Browse our range of reports and publications including performance and financial statement audit reports, assurance review reports, information reports and annual reports.

Auditor-General Report No. 22 of 2024–25

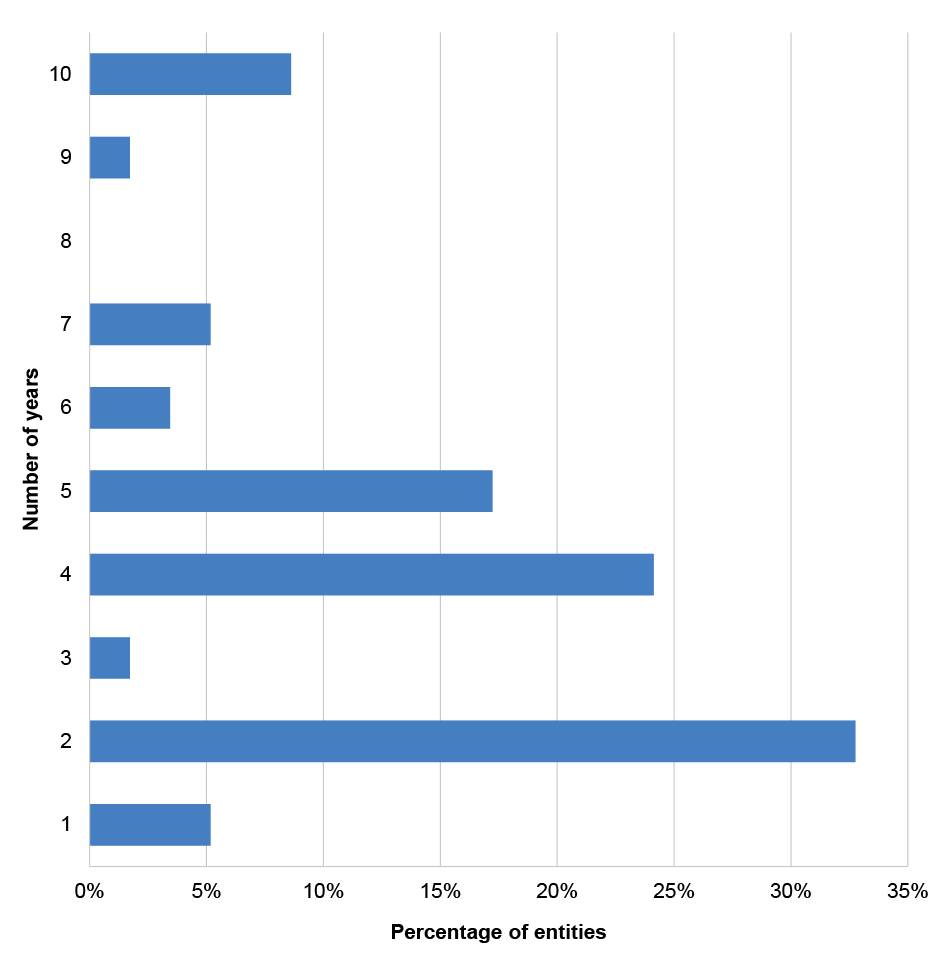

Audits of the Financial Statements of Australian Government Entities for the Period Ended 30 June 2024

Published

Thursday 6 February 2025

Portfolio

Across Entities

Entity

Across Entities

Contact

Please direct enquiries through our contact page.

This report complements the Interim Report on Key Financial Controls of Major Entities financial statement audit report published in June 2024. It provides a summary of the final results of the audits of the Consolidated Financial Statements for the Australian Government and the financial statements of Australian Government entities for the period ended 30 June 2024.

Executive summary

The Australian National Audit Office (ANAO) publishes an annual audit work program (AAWP) which reflects the audit strategy and deliverables for the forward year. The purpose of the AAWP is to inform the Parliament, the public, and government sector entities of the planned audit coverage for the Australian Government sector by way of financial statements audits, performance audits, performance statements audits and other assurance activities. As set out in the AAWP, the ANAO prepares two reports annually that, drawing on information collected during financial statements audits, provide insights at a point in time of financial statements risks, governance arrangements and internal control frameworks of Commonwealth entities. These reports provide Parliament with an independent examination of the financial accounting and reporting of public sector entities.

These reports explain how entities’ internal control frameworks are critical to executing an efficient and effective audit and underpin an entity’s capacity to transparently discharge its duties and obligations under the Public Governance, Performance and Accountability Act 2013 (PGPA Act). Deficiencies identified during audits that pose either a significant or moderate risk to an entity’s ability to prepare financial statements free from material misstatement are reported.

This report presents the final results of the 2023–24 audits of the Australian Government’s Consolidated Financial Statements (CFS) and 245 Australian Government entities. The Auditor-General Report No. 42 2023–24 Interim Report on Key Financial Controls of Major Entities, focused on the interim results of the audits of 27 of these entities.

Consolidated financial statements

Audit results

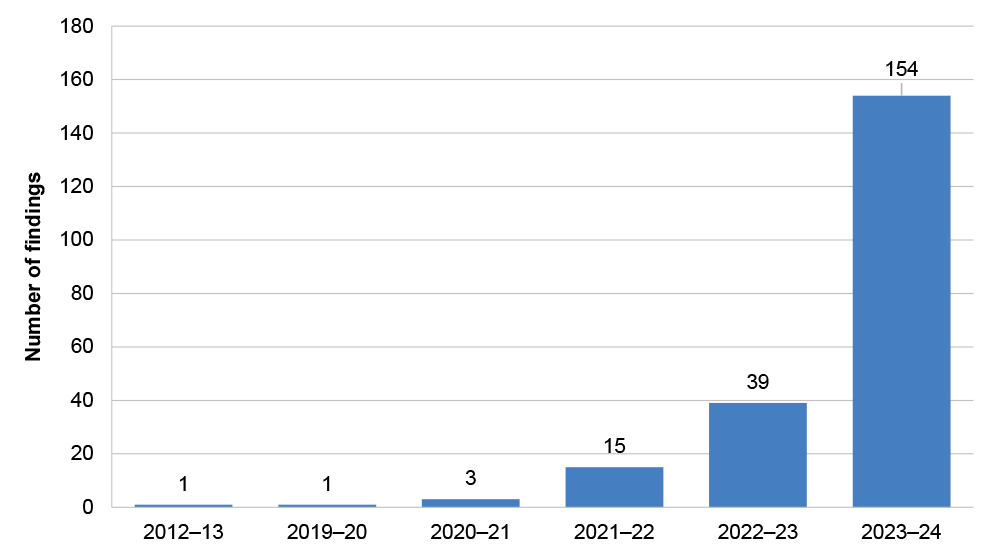

1. The CFS presents the whole of government and the General Government Sector financial statements. The 2023–24 CFS were signed by the Minister for Finance on 28 November 2024 and an unmodified auditor’s report was issued on 2 December 2024.

2. There were no significant or moderate audit issues identified in the audit of the CFS in 2023–24 or 2022–23.

Australian Government financial position

3. The Australian Government reported a net operating balance of a surplus of $10.0 billion ($24.9 billion surplus in 2022–23). The Australian Government’s net worth deficiency decreased from $570.3 billion in 2022–23 to $567.5 billion in 2023–24 (see paragraphs 1.8 to 1.26).

Financial audit results and other matters

Quality and timeliness of financial statements preparation

4. The ANAO issued 240 unmodified auditor’s reports as at 9 December 2024. The financial statements were finalised and auditor’s reports issued for 79 per cent (2022–23: 91 per cent) of entities within three months of financial year-end. The decrease in timeliness of auditor’s reports reflects an increase in the number of audit findings and legislative breaches identified by the ANAO, as well as limitations on the available resources within the ANAO in order to undertake additional audit procedures in response to these findings

5. A quality financial statements preparation process will reduce the risk of inaccurate or unreliable reporting. Seventy-one per cent of entities delivered financial statements in line with an agreed timetable (2022–23: 72 per cent). The total number of adjusted and unadjusted audit differences decreased during 2023–24, although 38 per cent of audit differences remained unadjusted. The quantity and value of adjusted and unadjusted audit differences indicate there remains an opportunity for entities to improve quality assurance over financial statements preparation processes (see paragraphs 2.138 to 2.154).

Timeliness of financial reporting

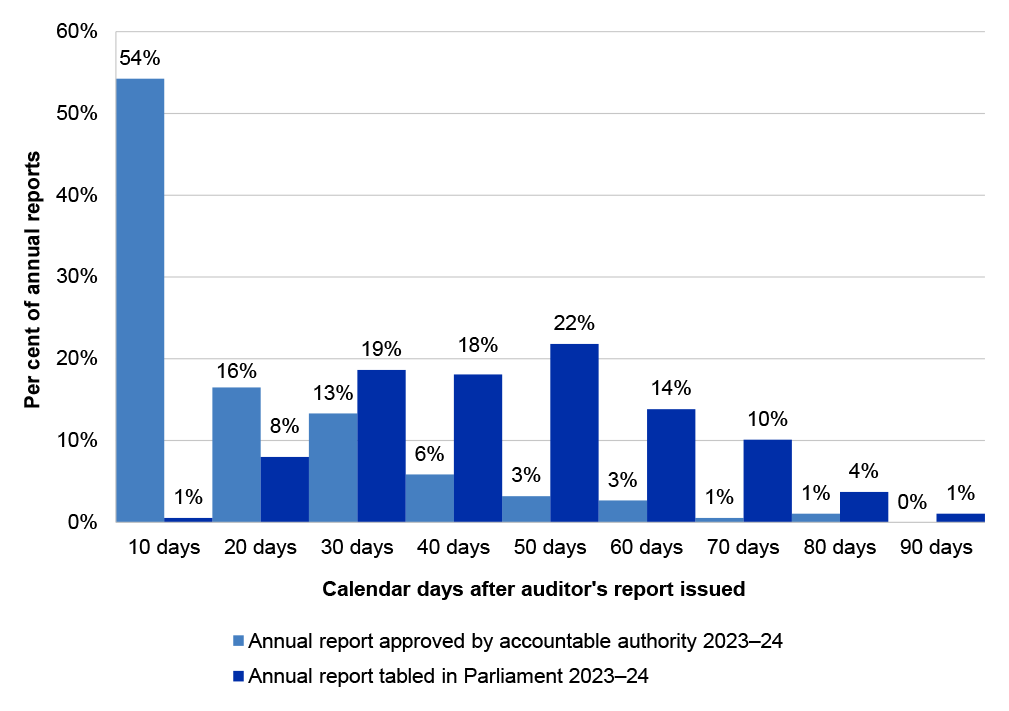

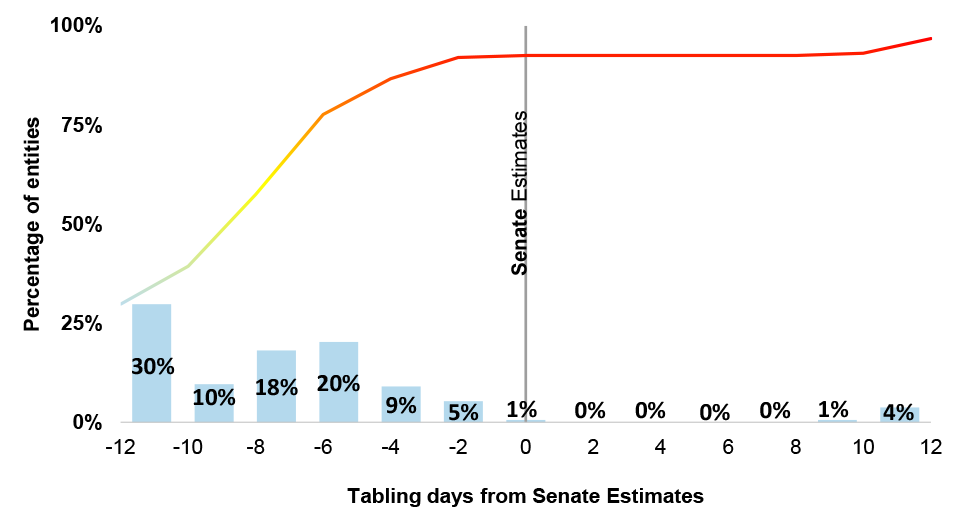

6. Annual reports that are not tabled in a timely manner before budget supplementary estimates hearings decrease the opportunity for the Senate to scrutinise an entity’s performance. Timeliness of tabling of entity annual reports improved. Ninety-three per cent (2022–23: 66 per cent) of entities that are required to table an annual report in Parliament tabled prior to the date that the portfolio’s supplementary budget estimates hearing commenced. Supplementary estimates hearings were held one week later in 2023–24 than in 2022–23. Fifty-seven per cent of entities tabled annual reports one week or more before the hearing (2022–23: 12 per cent). Of the entities required to table an annual report, 4 per cent (2022–23: 6 per cent) had not tabled an annual report as at 9 December 2024 (see paragraphs 2.155 to 2.166).

Official hospitality

7. Eighty-one per cent of entities permit the provision of hospitality and the majority have policies, procedures or guidance in place. Expenditure on the provision of hospitality for the period 2020–21 to 2023–24 was $70.0 million. Official hospitality involves the provision of public resources to persons other than officials of an entity to achieve the entity’s objectives. Entities that provide official hospitality should have policies, and guidance in place which clearly set expectations for officials. There are no mandatory requirements for entities in managing the provision of hospitality, however, the Department of Finance (Finance) does provide some guidance to entities in model accountable authority instructions. Of those entities that permit hospitality 83 per cent have established formal policies, guidelines or processes.

8. Entities with higher levels of exposure to the provision of official hospitality could give further consideration to implementing or enhancing compliance and reporting arrangements. Seventy-four per cent of entities included compliance requirements in their policies, procedures or guidance which support entity’s obtaining assurance over the conduct of official hospitality. Compliance processes included acquittals, formal reporting, attestations from officials and/or periodic internal audits. Thirty-one per cent of entities had established formal reporting on provision of official hospitality within their entities (see paragraphs 2.36 to 2.56).

Artificial intelligence

9. Fifty-six entities used artificial intelligence (AI) in their operations during 2023–24 (2022–23: 27 entities). Most of these entities had adopted AI for research and development activities, IT systems administration and data and reporting.

10. During 2023–24, 64 per cent of entities that used AI had also established internal policies governing the use of AI (2022–23: 44 per cent). Twenty-seven per cent of entities had established internal policies regarding assurance over AI use. An absence of governance frameworks for managing the use of emerging technologies could increase the risk of unintended consequences. In September 2024, the Digital Transformation Agency (DTA) released the Policy for the responsible use of AI in government, which establishes requirements for accountability and transparency on the use of AI within entities (see paragraphs 2.67 to 2.71).

Cloud computing

11. Assurance over effectiveness of cloud computing arrangements (CCA) could be improved. During 2023–24, 89 per cent of entities used CCAs as part of the delivery model for the IT environment, primarily software-as-a-service (SaaS) arrangements. A Service Organisation Controls (SOC) certificate provides assurance over the implementation, design and operating effectiveness of controls included in contracts, including security, privacy, process integrity and availability. Eighty-two per cent of entities did not have in place a formal policy or procedure which would require the formal review and consideration of a SOC certificate.

12. In the absence of a formal process for obtaining and reviewing SOC certificates, there is a risk that deficiencies in controls at a service provider are not identified, mitigated or addressed in a timely manner (see paragraphs 2.57 to 2.66).

Audit committee member rotation

13. Audit committee member rotation considerations could be enhanced. The rotation of audit committee membership is not mandated, though guidance to the sector indicates that rotation of members allows for a flow of new skills and talent through committees, supporting objectivity. Forty-six per cent of entities did not have a policy requirement for audit committee member rotation.

14. Entities could enhance the effectiveness of their audit committees by adopting a formal process for rotation of audit committee membership, which balances the need for continuity and objectivity of membership (see paragraphs 2.16 to 2.21).

Fraud framework requirements

15. The Commonwealth Fraud Control Framework 2017 encourages entities to conduct fraud risk assessments at least every two years and entities responsible for activities with a high fraud risk may assess risk more frequently. All entities had in place a fraud control plan. Ninety-seven per cent of entities had conducted a fraud risk assessment within the last two years. Changes to the framework which occurred on 1 July 2024 requires entities to expand plans to take account of preventing, detecting and dealing with corruption, as well as periodically examining the effectiveness of internal controls (see paragraphs 2.16 to 2.21).

Summary of audit findings

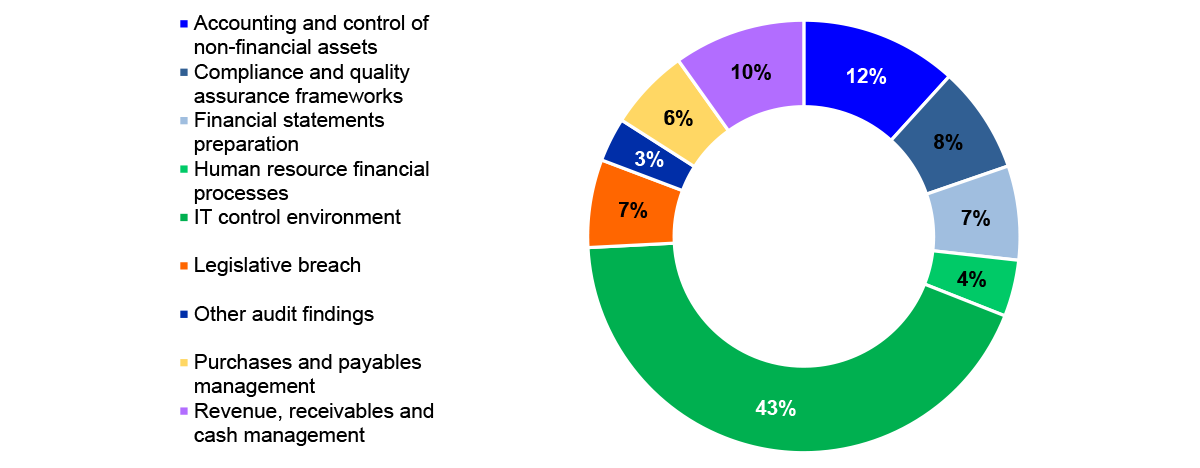

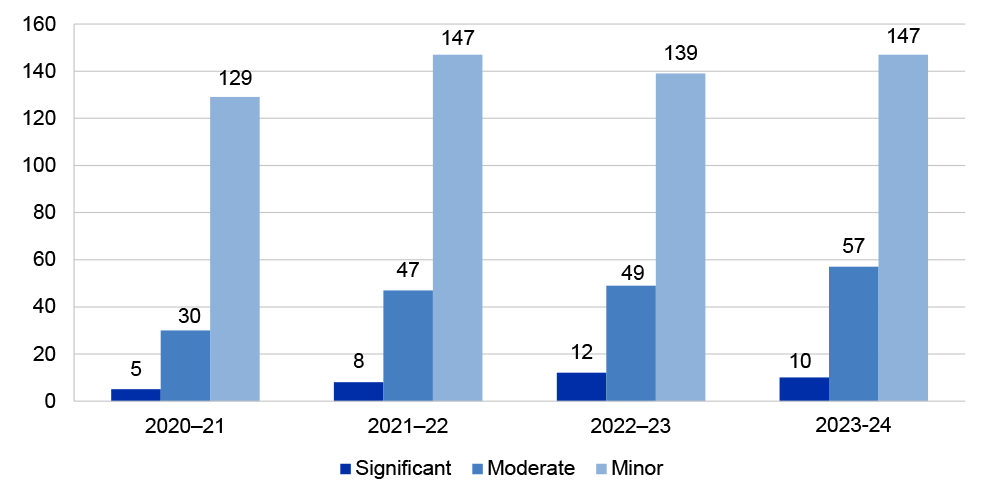

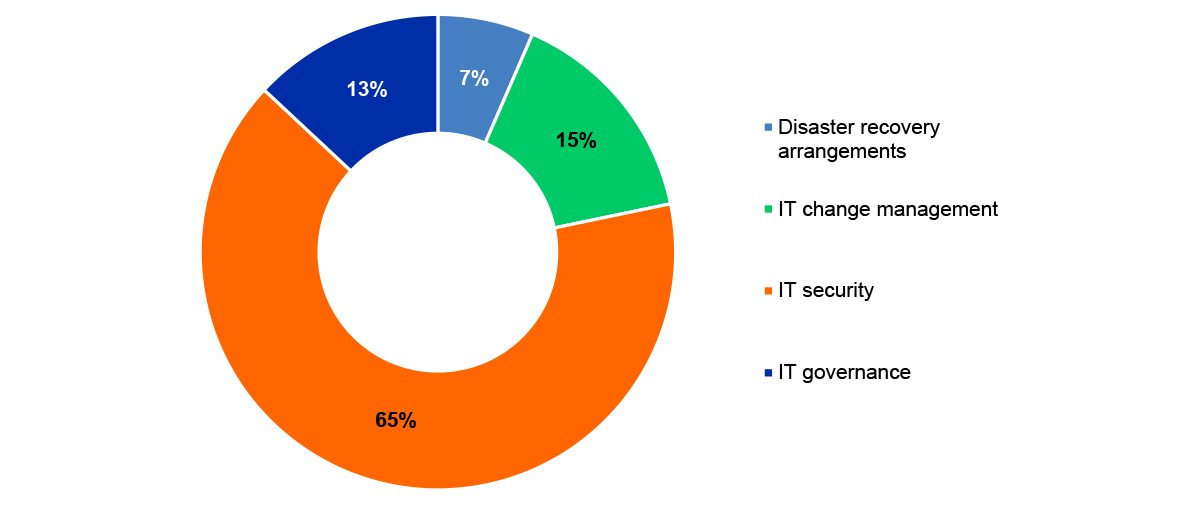

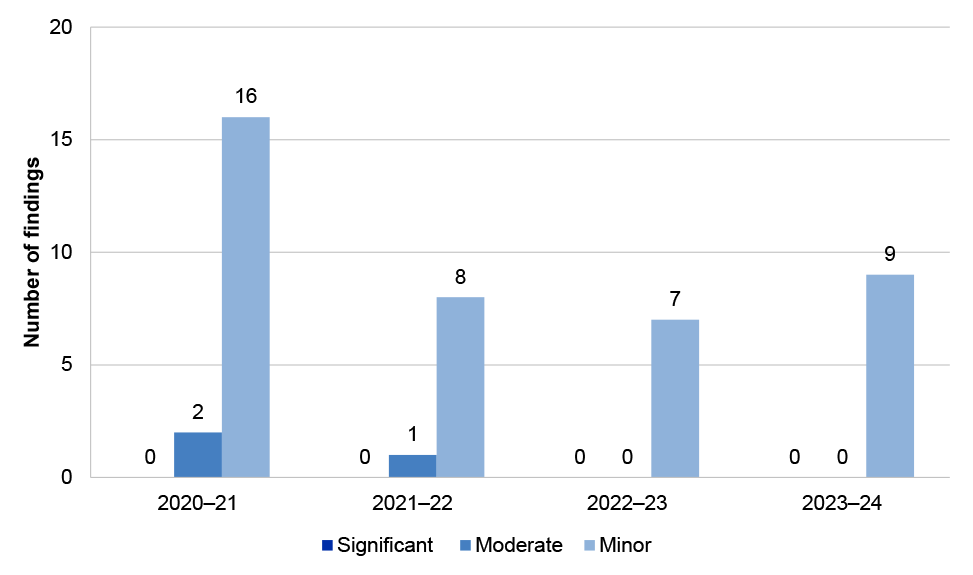

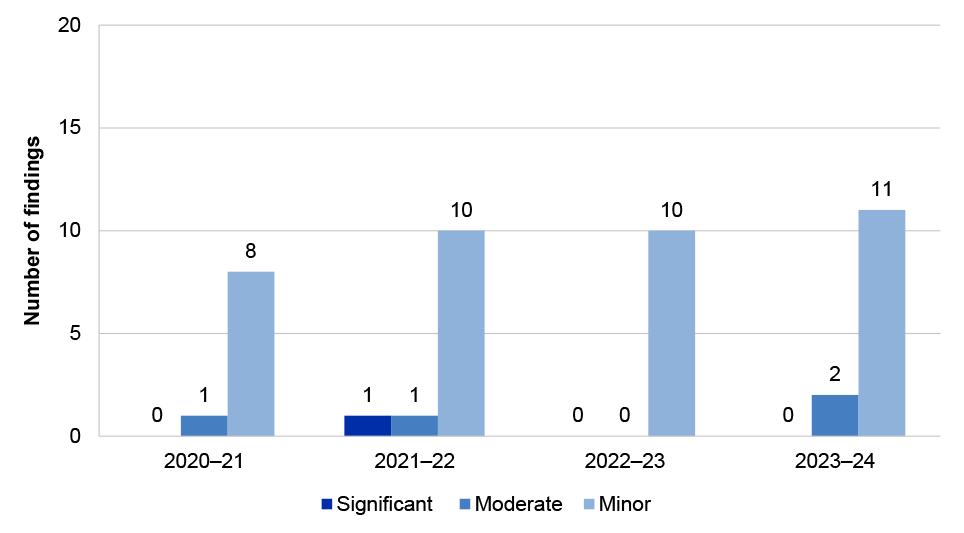

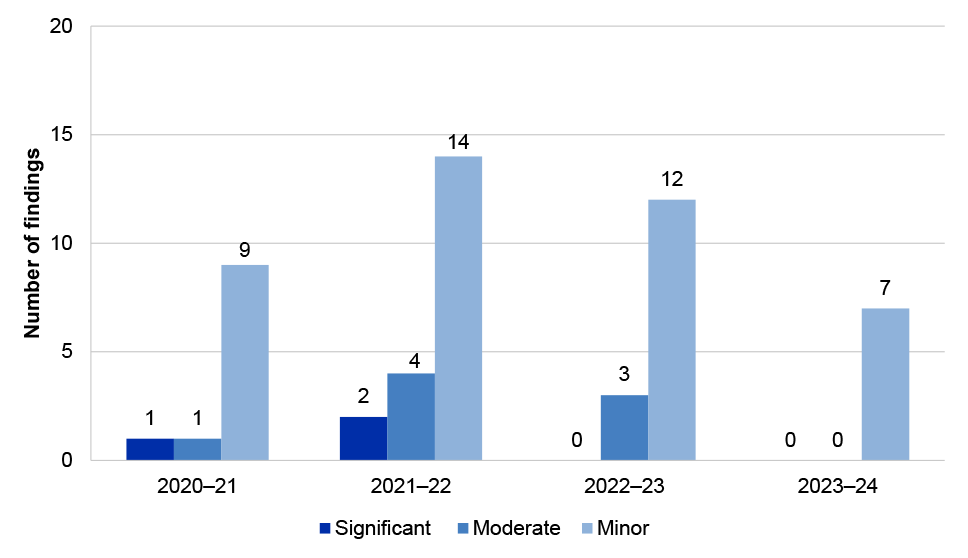

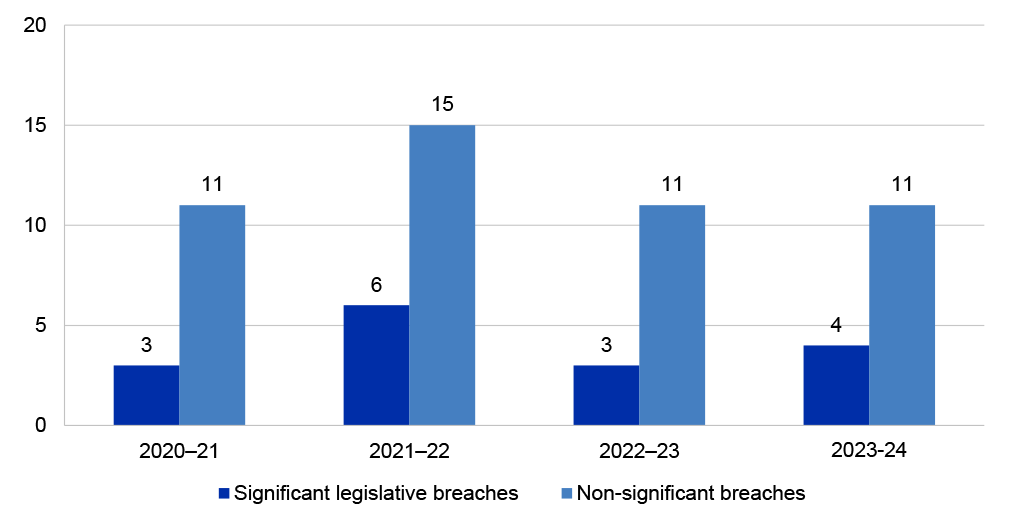

16. Internal controls largely supported the preparation of financial statements free from material misstatement. However, the number of audit findings identified by the ANAO has increased from 2023–24. A total of 214 audit findings and legislative breaches were reported to entities as a result of the 2023–24 financial statements audits. These comprised six significant, 46 moderate, 147 minor audit findings and 15 legislative breaches. The highest number of findings are in the categories of:

- IT control environment, including security, change management and user access;

- compliance and quality assurance frameworks, including legal conformance; and

- accounting and control of non-financial assets.

17. IT controls remain a key issue. Forty-three per cent of all audit findings identified by the ANAO related to the IT control environment, particularly IT security. Weaknesses in controls in this area can expose entities to an increased risk of unauthorised access to systems and data, or data leakage. The number of IT findings identified by the ANAO indicate that there remains room for improvement across the sector to enhance governance processes supporting the design, implementation and operating effectiveness of controls.

18. These audits findings included four significant legislative breaches, one of which was first identified since 2012–13. The majority (53 per cent) of other legislative breaches relate to incorrect payments of remuneration to key management personnel and/or non-compliance with determinations made by the Remuneration Tribunal. Entities could take further steps to enhance governance supporting remuneration to prevent non-compliance or incorrect payments from occurring (see paragraphs 2.72 to 2.137).

Financial sustainability

19. An assessment of an entity’s financial sustainability can provide an indication of financial management issues or signal a risk that the entity will require additional or refocused funding. The ANAO’s analysis concluded that the financial sustainability of the majority of entities was not at risk (see paragraphs 2.167 to 2.196).

Reporting and auditing frameworks

Changes to the Australian public sector reporting framework

20. The development of a climate-related reporting framework and assurance regime in Australia continues to progress. ANAO consultation with Finance to establish an assurance and verification regime for the Commonwealth Climate Disclosure (CCD) reform is ongoing (see paragraphs 3.20 to 3.24).

21. Emerging technologies (including AI) present opportunities for innovation and efficiency in operations by entities. However, rapid developments and associated risks highlight the need for Accountable Authorities to implement effective governance arrangements when adopting these technologies. The ANAO is incorporating consideration of risks relating to the use of emerging technologies, including AI, into audit planning processes to provide Parliament with assurance regarding the use of AI by the Australian Government (see paragraphs 3.25 to 3.33).

22. The ANAO Audit Quality Report 2023–24 was published on 1 November 2024. The report demonstrates the evaluation of the design, implementation and operating effectiveness of the ANAO’s Quality Management Framework and achievement of ANAO quality objectives (see paragraphs 3.34 to 3.39).

23. The ANAO Integrity Report 2023–24 and the ANAO Integrity Framework 2024–25 were also published on 1 November 2024 to provide transparency of the measures undertaken to maintain a high integrity culture within the ANAO (see paragraphs 3.44 to 3.46).

Cost of this report

24. The cost to the ANAO of producing this report is approximately $445,000.

1. The Consolidated Financial Statements

Chapter coverage

This chapter outlines the results of the audit of the Consolidated Financial Statements (CFS) of the Australian Government, which includes the Whole of Government (Australian Government) and the General Government Sector (GGS) financial statements for the year ended 30 June 2024.

This chapter also includes:

- the Key Audit Matters (KAM) reported for the Australian Government;

- an analysis of the Australian Government’s financial outcome and financial position; and

- an analysis of other matters identified during the audit of the CFS.

Audit results

The 2023–24 CFS was signed by the Minister for Finance on 28 November 2024 and the Auditor-General’s unmodified auditor’s report was issued on 2 December 2024.

There were no significant or moderate audit findings identified in the audit of the CFS in 2022–23 or 2023–24.

The Australian Government reported a net operating balance of a surplus of $10.0 billion ($24.9 billion surplus in 2022–23). The surplus has contracted because of growth in expenses that have outgrown taxation revenue. Revenue grew by $37.3 billion (5.4 per cent) while expenses grew by $52.1 billion (7.8 per cent).

The Australian Government’s net worth deficiency decreased from $570.3 billion in 2022–23 to $567.5 billion in 2023–24 mainly due to the impact of favourable gains on investments and liabilities as a result of changes in valuation inputs.

Background

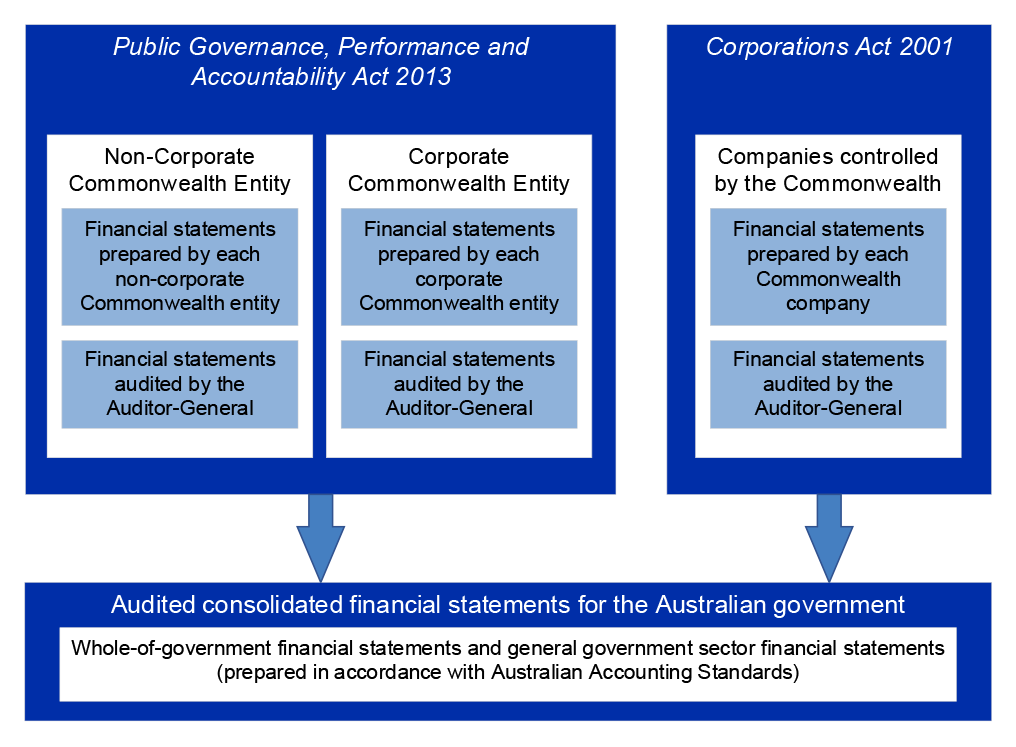

1.1 Government accountability and transparency is supported by the preparation and audit of the Australian Government’s CFS. The CFS and the associated financial analysis provide information to assist users in assessing the financial performance and position of the Australian Government. The CFS is prepared by the Department of Finance (Finance) and issued by the Minister for Finance.

1.2 The CFS presents the consolidated whole of government financial results which includes the results of all Australian Government controlled entities, as well as the GGS financial statements. The 2023–24 CFS is prepared in accordance with section 48 of the Public Governance, Performance and Accountability Act 2013 (PGPA Act) and the requirements of the Australian Accounting Standards, particularly AASB 1049 Whole of Government and General Government Sector Financial Reporting (AASB 1049).

1.3 AASB 1049 requires, with limited exceptions, the principles and rules in the Australian Bureau of Statistics’ Government Finance Statistics (GFS) Manual to be applied in the preparation of the CFS where compliance with the GFS Manual would not conflict with Australian Accounting Standards.

Key areas of financial statements risk

1.4 The ANAO’s 2023–24 audit approach identified four key areas of financial statements risk that had the potential to impact the Australian Government and which were considered Key Audit Matters (KAM).

Table 1.1: Key areas of financial statements risk

|

Relevant financial statements line itema |

Key areas of risk |

Factors contributing to the risk assessment |

|

Taxation revenue $649.4 billion Australian Taxation Office |

Higher Accuracy of taxation revenue KAM |

|

|

Superannuation liabilitiesb $308.5 billion Department of Defence Department of Finance |

Higher Valuation of superannuation liabilities KAM |

|

|

Specialist Military Equipment (SME) $88.6 billion Department of Defence Other plant, equipment and infrastructure $88.3 billion Numerous entities |

Moderate Valuation of specialist military equipment and other plant, equipment and infrastructure assets KAM |

|

|

Australian Government Securities $611.0 billion Australian Office of Financial Management (AOFM) |

Moderate Valuation and disclosure of Australian Government Securities KAM |

|

Note: For 2023–24, the ‘accuracy and occurrence of personal benefits expense’ and the ‘valuation of collective investment vehicles’ are no longer considered key audit matters compared to the prior year.

Note a: Figures presented in Table 1.1 may differ from the financial statements of individual entities because of eliminations and adjustments at the CFS level or where the entities identified contribute a majority to the balance of the financial statements line item.

Note b: These are the main government entities responsible for administration and reporting of Australian Government superannuation liabilities. Liabilities also include schemes managed by other entities, such as the Australian Postal Corporation.

Source: ANAO 2023–24 audit results, and the CFS for the year ended 30 June 2024.

Audit results

1.5 The 2023–24 CFS was signed by the Minister for Finance on 28 November 2024 and the Auditor-General’s unmodified auditor’s report was issued on 2 December 2024.

1.6 There were no unadjusted audit differences in 2022–23 or 2023–24.

1.7 There were no significant or moderate audit findings arising from the 2022–23 or 2023–24 financial statements audits of the CFS. Table 1.2 presents a summary of the total number of unresolved findings at the conclusion of the 2023–24 final audit.

Table 1.2: Unresolved audit findings

|

Entity |

Significant |

Moderate |

Minor |

Total |

|

Consolidated Financial Statements |

– |

– |

3 |

3 |

Source: ANAO 2023–24 audit results.

Australian Government’s financial outcome

1.8 The following provides analysis of key financial balances for the Australian Government.

Operating result

1.9 The following key financial measures were reported for 2023–24:

- net operating balance was a surplus of $10.0 billion (compared to a surplus of $24.9 billion in 2022–23);

- operating result was a deficit of $20.1 billion (compared to a surplus of $13.2 billion in 2022–23); and

- comprehensive result (change in net worth) was an increase in net worth of $2.8 billion (compared to an increase of $38.4 billion in 2022–23).

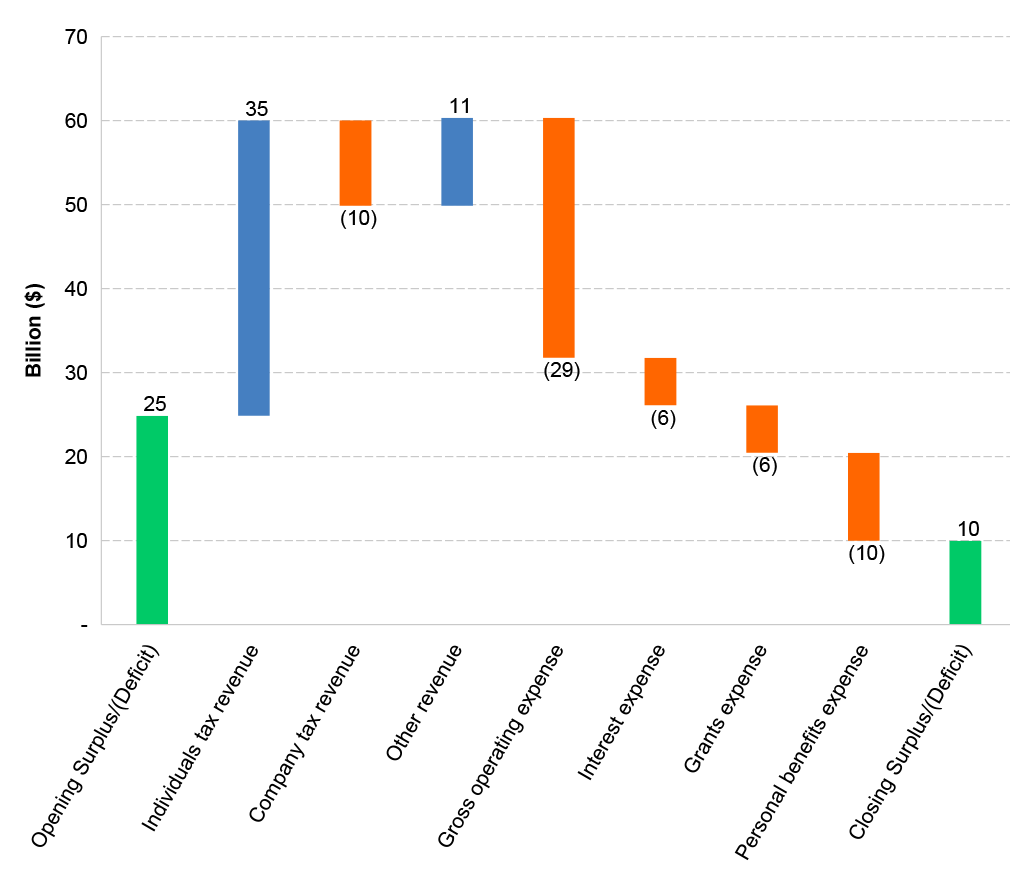

1.10 Figure 1.1 presents the changes in the Australian Government’s net operating balance from 1 July 2023 to 30 June 2024.

Figure 1.1: Changes in the Australian Government’s net operating balance from 1 July 2023 to 30 June 2024

Source: ANAO analysis of the 2023–24 CFS.

1.11 Table 1.3 provides commentary on the main contributors to the change in net operating balance of the Australian Government identified in Figure 1.1.

Table 1.3: Explanation of key movements in net operating balance

|

Relevant financial statements line item |

Explanation for key movements in net operating balance |

|

Individuals tax revenue |

There has been a $35.2 billion increase in individual taxation revenue as a result of growth in employment, wages and capital gains. |

|

Company tax revenue |

Company income tax revenue decreased by $10.2 billion across various industries, particularly the mining sector due to lower commodity prices during the year. |

|

Other revenue |

Other revenue has increased by $10.5 billion as a result of:

|

|

Gross operating expense |

Gross operating expense has increased by $28.6 billion primarily as a result of:

|

|

Interest expense |

Interest expense has increased by $5.7 billion mainly driven by higher average annual interest rate in the current year compared to the prior year. |

|

Grants expense |

Grants expenses has increased by $5.6 billion mainly due to the increase in GST revenue redistribution to the States and Territories. |

|

Personal benefits expense |

Personal benefits have increased by $10.4 billion as a result of the following partially offsetting factors:

|

Source: ANAO analysis of 2023–24 CFS.

Classification of expenses by the functions of Government

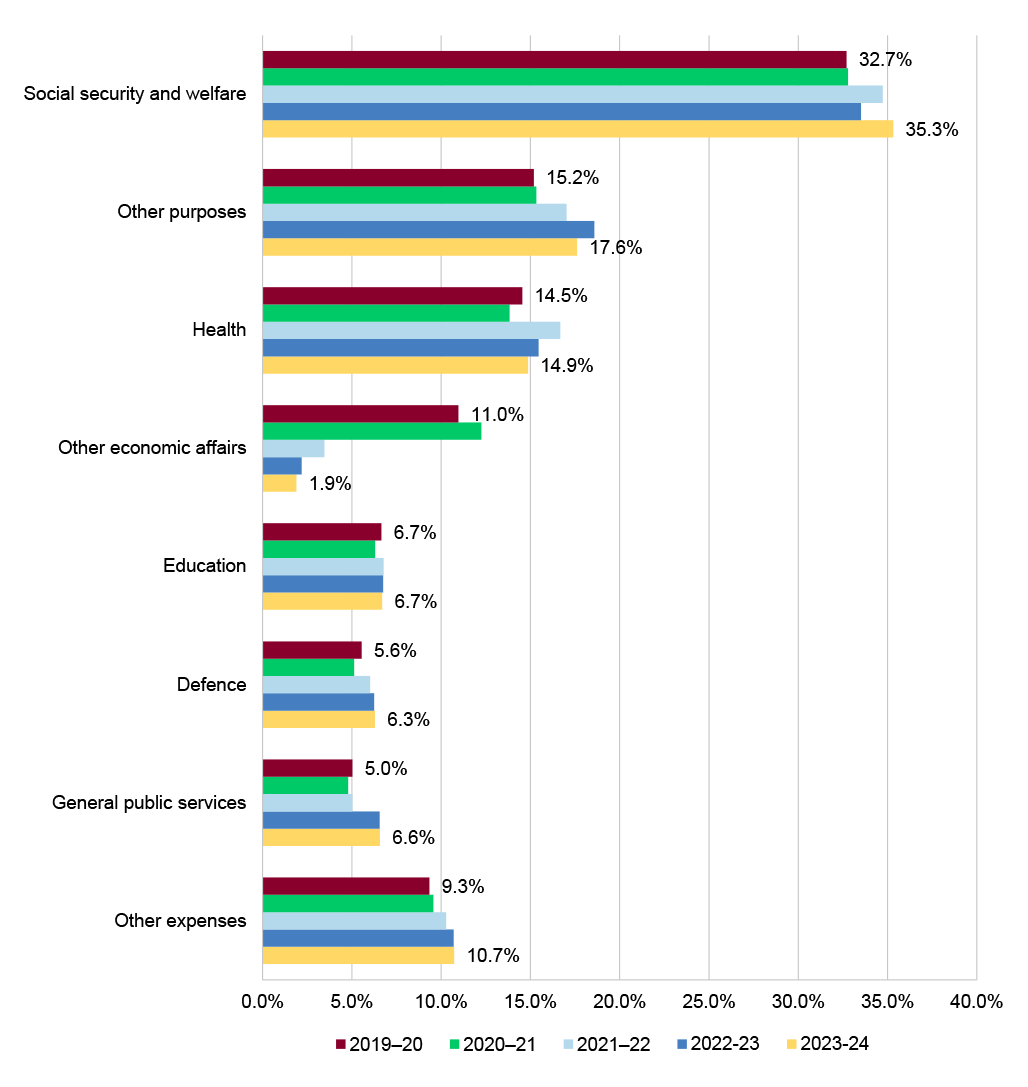

1.12 Figure 1.2 provides an analysis of the Australian Government’s expenses by function from 1 July 2019 to 30 June 2024. As a percentage of total expenses, each function has remained stable during this period, except for:

- ‘Other economic affairs’: During 2019–20 and 2020–21 the ‘Other economic affairs’ function included higher expenses related to the JobKeeper and cashflow boost payments which supported businesses and individuals impacted by the effects of the COVID-19 pandemic. The percentage of expenditure returned to pre-pandemic levels by 2022–23;

- ‘Other purposes’: This function consists of the General Revenue Assistance payments to the states and territories for their share in GST. These payments were reduced over the COVID-19 pandemic period as consumption declined and have returned to pre-pandemic levels in 2023–24; and

- ‘General public services’: These expenses have increased in 2022–23 and 2023–24 because the Reserve Bank of Australia (RBA) is paying more interest in its exchange settlement accounts as a result of higher interest rates over the period.

Figure 1.2: Proportion of expenses of Government by function from 2019–20 to 2023–24

Notes: The ‘Other purposes’ function includes public debt transactions, general purpose inter-government transactions, natural disaster relief and grants to and through state and territory governments.

The ‘Other economic affairs’ function represents non-standard payments including storage, tourism promotion, labour market assistance to industry and industrial relations.

‘Other expenses’ includes payments to: agriculture, forestry and fishing; fuel and energy; housing and community amenities; mining, manufacturing and construction; public order and safety; recreation and culture; transport and communications.

Source: ANAO analysis of the CFS from 2019–20 to 2023–24.

Australian Government’s financial position

Net worth

Changes in the Australian Government’s net worth from 1 July 2023 to 30 June 2024

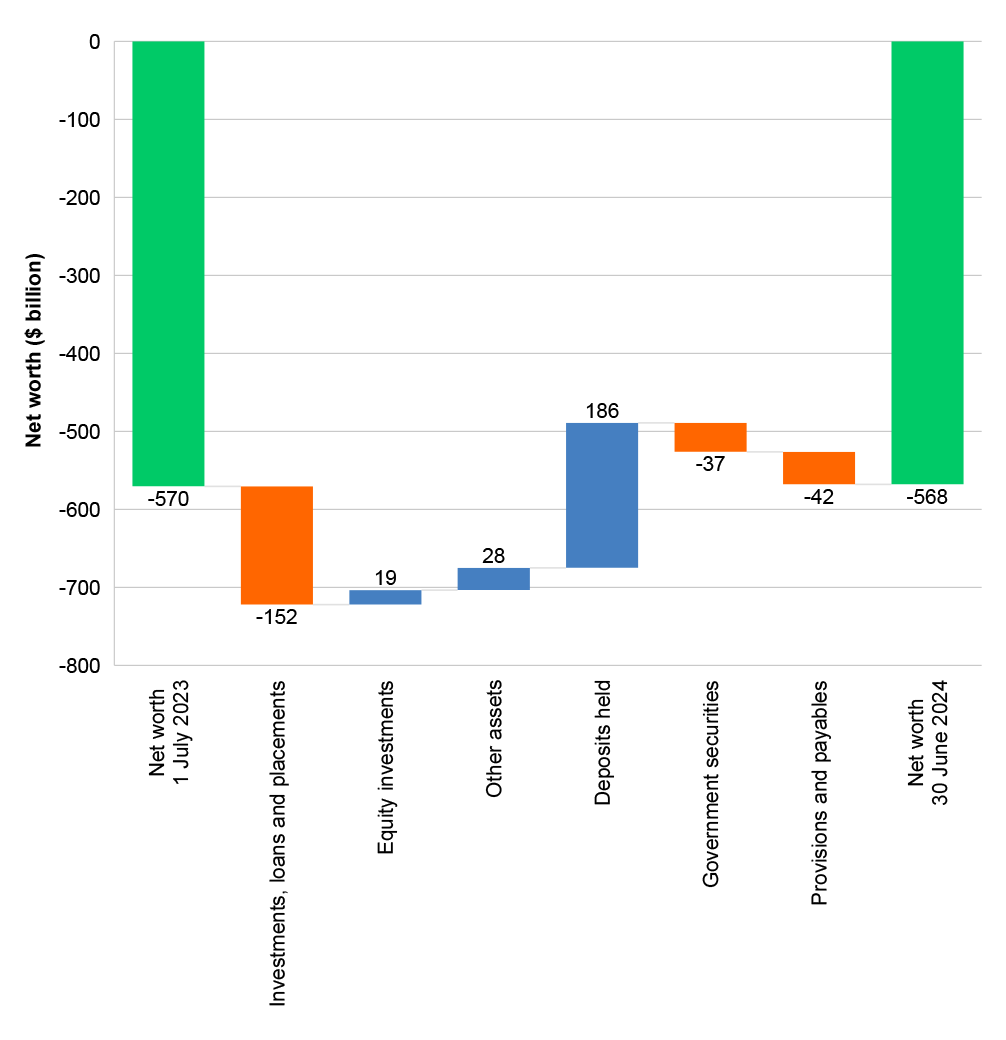

1.13 The Australian Government’s net worth deficiency reduced from $570.3 billion in 2022–23 to $567.5 billion in 2023–24. Figure 1.3 provides an analysis of the movement in net worth from 1 July 2023 to 30 June 2024.

Figure 1.3: Changes in the Australian Government’s net worth from 1 July 2023 to 30 June 2024

Source: ANAO analysis of the 2023–24 CFS.

1.14 Table 1.4 provides commentary on the main contributors to the change in net worth of the Australian Government identified in Figure 1.3.

Table 1.4: Explanation of key movements in net worth

|

Relevant financial statement item |

Explanation for key movements in net worth |

|

Investments, loans and placements |

Investments, loans and placements comprise securities and other non-equity investments held for liquidity or policy purposes by the RBA. As a response to the COVID-19 pandemic, the RBA established the Term Funding Facility (TFF) to provide low-cost, fixed 3-year term funding to financial institutions. The TFF was closed to new drawdowns in June 2021. The RBA also purchased Australian, state and territory government bonds as part of the Bond Purchase Program (BPP). Repayments of TFF drawdowns were largely made by 30 June 2024, with the final drawdowns repaid on 1 July 2024. |

|

Equity investments |

Equity investments primarily comprise of the Department of Finance’s and the Future Fund’s holdings of listed equities and listed managed investment schemes. There was a $17.5 billion increase in the value of these investments due to an overall increase in amounts invested and the improvements in the performance of underlying equity markets. |

|

Other assets |

Other assets have increased by $30.9 billion mainly as a result of the:

|

|

Deposits held |

Financial institutions are required to deposit funds with the RBA’s exchange settlement accounts to settle financial obligations arising from the clearing of payments. This is recognised as a liability for the Australian Government. As part of the response to the COVID-19 pandemic, the RBA increased exchange settlement balances through to the TFF and BPP. The decline in exchange settlement balances during 2023–24 mainly reflects repayments of the TFF. |

|

Government securities |

Government securities are issued by AOFM to meet the Australian Government’s financing needs, and these are recognised as a liability. The increase in government securities is due to the following:

|

|

Provisions and payables |

Provisions and payables have increased by $41.8 billion mainly driven by the growth in the Department of Veterans’ Affairs’ military compensation provisions. This is because of higher claims experience and economic factors such as inflation and the actuarial modelling to reflect changes to key assumptions. |

Source: ANAO analysis of 2023–24 CFS.

Changes in the Australian Government’s net worth from 2014–15 to 2023–24

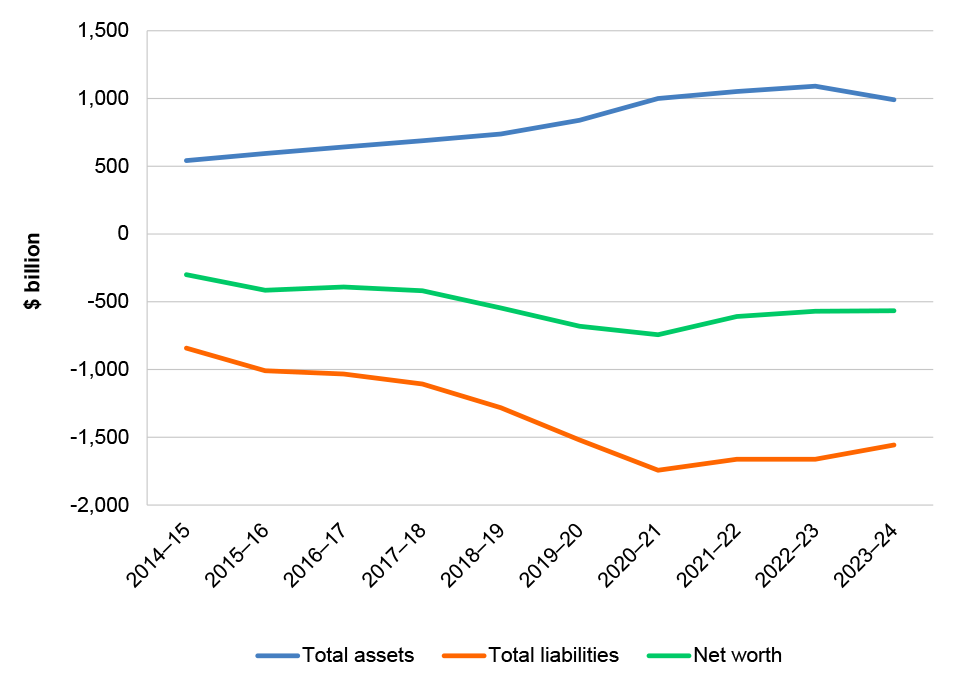

1.15 Figure 1.4 illustrates the total assets, total liabilities and net worth of the Australian Government since 2014–15. During the period:

- Total assets increased from $541.9 billion to $989.0 billion;

- Total liabilities increased from $841.8 billion to $1,556.5 billion; and

- the Net worth position decreased, from a deficiency of $299.8 billion to a deficit of $567.8 billion.

Figure 1.4: Australian Government’s total assets, total liabilities and net worth, from 2014–15 to 2023–24

Source: ANAO analysis of the 2014–15 to 2023–24 CFS.

Government securities

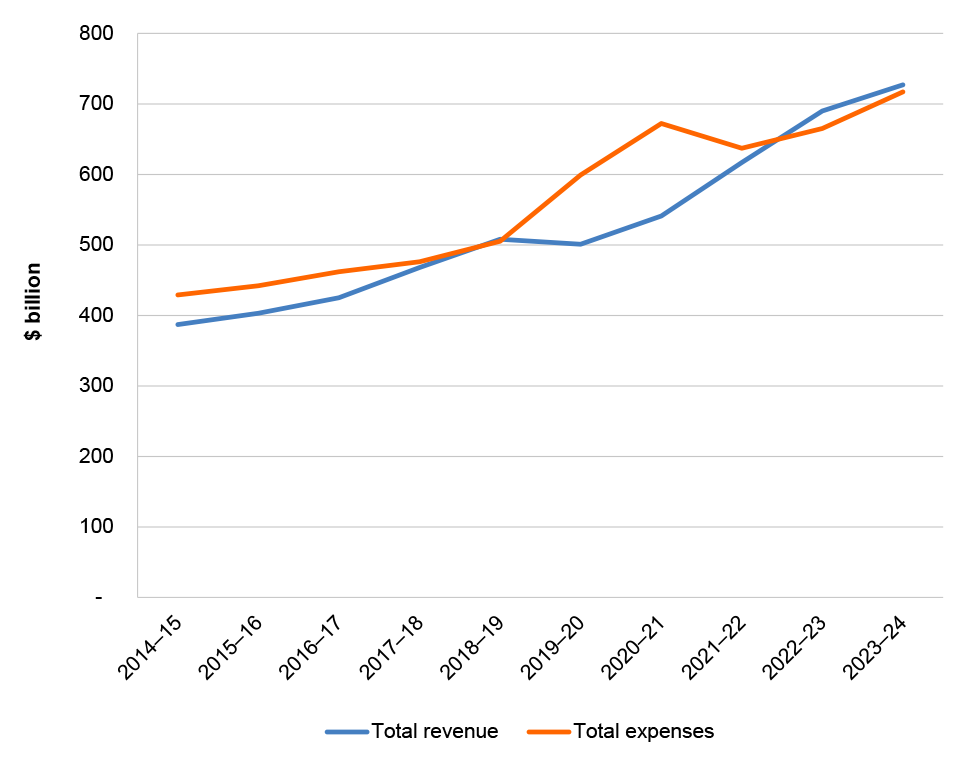

1.16 Government securities are primarily issued to meet the financing needs of the Australian Government and are issued to fund the operations of the Australian Government because over the period from 2014–15 to 2021–22, the Australian Government’s expenses have been greater than the revenue it received. Since 2022–23, revenues have exceeded expenses. Figure 1.5 illustrates the trend of Australian Government revenue and expenses over the period 2014–15 to 2023–24.

Figure 1.5: Australian Government revenue and expense for the period 2014–15 to 2023–24

Source: ANAO analysis of the 2014–15 to 2023–24 CFS.

1.17 The Australian Office of Financial Management (AOFM) is responsible for managing the Australian Government Securities, which totalled $844.2 billion for the GGS at 30 June 2024, comprised of Treasury Bonds, Treasury Indexed Bonds and Treasury Notes. The value of the Australian Government’s Securities is $611.0 billion largely due to the RBA holding a portion of Australian Government Securities on issue. While Figure 1.5 shows that revenue is greater than expenses for 2023–24, additional government securities were issued during the year, including $7.0 billion for the new Green Treasury Bonds.1

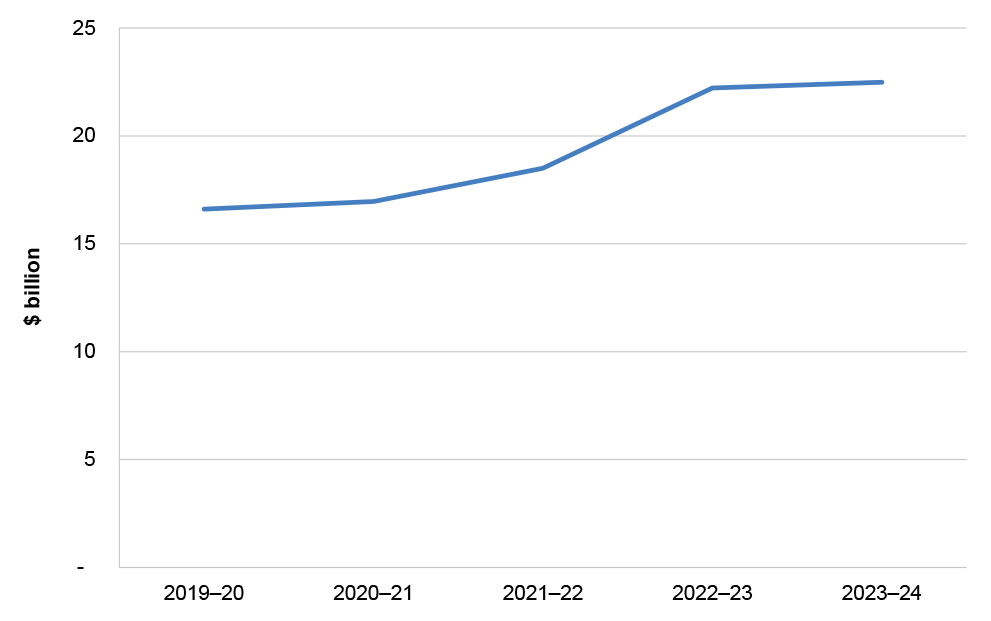

1.18 Figure 1.6 demonstrates the interest paid by AOFM on Government Securities over the five-year period from 2019–20 to 2023–24. During 2023–24 interest repayments flattened as interest rates have remained relatively stable. However, new securities issued during 2023–24 were issued at higher yields than in previous years. At 30 June 2024, the weighted average market yield on Treasury Bonds (the major portion of Australian Government Securities) was 4.18 per cent (2022–23: 4.06 per cent).

Figure 1.6: AOFM Government Securities Interest Paid from 2019–20 to 2023–24

Source: ANAO analysis of AOFM from 2019–20 to 2023–24.

Net debt

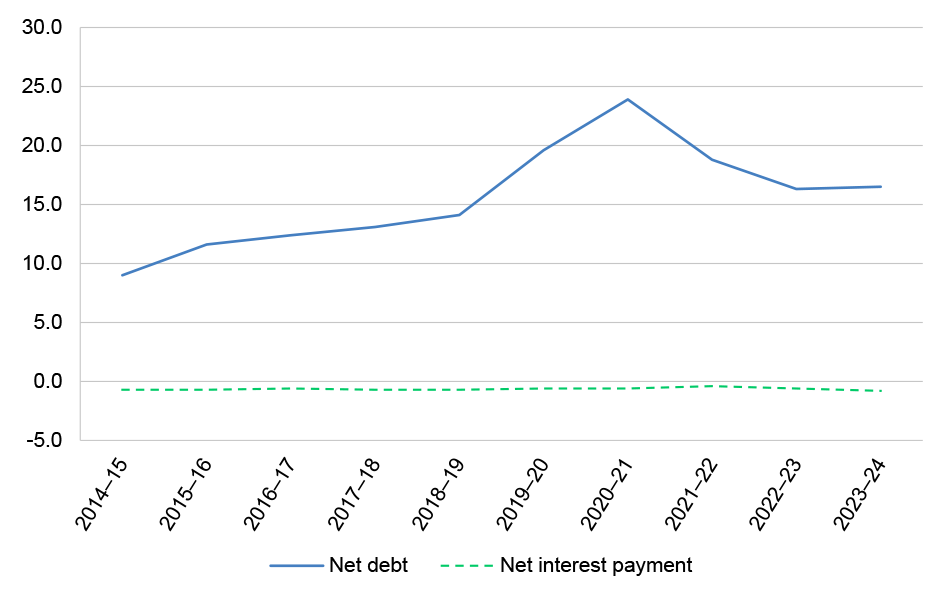

1.19 There was a steady growth in net debt as a percentage of Gross Domestic Product (GDP), growing from 9.0 per cent in 2014–15 and peaking in 2020–21 at 23.9 per cent due to the COVID-19 pandemic. Since this time there has been a decrease in the net debt position to 15.8 per cent of GDP in 2023–24.

1.20 Figure 1.7 illustrates the change in the indicators of the net financial position and net interest payments of the Australian Government from 2014–15 to 2023–24 as a percentage of GDP.

Figure 1.7: Australian Government net debt position as per cent of GDP, from 2014–15 to 2023–24

Source: ANAO analysis of 2023–24 commentary on the CFS.

Superannuation liabilities and the Future Fund

1.21 The Australian Government has superannuation liabilities arising from obligations to employees for defined benefit superannuation schemes. Note 9C of the CFS provides information on the nature of these schemes. The total superannuation net liability for these schemes was $308.5 billion as at 30 June 2024 ($313.1 billion as at 30 June 2023). The significant balances of the reported net liability relate to the following schemes that are closed to new members:

- Commonwealth Superannuation Scheme ($66.2 billion);

- Public Sector Superannuation Scheme ($101.7 billion);

- Military Superannuation Benefits Scheme ($101.2 billion); and

- Defence Force Retirement and Death Benefits Scheme ($31.7 billion).

1.22 The primary reason for the decrease in the liability is the increase in the discount rate used in valuing the superannuation liability between 30 June 2022 and 30 June 2024. The long-term nature of the superannuation liability means that small changes to the discount rate can have a large impact on the estimation of the value of the liability.

1.23 The Future Fund was established by the Future Fund Act 2006 to strengthen the Australian Government’s long-term financial position through the acquisition of financial assets and investments to assist in the discharge of the Australian Government’s superannuation liabilities. The Future Fund Board of Guardians is responsible for deciding how to invest the assets of the Future Fund through balancing the risk aspects of each investment mandate to maximise returns.

1.24 Figure 1.8 provides an overview of the balances of the Australian Government superannuation liabilities, the net investment balance of the Future Fund and the target asset level (TAL) from 2014–15 to 2023–24.

Figure 1.8: Total value of Australian Government superannuation liabilities and Future Fund investments, and the target asset level, from 2014–15 to 2023–24

Source: ANAO analysis of 2023–24 CFS and the Target Asset Level Declaration issued by the designated actuary of the Future Fund on 25 June 2021.

1.25 The TAL represents the best estimate of the assets required, together with investment earnings on those assets, which would be sufficient to meet unfunded superannuation benefit payments accrued up to the start of the financial year. The discount rate used to calculate the present value of future payments for TAL purposes represents the expected investment return on Future Fund assets. The Australian Government’s superannuation liability included in Figure 1.8 reflects the present value of future unfunded superannuation benefits payments discounted using the Commonwealth bond rate, in accordance with Australian Accounting Standards.

1.26 Figure 1.8 shows that the 2023–24 estimate of the TAL is $230.5 billion2, which is above the current Future Fund investment asset balance of $215.0 billion (2023: $202.9 billion). The Future Fund Act 2006 permits drawdowns when the balance of the Future Fund equals or exceeds the TAL. On 21 November 2024, the Australian Government announced that it would delay drawdowns from the Future Fund until at least 2032–33.3

Commonwealth investments

1.27 In recent years, the ANAO has identified an increase the number and size of investment schemes, investment mechanisms and ad-hoc investments. These investments have included direct equity investments such as Inland Rail Pty Ltd and Marinus Link Pty Ltd, the Capacity Investment Scheme and other direct investments such as Digicel and PSI Quantum Computing Corporation.

1.28 The ANAO has identified that the different vehicles for investments have different governance structures and the transparency of these investments is not consistent across the Commonwealth.

1.29 The Australian Government reports fiscal aggregates including net operating balance and underlying cash. These aggregates exclude cash or accounting movements that are of an investment or financing nature, such as investments made for policy purposes and the fair value losses on these investments.

1.30 Investments made for policy purposes have elements of economic and social benefits in addition to providing commercial returns to the Australian Government. These investments are also referred to as alternative financing arrangements.

1.31 The Parliamentary Budget Office (PBO) has noted that — ‘under successive governments there has been a shift toward delivering more government policies using alternative financing arrangements rather than direct payments’.4 The Joint Committee of Public Accounts and Audit (JCPAA) conducted an inquiry into Alternative Financing Mechanisms and released its report in March 2022.5

1.32 The JCPAA recommended that the Minister for Finance ‘consider changes to improve transparency for equity investments’ consistent with proposed improvements identified by the PBO to budget documents to assist Parliament in scrutinising investments for policy purposes.

1.33 This would improve transparency on where the government for policy purposes, is investing and seeking a sufficient rate of return on equity compared with those circumstances where the government is not investing to make a sufficient rate of return.

1.34 In response to the JCPAA’s recommendations, the Department of Finance introduced improvements to the transparency and disclosure in budget reporting of balance sheet items initially as part of the 2023–24 Budget. These improvements were made to enhance the understanding of the Australian Government’s financial position by parliamentarians and the public. The Department of Finance has maintained the same disclosure in the 2024–25 Budget.

1.35 The Department of Finance has advised the JCPAA that it will continue to look for opportunities to improve the level of transparency and disclosure contained in the Budget Papers.6

1.36 The ANAO has reviewed the recommendation regarding better segregation of the commercial and non-commercial portions (economic and social benefits) of the investments to better reflect the implications on key fiscal aggregates (of underlying cash and net operating balance) in the financial statements. The impact of the equity injections on operations of these entities is not reflected in the net operating balance unless dividends are received from the entities. The ongoing valuations of these entities are reflected in net worth. If the valuation of these entities deteriorates (for example as a result of accumulating losses or the valuation of future cash flows associated with assets procured through equity injections being less than their purchase costs), the deterioration in the position will be reflected in the GGS’ net worth but not impact on the net operating balance even if the deterioration was a predictable result of a non-commercial policy decision.

|

Case study 1. Case study Australian Rail Track Corporation — Equity injections for the Inland Rail project |

|

The Australian Government provides financing for the Inland Rail project through the Australian Rail Track Corporation (ARTC). At 30 June 2024 the Australian Government was committed to invest $14.0 billion of equity funding into ARTC to deliver the project (which is in early construction phases) with $0.7 billion (2022–23: $1.0 billion) in equity contributions provided in 2023–24. This is an example of a financing arrangement that requires an assessment of whether a sufficient rate of return can be generated from the investment to determine what portion reflects an economic transaction (equity investment) and which portion is for social benefits (grants expense). In the 2015 Inland Rail Business Case, it was determined that ‘Inland Rail would not generate sufficient access revenues to cover the full costs of the Programme, including, capital, operations and maintenance costs’.a ARTC’s accounting policy for the assets constructed in relation to the Inland Rail Line is to impair the expenditure based on the forecast net present value of the project to nil value on the construction of Inland Rail. This impairment is based on the judgement that the discounted future net cash flows from the operation on the Inland Rail are less than the cost of construction. Impairment of the expenses relating to the Inland Rail assets in 2023–24 amounted to $573.3 million (2022–23: $866.5 million). At the CFS level there is nothing in Australian Accounting Standards or the Commonwealth financial framework that precludes the transactions from being treated as equity injections. The ABS GFS Manual requires a realistic rate of return (for an underlying investment) in order for the transaction to be treated as equity when presenting the fiscal outcomes for the Australian Government general government sector. Where no realistic rate of return is achieved the transaction should impact on the net operating balance given the transaction is a result of a non-commercial policy decision. The current accounting treatment in the CFS is consistent with the Australian Accounting Standards. |

Note a: Inland Rail Program Business Case 2015, available from https://inlandrail.com.au/wp-content/uploads/2020/07/business-case-2015.pdf [accessed on 23 October 2024].

|

Case study 2. Case study Export Finance Australia loan to PSI Quantum Computing Corporation |

|

On 30 Apil 2024, the Commonwealth and the Queensland Governments signed an agreement to invest equivalent of $463.0 million via an equity investment and two loan tranches to PsiQuantum. One of the loans for $75.0 million will be made available to be drawn down in 2024–25 with the Commonwealth’s investment in PsiQuantum being made by Export Finance Australia (EFA) on the National Interest Account. The loan to PsiQuantum meets the definition of a concessional loan, with no principal or interest repayment to the Commonwealth required unless PsiQuantum is sold. A portion of the loan has been treated as a grant expense. |

Definitions used in this chapter

1.37 Table 1.5 provides a glossary of the key fiscal aggregates and other terminology used in this chapter to explain the Australian Government’s net worth and financial performance.

Table 1.5: Definitions of terms used

|

Name |

Definition |

|

Net operating balance |

This is calculated as income from transactions minus expenses from transactions. It is equivalent to the change in net worth arising from transactions. |

|

Operating result |

Income less expenses, excluding the components of other comprehensive income. Also known as ‘profit or loss’. The operating result includes the net operating balance plus items including net write-down of assets, net gains/(losses) from the sale of assets, net foreign exchange gains/(losses), net interest on derivatives gains/(losses), net fair value gains/(losses) and net other gains/(losses). |

|

Comprehensive result |

Total change in net worth before transactions with owners in their capacity as owners. Also known as ‘total change in net worth’. |

|

Fiscal balance |

The financing requirement of government, calculated as the net operating balance less the net acquisition of non-financial assets. A positive result reflects a net lending position and a negative result reflects a net borrowing position. Also known as net lending/(borrowing). |

|

Net worth |

The net worth of the Australian Government is defined as assets less liabilities. |

|

Net debt |

Net debt is equal to gross debt minus the stock position in financial assets corresponding to debt instruments. The Department of Finance defines net debt in the preface to the CFS as ‘the sum of deposits held, government securities, loans and lease liabilities less the sum of selected financial assets (cash and deposits, advances paid and investments, loans and placements). |

|

Government securities |

All securities issued by the Australian Government at tenders conducted by the AOFM. They comprise Treasury Bonds, Treasury Notes and Treasury Indexed Bonds. |

|

Investments for policy purposes |

Acquisitions of financial assets for policy purposes are distinguished from investments by the underlying government motivation for acquiring the assets. Where assets are acquired for the purpose of implementing or promoting government policy (e.g. loans to assist industry development), the acquisition of the assets is treated as being for policy purposes. Acquisition of financial assets for policy purposes includes government policies encouraging the development of certain industries or assisting citizens affected by natural disaster. |

|

Underlying cash balance |

Net cash receipts from operations (excluding net Future Fund earnings), less net capital investment (including by finance lease). |

Source: Australian Bureau of Statistics (2015). Australian System of Government Finance Statistics: Concepts, Sources and Methods; AASB 101 Preparation of Financial Statements, paragraphs 5 and 7; AASB 1049 Whole of Government and General Government Sector Financial Reporting, Appendix A; and Reserve Bank of Australia (2017). Glossary RBA. [Internet], available from https://www.rba.gov.au/glossary/ [accessed 22 October 2024].

2. Financial audit results and other matters

Chapter coverage

This chapter provides a summary of the:

- 2023–24 auditor’s reports issued by the ANAO;

- observations regarding entities’ internal control environments;

- unadjusted and adjusted audit differences reported to entities during 2023–24; and

- findings identified during the course of the 2023–24 financial statements audits of entities.

This chapter also provides analysis of the:

- quality and timeliness of financial statements preparation;

- timeliness of entities’ financial reporting;

- financial sustainability of material entities; and

- observations across the sector relating to: audit committee compliance and tenure, information technology (IT) controls, the prevalence and use of artificial intelligence (AI), the use of cloud computing and expenditure on official hospitality.

Conclusion

The ANAO issued 240 unmodified auditor’s reports, including the Australian Government’s Consolidated Financial Statements (CFS). The financial statements were finalised, and auditor’s reports issued for 79 per cent (2022–23: 91 per cent) of entities within three months of financial year-end.

The decrease in timeliness of auditor’s reports reflects an increase in the number of audit findings and legislative breaches identified by the ANAO, as well as limitations on the available resources within the ANAO in order to undertake additional audit procedures in response to these findings. During 2023–24 the ANAO delayed the final audits of a number of entities in order to address the increasing number of audit findings, particularly in material entities.

For most entities, at the completion of the final audits, key elements of internal control were operating effectively to provide reasonable assurance that the entities were able to prepare financial statements that were free from material misstatement. In five entities where significant audit findings were identified, these findings reduced the level of confidence and assurance that could be placed on key elements of internal control. These significant audit findings mainly related to corporate governance and IT governance and controls.

Timeliness of tabling of entity annual reports improved

Ninety-three per cent (2022–23: 66 per cent) of entities that are required to table an annual report in Parliament tabled prior to the date that the portfolio’s supplementary budget estimates hearing commenced. Supplementary estimates hearings were held one week later in 2023–24 than in 2022–23. Fifty-seven per cent of entities tabled annual reports one week or more before the hearing (2022–23: 12 per cent). Of the entities required to table an annual report, 4 per cent (2022–23: 6 per cent) had not tabled an annual report as at 9 December 2024.

Quality of financial statements improved

Seventy-one per cent of entities delivered financial statements in line with an agreed timetable (2022–23: 72 per cent). The total number of adjusted and unadjusted audit differences decreased during 2023–24, although 40 per cent of audit differences remained unadjusted. The quantity and value of adjusted and unadjusted audit differences indicate there remains an opportunity for entities to improve quality assurance over financial statements preparation processes.

Total audit findings have increased

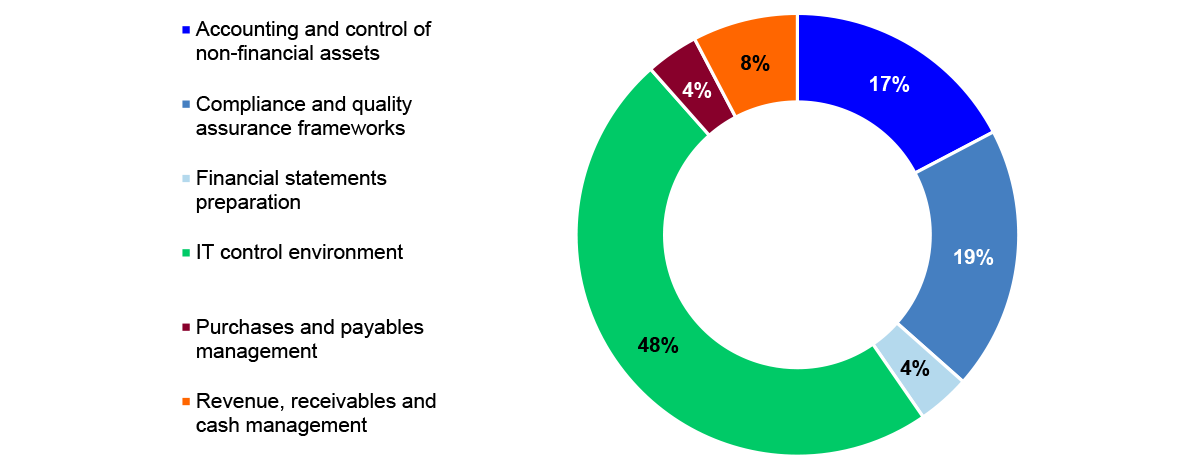

A total of 214 audit findings and legislative breaches were reported to entities in 2023–24 (2022–23: 200). These comprised six significant (2022–23: nine), 46 moderate (2022–23: 36), 147 minor findings (2022–23: 138) and 15 legislative breaches (2022–23: 14). The highest number of significant and moderate findings are in the categories of: IT control environment, including security, change management and user access; compliance and quality assurance frameworks, including legal conformance; and accounting and control of non-financial assets.

IT controls remain a key issue

Forty-three per cent of all audit findings identified by the ANAO related to the IT control environment, particularly IT security. Weaknesses in controls in this area can expose entities to an increased risk of unauthorised access to systems and data, or data leakage. The number of IT findings identified by the ANAO indicate that there remains room for improvement across the sector to enhance governance processes supporting the design, implementation and operating effectiveness of controls.

Audit committee member rotation considerations could be enhanced

The rotation of audit committee membership is not mandated. Finance has indicated that entities should consider the rotation of committee members to allow for a flow of new skills and talent through the committee and to ensure objectivity. Forty-four per cent of entities did not have a policy requirement for audit committee member rotation. Analysis of audit committee membership during 2023–24 indicates that individual committee members have served on average three years, ranging from one to 15 years.

Fraud framework requirements are largely in order

The Commonwealth Fraud Control Framework 2017 encourages entities to conduct fraud risk assessments at least every two years and entities responsible for activities with a high fraud risk may assess risk more frequently. All entities had in place a fraud control plan. Ninety-seven per cent of entities had conducted a fraud risk assessment within the last two years. Changes to the framework which occurred on 1 July 2024 requires entities to expand plans to take account of preventing, detecting and dealing with corruption, as well as periodically examining the effectiveness of internal controls.

Compliance mechanisms supporting the provision of hospitality could be more widely adopted

Eighty-one per cent of entities permit the provision of hospitality and the majority have policies, procedures or guidance in place. Expenditure for the period 2020–21 to 2023–24 was $70.0 million. Official hospitality involves the provision of public resources to persons other than officials of an entity to achieve the entity’s objectives. There are no mandatory requirements for entities in managing the provision of hospitality, however, Finance does provide some guidance to entities in model accountable authority instructions. Of those entities that permit hospitality, 83 per cent have established formal policies, guidelines or processes.

Seventy-four per cent of entities included compliance requirements in their policies, procedures or guidance which support entities obtaining assurance over the conduct of official hospitality. Compliance processes included acquittals, formal reporting, attestations from officials and/or periodic internal audits. Thirty-one per cent of entities had established formal reporting on provision of official hospitality within their entities, with reporting to the Accountable Authority, executive management board or Chief Financial Officer.

Further adoption of artificial intelligence

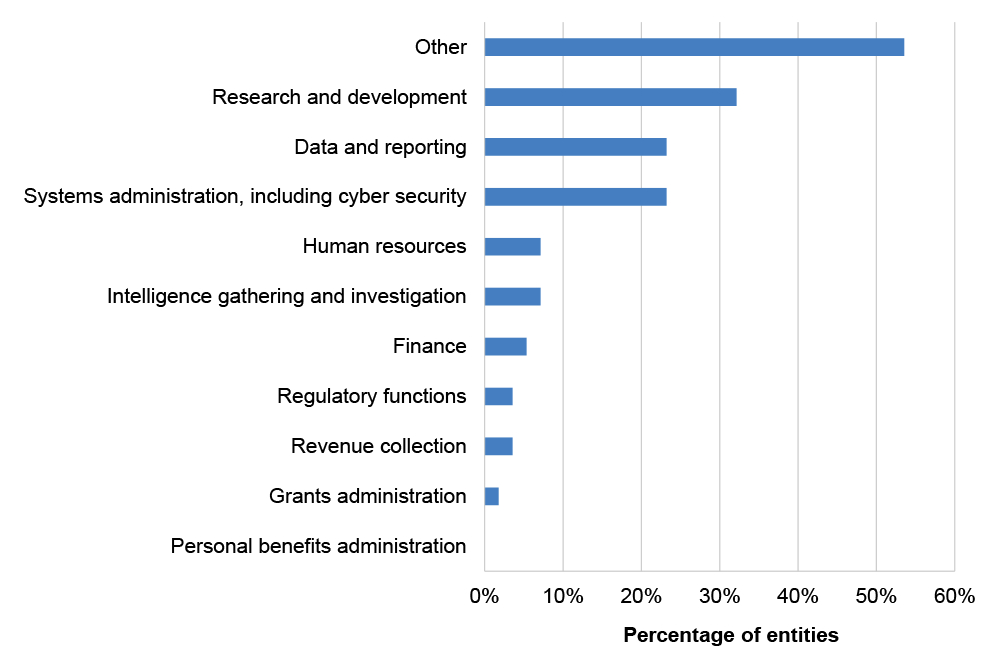

Fifty-six entities used AI in their operations during 2023–24 (2022–23: 27 entities). Most of these entities had adopted AI for research and development activities, data and reporting and/or IT systems administration.

During 2023–24, 64 per cent of entities that adopted AI had also established internal policies governing the use of AI (2022–23: 44 per cent). Twenty-seven per cent of entities had established internal policies regarding assurance over AI use. An absence of governance frameworks for managing the use of emerging technologies could increase the risk of unintended consequences. In September 2024, the Digital Transformation Agency (DTA) released the Policy for the responsible use of AI in government, which establishes requirements for accountability and transparency on the use of AI within entities.

Assurance over effectiveness of cloud computing arrangements could be improved

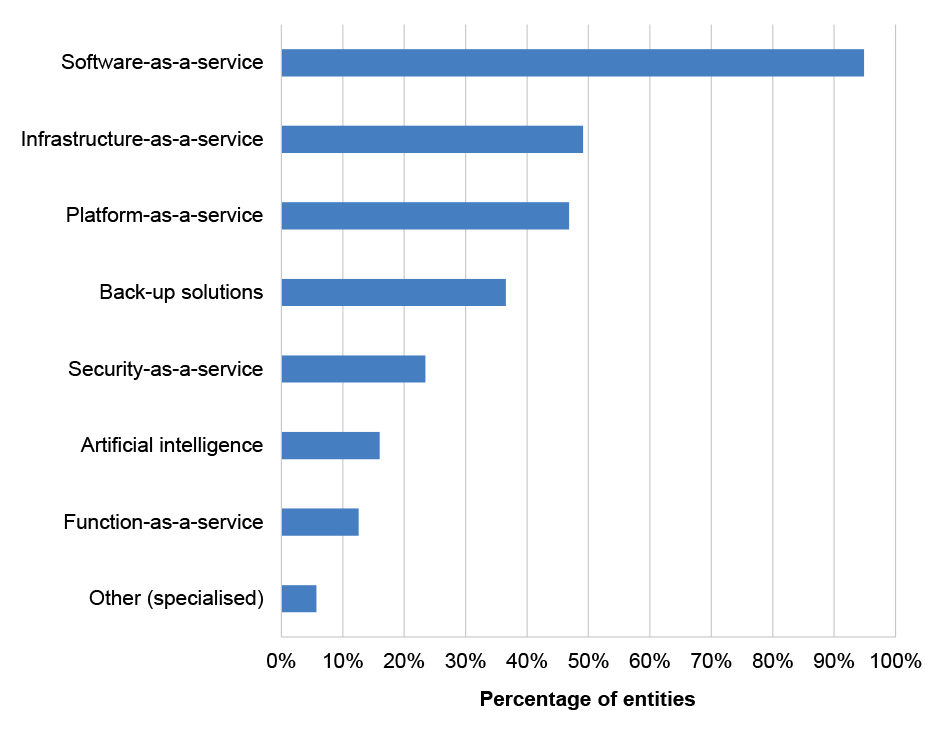

During 2023–24, 89 per cent of entities used cloud computing arrangements (CCAs) as part of the delivery model for the IT environment, primarily software-as-a-service (SaaS) arrangements. A Service Organisation Controls (SOC) certificate provides assurance over the implementation, design and operating effectiveness of controls included in contracts, including security, privacy, process integrity and availability. Twenty-five per cent of entities received a SOC certificate for all CCA services provided. Eighty-two per cent of entities did not have in place a formal policy or procedure which would require the formal review and consideration of a SOC certificate. In the absence of a formal process for obtaining and reviewing SOC certificates, there is a risk that deficiencies in controls at a service provider are not identified, mitigated or addressed in a timely manner.

Continuing legislative breaches arising from incorrect payments made to Key Management Personnel

Fifty-three per cent of legislative breaches identified by the ANAO in 2023–24 relate to incorrect payments of remuneration to key management personnel (KMP) and/or non-compliance with determinations made by the Remuneration Tribunal.

Financial sustainability in material entities remains sound

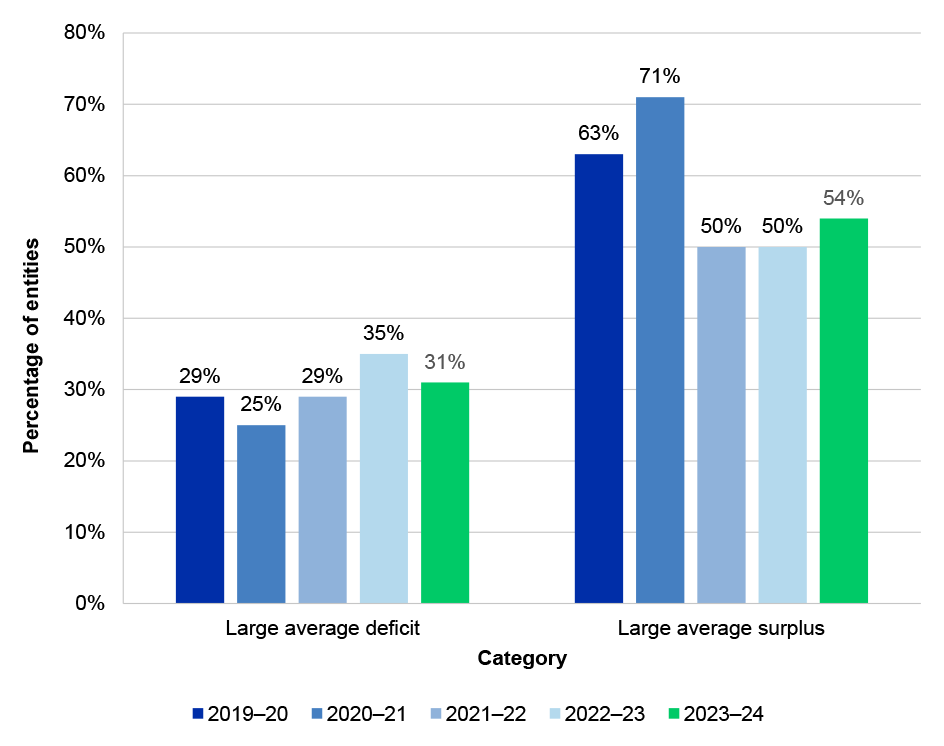

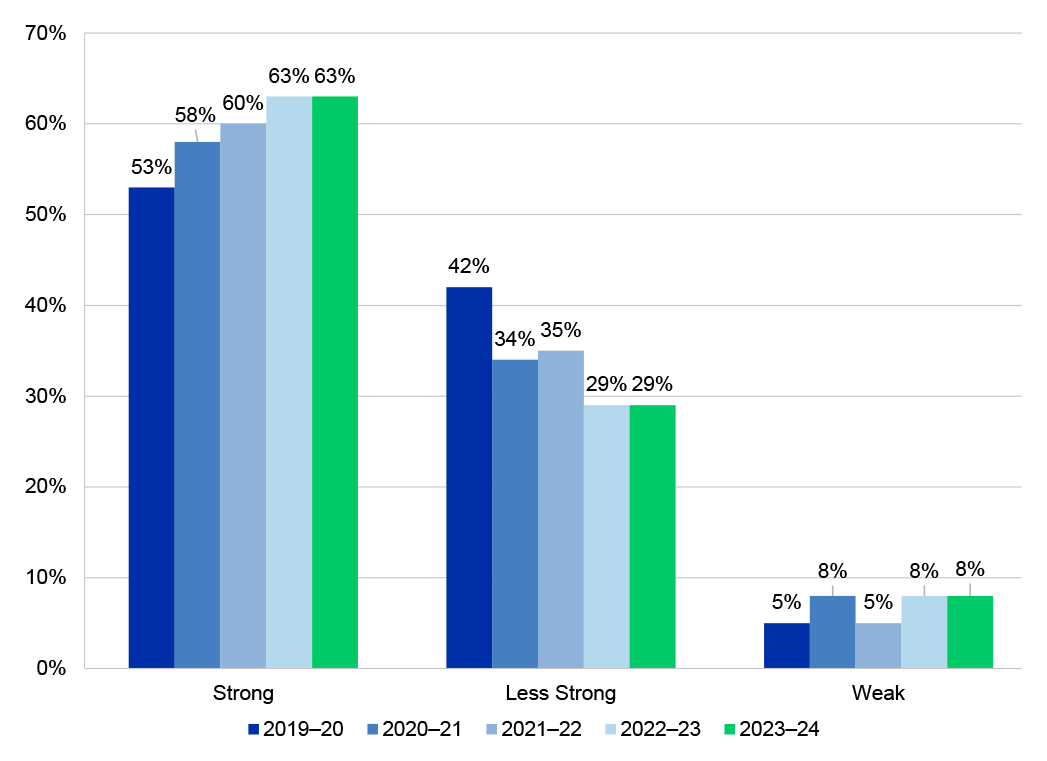

An analysis of the operating results and balance sheet positions for material entities concluded that the financial sustainability for the majority of those entities was not at risk.

Opportunities for improvement

The following opportunities for improvement are discussed in this chapter.

- Entities could enhance the effectiveness of their audit committees by adopting a formal process for rotation of audit committee membership, which balances the need for continuity and objectivity.

- Entities that provide official hospitality should have policies and guidance in place which clearly set expectations for officials.

- Entities with higher levels of exposure to the provision of official hospitality could give further consideration to implementing or enhancing compliance and reporting arrangements. Where designed appropriately, compliance activities would support assurance that expenditure on official hospitality is proper and publicly defensible. Entities may also consider whether regular and formal reporting to management, and those officers charged with governance, would increase transparency and manage risks associated with provision of official hospitality.

- Entities that use CCA service providers should consider whether there is a need to obtain a SOC certificate to obtain assurance about the implementation, design and operating effectiveness of controls at a service provider. Entities should have a policy which requires the review and consideration of the SOC, including any actions taken to address deficiencies or manage the contract with the service provider.

- Entities should monitor and evaluate the effectiveness of their IT controls to ensure risks are successfully managed. In particular, continuous assessment of controls related to change management practices, timely removal of user access and disaster recovery testing would improve the management of IT risks. Having a systematic approach to assessing the design, implementation and operating effectiveness of controls increases the chances of successfully managing IT risks.

- Effective management of remuneration includes aligning payroll process with policy, legal and contractual requirements.

Introduction

2.1 The Auditor-General for Australia is required by the Public Governance, Performance and Accountability Act 2013 (PGPA Act) to audit and report on the financial statements of all Commonwealth entities, Commonwealth companies and their subsidiaries.7 This chapter summarises the results of the 2023–24 financial statements audits and provides information on certain topics relating to the governance and administration of entities.

Summary of 2023–24 auditor’s reports

Timeliness of auditor’s reports decreased due to an increasing number of complex audit findings and matters identified impacting the preparation of financial statements

At 9 December 2024, the ANAO had issued 240 unmodified auditor’s reports, including the Australian Government’s Consolidated Financial Statements (CFS). Seventy-nine per cent of auditor’s reports were signed within three months of year-end compared to 91 per cent in 2022–23. The decrease in timeliness of auditor’s reports reflects an increase in the number of audit findings and legislative breaches identified, which were considered by the ANAO in forming an opinion over entity financial statements, and limitations on the available resources within the ANAO in order to undertake the audit work arising from these findings.

Auditor’s reports issued

2.2 A comparison of the number and type of auditor’s reports issued by the Auditor-General and their delegates in 2022–23 and 2023–24 (as at 9 December 2024), including the CFS is summarised at Table 2.1.

Table 2.1: Summary of auditor’s reports issued and outstanding as at 9 December 2024 and 30 November 2023

|

Auditor’s report |

2023–24 |

2022–23 |

|

Unmodified |

240 |

241a |

|

13a |

15 |

|

– |

– |

|

Modified |

– |

– |

|

Auditor’s reports issued |

240 |

241 |

|

Not yet issued |

6b |

3c |

|

Total number of financial statements auditsd |

246 |

244 |

Note a: Thirteen of the unmodified auditor’s reports included an emphasis of matter.

The auditor’s report for seven entities included an emphasis of matter to draw users’ attention to the basis of preparation of the financial statements or restrictions on the distribution or use of the auditor’s report. These entities are: Australia Post Licensee Advisory Council Limited; Australian Sports Foundation Charitable Trust; Darwin Hotel Partnership; Gagudju Lodge Cooinda Trust; IBA Retail Property Trust; Performance Bond Fund; and Tennant Creek Land Holding Trust.

The auditor’s report for six entities included an emphasis of matter to draw to users’ attention a particular matter in the financial statements. These entities are: Australian Scientific Instruments Pty Ltd; Departments of: Veterans’ Affairs; and Social Services; Natural Heritage Trust of Australia; National Health Funding Body; and Seafarers Safety, Rehabilitation and Compensation Authority. For details of each of the matters included in the auditor’s report, refer to Chapter 4.

Note b: As at 9 December 2024, the 2023–24 financial statements audits had not been finalised for the following entities: IBA Retail Asset Management Pty Ltd; Ikara Wilpena Enterprises Pty Ltd; Ikara Wilpena Holdings Trust; National ICT Australia Ltd; Royal Australian Navy Central Canteens Board; and Win with Navy Ltd.

Note c: As at 30 November 2023, the 2022–23 financial statements audits had not been finalised for the following entities: Bundanon Trust; Royal Australian Navy Central Canteens Board; and Wreck Bay Aboriginal Community Council. These audits were subsequently finalised. The results of these audits were reported in Auditor-General Report No. 42 2023–24 Interim Report on Key Financial Controls of Major Entities.

Note d: The Consolidated Financial Statements is included in the total number of financial statements audits.

Source: 2022–23 and 2023–24 ANAO auditor’s reports.

2.3 A financial statements audit is finalised when the auditor has formed an opinion on the financial statements, and that opinion has been expressed through a written report.

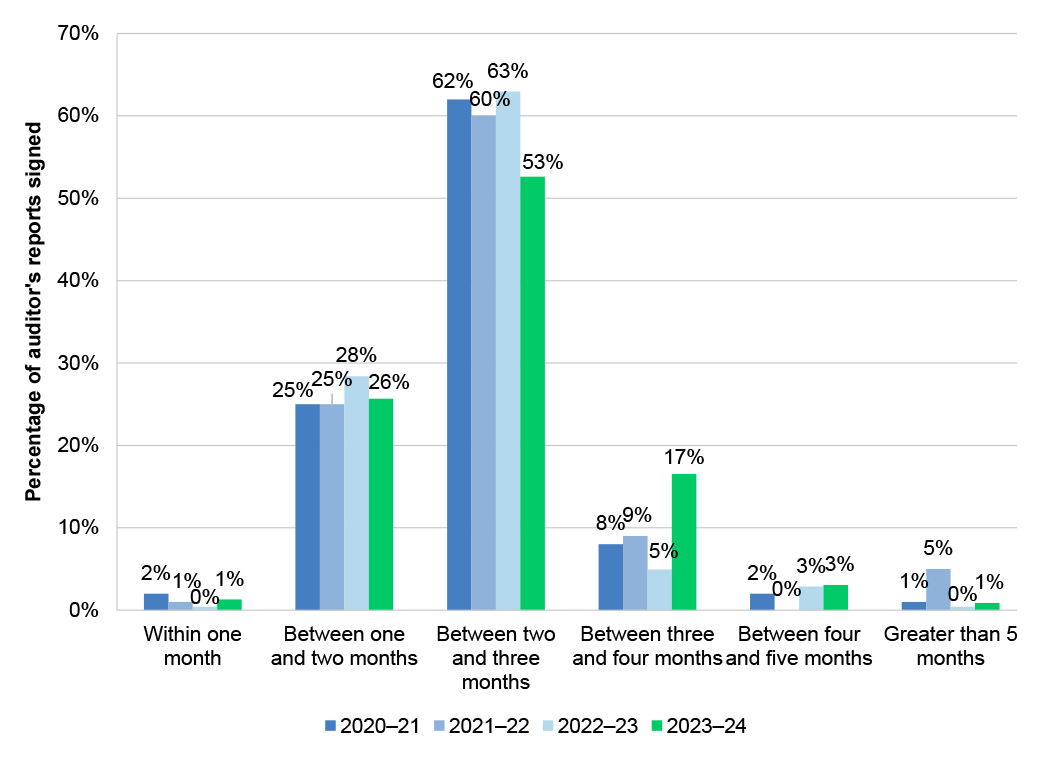

2.4 The ANAO’s 2024–25 Corporate Plan included a performance measure ‘Percentage of mandated financial statements audit reports issued in time to meet entity annual reporting timeframes’, for which the target was set at 85 per cent within three months of the end of the financial year. Figure 2.1 shows that the finalisation of financial statements audits within three months of the reporting date has decreased from 2022–23. Seventy-nine per cent of auditor’s reports were issued within three months of the end of the reporting period compared to 91 per cent in 2022–23.

Figure 2.1: Timeframes for auditor’s report signing from the end of financial year

Source: ANAO analysis.

2.5 The decrease in timeliness of auditor’s reports in 2023–24 is largely due to:

- an increase in the number of audit findings identified by the ANAO during 2023–24. Audit findings are representative of weaknesses in entity internal control supporting the preparation of the financial statements. Where audit findings are identified the ANAO is generally required to perform alternative or additional audit procedures, to gain sufficient and appropriate audit evidence that the financial statements are not materially misstated; and

- the nature of the ANAO’s resourcing base. The ANAO is funded to undertake financial statements audits via an annual appropriation. When audit findings, contentious matters or audit differences are identified, the ANAO must work within its existing resourcing base in order to finalise these engagements and perform the necessary alternative or additional audit procedures. In these circumstances, the ANAO prioritises the completion of material entity audits in support of the preparation of the Australian Government’s Consolidated Financial Statements. During 2023–24 the ANAO delayed the audit of ten entities in order to complete the audits of material entities. These entities were the: Australian Strategic Policy Institute Ltd; Australian Submarine Agency; Australian Transport Safety Bureau; Independent Health and Aged Care Pricing Authority; Independent Parliamentary Expenses Authority; IP Australia; Office of the Director of Public Prosecutions (Cth); Old Parliament House; Parliamentary Workplace Support Service; and Wreck Bay Aboriginal Community Council.

2.6 The ANAO issued 98 per cent of auditor’s reports within two business days of the signing of the financial statements by the accountable authority (2022–23: 99 per cent).

What is the ANAO’s assessment of the effectiveness of entity internal control environments supporting the financial statements?

Internal controls largely supported the preparation of financial statements that were free from material misstatement

For most entities, at the completion of the final audits, key elements of internal control were operating effectively to provide reasonable assurance that the entities were able to prepare financial statements that were free from material misstatement. In five entities where significant audit findings were identified these findings reduced the level of confidence and assurance that could be placed on key elements of internal control. These significant audit findings mainly related to corporate governance and IT governance and controls.

Audit committee member rotation considerations could be enhanced

The rotation of audit committee membership is not mandated. Finance has indicated that entities should consider the rotation of committee members to allow for a flow of new skills and talent through the committee and to ensure objectivity. Forty-four per cent of entities did not have a policy requirement for audit committee member rotation. Of those entities that did have a policy, the average term for rotation was five years, ranging from two to 10 years. Analysis of audit committee membership during 2023–24 indicates that individual committee members have served on average three years, ranging from one to 15 years.

Fraud framework requirements are largely in order

The Commonwealth Fraud Control Framework 2017 encourages entities to conduct fraud risk assessments at least every two years and entities responsible for activities with a high fraud risk may assess risk more frequently. All entities had in place a fraud control plan. Ninety-seven per cent of entities had conducted a fraud risk assessment within the last two years. Changes to the framework on 1 July 2024 will require entities to expand plans to take account of preventing, detecting and dealing with corruption, as well as periodically examining the effectiveness of internal controls.

Opportunities for improvement

Entities could enhance the effectiveness of their audit committees by adopting a formal process for rotation of audit committee membership, which balances the need for continuity and objectivity of membership.

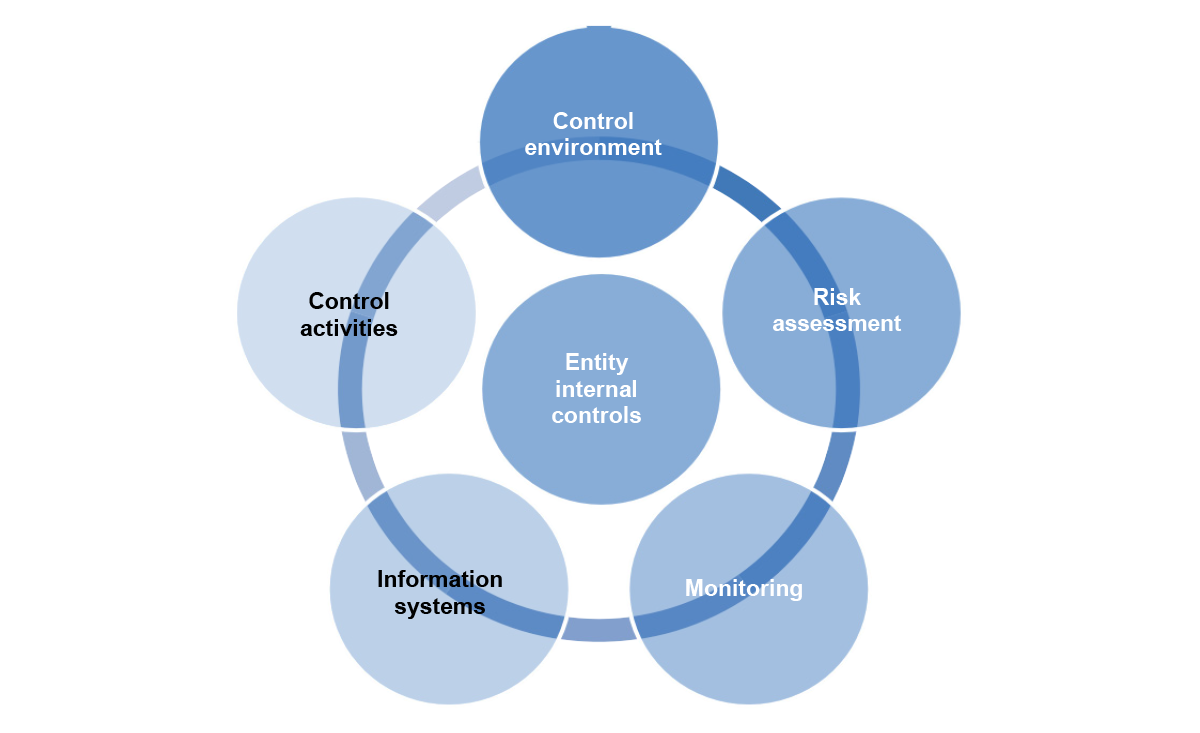

2.7 The ANAO applies the framework in ASA 315 Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and its Environment to consider the impact of elements of an entity’s internal controls supporting the preparation of financial statements. This approach provides a basis for designing and implementing responses to the assessed risk of material misstatement. Figure 2.2 outlines these elements.

Figure 2.2: Elements of entity internal controls

Source: ASA 315 Identifying and assessing the risk of material misstatement through understanding the entity and its environment, paragraphs 4 to 21.

2.8 An effective internal control framework provides a level of assurance that entities are able to prepare financial statements that are free from material misstatement. For the majority of entities in 2023–24 key elements of internal control were operating effectively, providing the ANAO with reasonable assurance that the prepared financial statements were free from material misstatement.

2.9 Except for particular finding/s outlined in Chapter 48, key elements of internal control were operating effectively to provide reasonable assurance that entities are able to prepare financial statements that are free from material misstatement. These particular findings reported to entities represented moderate or significant business or financial management risk to the entity.

2.10 For entities where audit findings were reported, the ANAO was required to undertake additional audit procedures to obtain sufficient and appropriate audit evidence that provided reasonable assurance the entity’s financial statements were not materially misstated.

2.11 Table 2.2 details the assessment of the effectiveness of the elements of internal control at the conclusion of the final audit for the entities included in this report.

Table 2.2: Assessment of the effectiveness of the elements of internal control

|

Overall assessment of effectiveness of elements of internal control supporting the preparation of financial statements |

Percentage of entities (%) |

|

Effective, with no significant or moderate audit findings identified |

88 |

|

Effective, with the exception of particular moderate audit findings identified |

10 |

|

Reduced level of reliance due to significant audit findings identified |

2 |

Source: ANAO analysis of 2023–24 audit results.

2.12 There were six significant audit findings reported to five entities during 2023–24 which reduced the level of reliance which could be placed on the effective operation of internal control supporting the preparation of the financial statements. The audit findings reported to these entities presented a significant business or financial management risk to each entity. These included issues that could result in a material misstatement of the entity’s financial statements. The five entities are: the Anindilyakwa Land Council; Australian Taxation Office; Department of Defence; Department of Health and Aged Care; and Services Australia.

Control environment

2.13 The PGPA Act sets out the requirements to establish and maintain systems relating to risk and control. Section 16 of the PGPA Act states that:

The accountable authority of a Commonwealth entity must establish and maintain:

(a) an appropriate system of risk oversight and management for the entity; and

(b) an appropriate system of internal control for the entity;

including by implementing measures directed at ensuring officials of the entity comply with finance law.9

2.14 An effective control environment is underpinned by a fit-for-purpose governance structure. Indicators of an effective governance structure include whether management has established frameworks and processes that promote positive attitudes, awareness and actions concerning the entity’s internal controls and their importance in the entity. The main elements reviewed included: governance structures relevant to the preparation of the financial statements; audit committee and assurance arrangements; systems of authorisation; and processes for recording financial transactions.

2.15 Clear lines of accountability and reporting are important in establishing a strong internal control environment for the purposes of preparing the financial statements. The involvement of those charged with governance is an important element of these structures. Just as important is ensuring that staff at all levels in an entity understand their own role in the control framework. This can be achieved through the issuance of accountable authority instructions and delegation instruments.

Audit committees

2.16 Audit committees play an important role in providing advice to Accountable Authorities over the appropriateness of an entity’s financial reporting, performance reporting, system of risk oversight and management and system of internal control.

2.17 Finance’s Resource Management Guide (RMG 202) relating to audit committees, describes a committee’s role as supporting good governance of entities.10 The Public Governance, Performance and Accountability Act 2013 (PGPA Act) and Public Governance, Performance and Accountability Rule 2014 (PGPA Rule) prescribe requirements for establishment, membership and functions of these committees. With the exception of three entities, the ANAO’s analysis confirms that for all entities in this report:

- have established audit committees that meet the minimum requirements for audit committees as outlined in section 1711 or section 2812 of the PGPA Rule;

- committees consist of a majority of members which were assessed by the entity to be independent;

- all committee chairs were independent members; and

- an audit committee charter, that is consistent with their obligations under subsection 17(2) of the PGPA Rule, is in place.

2.18 The entities that did not meet these minimum requirements were the: Australian Strategic Policy Institute Ltd; National Transport Commission; and Royal Australian Air Force Veterans’ Residences Trust.13

2.19 The rotation of audit committee membership is not mandated. Finance’s RMGs indicate that: ‘it is important to rotate the audit committee members to allow for a flow of skills and talent through the committee, enhancing its effectiveness and ensuring its objectivity’.14 Finance also indicates that: ‘The frequency of rotation of committee members needs to be balanced against the time it takes to develop experience and knowledge of the entity’s operations and to develop productive relationships with the entity’s officials and the other audit committee members’.15

2.20 Fifty-six per cent of entities had implemented a rotation policy for members of their audit committee. These entities included individual member rotation requirements which specified the maximum period of time in which a member could serve on the committee.

2.21 Figure 2.3 demonstrates the range of the maximum time period for audit committee members for entities with rotation requirements is two to 10 years. The average maximum time period permitted for these entities was five years.

Figure 2.3: Maximum number of years which can be served by audit committee members as per entity audit committee charters

Source: ANAO analysis of entity audit committee charters.

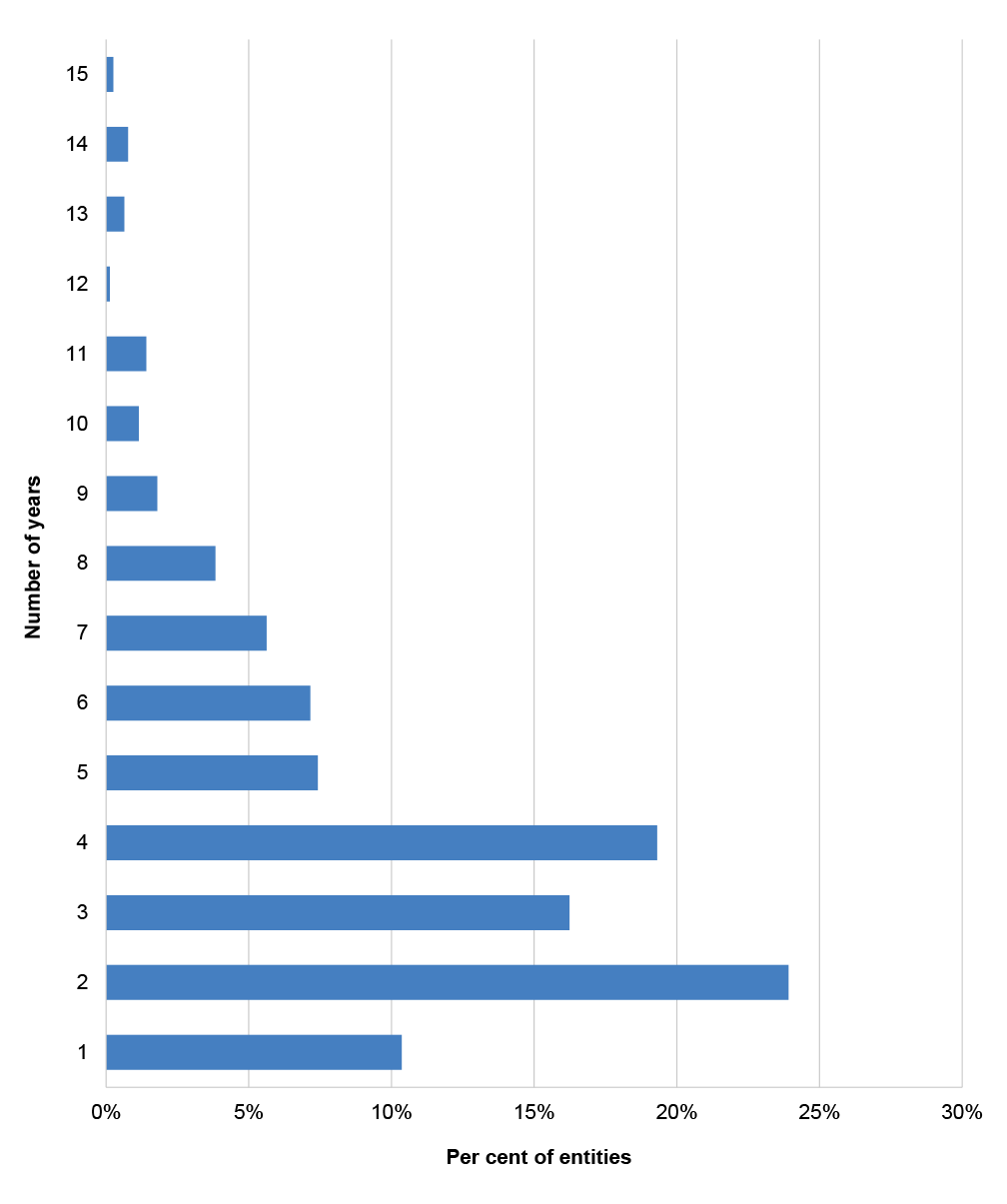

2.22 Figure 2.4 demonstrates that during 2023–24 the range of the total time served by individual members of audit committees was one to 15 years, with an average of three years. Twenty-five per cent of members were appointed to an audit committee during 2023–24.

Figure 2.4: Percentage of the number of years served by entity audit committee members for all entities

Source: ANAO analysis of audit committee member tenure at 30 June 2024.

2.23 The PGPA Act and Rule do not specify the total number of audit committees which an individual can be a member. Finance’s RMGs indicate that:

An audit committee’s effectiveness can be enhanced by having members with experience on other public or private sector audit committees and with networks to other audit committees. However, membership of multiple audit committees needs to be balanced against the ability to understand the issues and operating context of a specific entity.16

2.24 Of individual audit committee members during 2023–24:

- Sixty-three per cent of individuals were appointed only one audit committee.

- The total range of committees served by individuals was one to 15.

- One per cent, or 11 individuals, served on more than five audit committees.

Opportunity for improvement

2.25 Entities could enhance the effectiveness of their audit committees by adopting a formal process for rotation of audit committee membership, which balances the need for continuity and objectivity.

Fraud risk assessment processes

2.26 Section 16 of the PGPA Act sets out an accountable authority’s responsibilities regarding the establishment of appropriate risk oversight and management in an entity. An understanding of an entity’s process to identify and manage risk is essential to an effective and efficient financial statements audit. A review of this process is completed to assist the ANAO to understand how entities identify and manage fraud risks relating to financial statements and assess the risk of material misstatement to an entity’s financial statements.

Fraud control

2.27 Section 10 of the PGPA Rule details the minimum standards for accountable authorities of Commonwealth entities for managing the risk and incidence of fraud. The accountable authority of an entity must take all reasonable measures to prevent, detect and deal with fraud relating to the entity. This includes conducting fraud risk assessments regularly and when there is a substantial change in the structure, functions or activities of the entity.17

2.28 The Commonwealth Fraud Control Framework 2017, encourages entities to conduct fraud risk assessments at least every two years and entities responsible for activities with a high fraud risk may assess risk more frequently.18

2.29 The ANAO analysed the extent to which the guidance and requirements of the Commonwealth Fraud Control Framework 2017 were implemented by entities at 30 June 2024 and identified that:

- all entities have developed and implemented a fraud control plan to prevent and detect fraud19;

- all entities had undertaken a fraud risk assessment. However, six entities had not conducted a fraud risk assessment within the last two years. These entities are: Attorney-General’s Department; Australian Centre for International Agricultural Research; Australian National Maritime Museum; Australian Radiation Protection and Nuclear Safety Agency; Sydney Harbour Federation Trust; and Wine Australia.

2.30 On 1 July 2024, the Commonwealth Fraud and Corruption Control Framework came into effect.20 In addition to the existing requirements of the 2017 framework, the new framework requires that:

- accountable authorities also take steps to prevent, detect and deal with corrupt conduct, in addition to fraud;

- entities have in place governance structures and processes to oversee and manage risks of fraud and corruption;

- entities have in place officials who are responsible for managing risks of fraud and corruption; and

- entities must periodically review the effectiveness of their fraud and corruption controls.

Information systems and communication

2.31 The information system relevant to the preparation of the financial statements consists of activities and policies, and accounting and supporting records, designed and established to initiate, record and process entity transactions (as well as to capture, process and disclose information about events and conditions other than transactions).

2.32 An entity’s business processes include activities that are designed to record information, including accounting and financial reporting information and to ensure compliance with laws and regulations.

2.33 Ninety-two audit findings have been reported to entities in 2023–24 relating to the IT control environment, accounting for 43 per cent of all audit findings identified by the ANAO. The most common findings identified related to weaknesses in: privileged and other user access; and change management. Further information relating to these findings is available in paragraphs 2.87 to 2.97.

Control activities

2.34 The control activities component of an entities’ system of internal control are primarily direct controls which are designed to prevent, detect or correct misstatements.21 Auditors are required to evaluate the design of the controls and determine whether the controls have been implemented. Controls include authorisations and approvals, reconciliations, verifications (such as edit and validation checks or automated calculations), segregation of duties, and physical or logical controls, including those addressing safeguarding of assets.

2.35 Where the ANAO identifies one or more control deficiencies, the ANAO assesses whether, individually or in combination, the deficiencies constitute a significant deficiency and reports these to accountable authorities as audit findings. The ANAO applies professional judgement in determining whether a deficiency represents a significant control deficiency. Information relating to the audit findings identified by the ANAO during the 2023–24 audits is available at paragraphs 2.72 to 2.137.

How are entities managing the provision of hospitality?

Eighty-one per cent of entities permit the provision of hospitality and the majority have policies, procedures or guidance in place

Official hospitality involves the provision of public resources to persons other than officials of an entity to achieve the entity’s objectives. There are no mandatory requirements for entities in managing the provision of hospitality, however, Finance does provide some guidance to entities in model accountable authority instructions. Eighty-one per cent of entities permit the provision of hospitality. Of those entities that permit hospitality, 83 per cent have established formal policies, guidelines or processes. Where a policy is in place, 13 per cent included caps on expenditure per person or event. The delegation to approve official hospitality was generally at senior executive level.

Most entities do not identify provision of hospitality as a risk

The provision of hospitality could have increased risks associated with probity and transparency. Sixteen per cent of entities identified specific risks associated with the provision of hospitality in their entity level risk assessment process. These risks included compliance focused areas such as self-approval of expenses as well as risk associated with conflict of interest arising from provision of hospitality.

Compliance mechanisms supporting the provision of hospitality could be more widely adopted