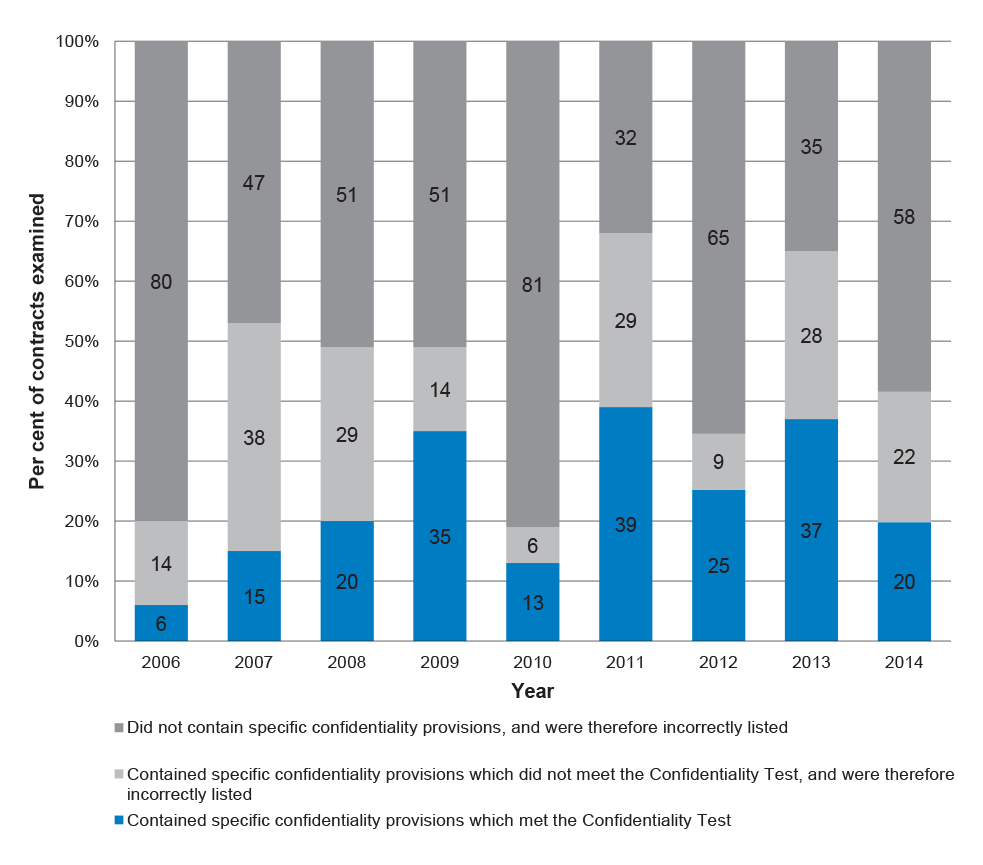

3.18 Each of the ANAO’s audits of the Senate Order since 2006 have identified that fewer than 40 per cent of contracts examined have contained specific confidentiality provisions that met the Confidentiality Test criteria. In 2014, that percentage dropped to 20 per cent. The trends in the use of confidentiality provisions are shown in Figure 3.3.

Figure 3.3: Trends in the appropriate use of confidentiality provisions in contracts over time

Source: ANAO analysis.

Note: Percentages may not add up to 100 per cent due to rounding.

3.19 Transparency in procurement activities is achieved through appropriate reporting of procurement activity, and the use of confidentiality provisions in contracts only where justified. The results of this audit of the Senate Order indicate that there continues to be a high degree of inappropriate use and misreporting by entities of the types of confidentiality provisions and reasons for their use. Errors in application and reporting relate to insufficient assessment of contracts. Suppliers’ claims for contract information to be kept confidential must be assessed against the four criteria of the Confidentiality Test on a case-by-case basis. For the contracts sampled, there were no documented assessments of suppliers’ claims against the Confidentiality Test. Entities need to pay greater attention to this aspect of procurement. Requiring staff to document the assessment of and decisions made in respect to suppliers’ claims for contract information to remain confidential, would assist in this regard.

Recommendation No.2

3.20 When considering requests to keep information contained in a contract confidential, the ANAO recommends that entities implement procedures that require:

- a case-by-case assessment of supplier requests against the Confidentiality Test; and

- adequate documentation of the reasons for agreeing to keep specific information in contracts confidential.

Department of Finance response:

3.21 Agreed. The Confidentiality Test plays an important role in assisting entities in complying with the Senate Order. In addition, Finance supports entities implementing case-by-case assessments of claims of confidentiality and documenting reasons.

Department of the Prime Minister and Cabinet

3.22 Agreed.

Department of Social Services

3.23 Agreed, the Department of Social Services (DSS) has implemented the above recommendations as follows:

(a) DSS guidance on confidentiality has been strengthened to include specific advice and examples by which DSS business areas can make informed decisions on a case by case basis against the Department of Finance ‘Confidentiality Test’; and

(b) The DSS centralised procurement unit (CPU) now reviews proposed reasons for agreeing to keep specific information in contracts confidential for each individual arrangement. The CPU will ensure that documented reasons for agreement are recorded in the procurement IT system.

In addition, the delivery of internal procurement training will assist to strengthen the process by which DSS manage requests to keep contract information confidential.

Department of Veterans’ Affairs

3.24 Agreed. While the Department has procedures in place, it will take measures to ensure the procedures are followed.

Implementation of previous recommendations

3.25 In the 2013 calendar year audit into Senate Order compliance, the ANAO included a recommendation for entities to improve practical support provided to staff to more accurately assess and report on confidentiality provisions in contracts. This recommendation was supported by the results for the Australian Federal Police (AFP) an entity included in the 2013 calendar year sample, which obtained a 100 per cent compliance result for its use of confidentiality provisions. The AFP routinely reviewed the internally reported use of confidentiality provisions by divisions and line areas to determine whether the use of provisions was appropriate and accurately reported.

3.26 All four entities included in the 2014 calendar year audit formally acknowledged the recommendations from the previous ANAO audit through their audit committees. However, the assurances provided to the audit committees were not supported by the results of this audit.

3.27 During the course of the audit, DSS had introduced a quality assurance process to assess the appropriateness of the use of confidentiality provisions and improve record keeping. These new processes should assist DSS to meet Senate Order requirements in the future and are outlined in case study 1.

|

Case study 1

At the commencement of the audit, DSS advised that it had encountered issues with contract reporting, which had led to a high number of contracts being reported as containing confidentiality provisions. DSS’ procurement processes at the time were supported by an IT system that allowed the central procurement unit to review key points in the procurement process. During the audit, DSS introduced a new quality assurance review point to identify when staff undertaking procurement intend to include specific confidentiality provisions within contracts. The review point involved the procurement IT system sending an alert to the central procurement unit. The unit then provided oversight and advice in relation to any confidentiality provisions before the contract was executed or a purchase order raised.

|

Parliamentary disclosure and ANAO access clauses

3.28 In entering into a contract, the Australian Government cannot provide an absolute guarantee of confidentiality. This is due to a number of obligations whereby the Government is required to disclose information, regardless of any contractual obligations to maintain confidentiality. These may include disclosure of information consistent with the Freedom of Information Act 1982 or disclosure of discoverable information that is relevant to a case before a court. In addition, entities may be required to facilitate the disclosure of, or access to, contractual information by the Parliament, its committees, and the Auditor-General to comply with accountability obligations. Accordingly, Australian Government contracts should contain clauses that provide, regardless of contract confidentiality, for:

- disclosure of contract‐related information to the Parliament or parliamentary committees; and

- access by the ANAO to a contractor’s records and premises.

3.29 Of the 101 contracts examined by the ANAO, 98 per cent contained appropriately worded parliamentary disclosure clauses, and 97 per cent included ANAO access clauses (see Table 3.4).

Table 3.4: Parliamentary and ANAO access clauses

|

Finance

|

30

|

28

|

93

|

27

|

90

|

|

PM&C

|

17

|

17

|

100

|

17

|

100

|

|

DSS

|

45

|

45

|

100

|

45

|

100

|

|

DVA

|

9

|

9

|

100

|

9

|

100

|

|

Total

|

101

|

98

|

97

|

97

|

96

|

Source: ANAO analysis.

3.30 All four of the audited entities’ standard contract templates contained appropriately worded parliamentary disclosure clauses and ANAO access clauses. Consistent with the findings of previous ANAO audits, where disclosure clauses were not included in the contracts examined, the entity’s standard contract template had generally not been used. There can be various reasons entities may use non-standard contract templates. However, entities should have in place procedures and guidance to make certain that disclosure and, where appropriate, access clauses are included in the contract terms and conditions of all contracts issued.

Conclusion

3.31 The proportion of contracts reported as containing confidentiality provisions in the 2014 calendar year across all non-corporate Commonwealth entities was low (4.5 per cent) and in keeping with 2013 levels. Despite this, specific confidentiality provisions in contracts have continued to be incorrectly used and reported. For example, in 80 per cent of the contracts sampled by the ANAO, the use of confidentiality provisions did not comply with the Guidance or was misreported.

3.32 Confidentiality provisions in government contracts can impede accountability and transparency in government purchasing. A request for specific information to be kept confidential must be assessed against the Confidentiality Test criteria and entities should make sure decisions to include confidentiality provisions are documented. Entities should also provide adequate training and oversight of this activity.

3.33 Finance supports entities to comply with the Senate Order, however the result of this audit indicate that more support is required to improve entity performance with respect to assessing and reporting on the use of confidentiality provisions. Finance should improve procurement guidance through placing direct reference to the Confidentiality Test within the Commonwealth Procurement Rules. Finance should also clarify and strengthen current guidance to include examples of entity assurance mechanisms, including better practice approaches.